- United States

- /

- Media

- /

- NasdaqGS:SATS

EchoStar (SATS) Valuation Revisited After Spectrum Deals and Analyst Upgrades Reshape Growth Narrative

Reviewed by Simply Wall St

EchoStar (SATS) has suddenly moved from underdog to talking point after a wave of upbeat analyst calls and multibillion dollar spectrum deals with AT&T and SpaceX reshaped how investors view the business.

See our latest analysis for EchoStar.

Those spectrum headlines have landed on top of an already powerful move, with EchoStar’s share price return up 58.7 percent over the past month and roughly 378.6 percent year to date. The 1 year total shareholder return of about 379.9 percent suggests momentum has shifted decisively in the bulls’ favor.

If EchoStar’s surge has you thinking about what else might rerate sharply, it could be a good moment to explore fast growing stocks with high insider ownership.

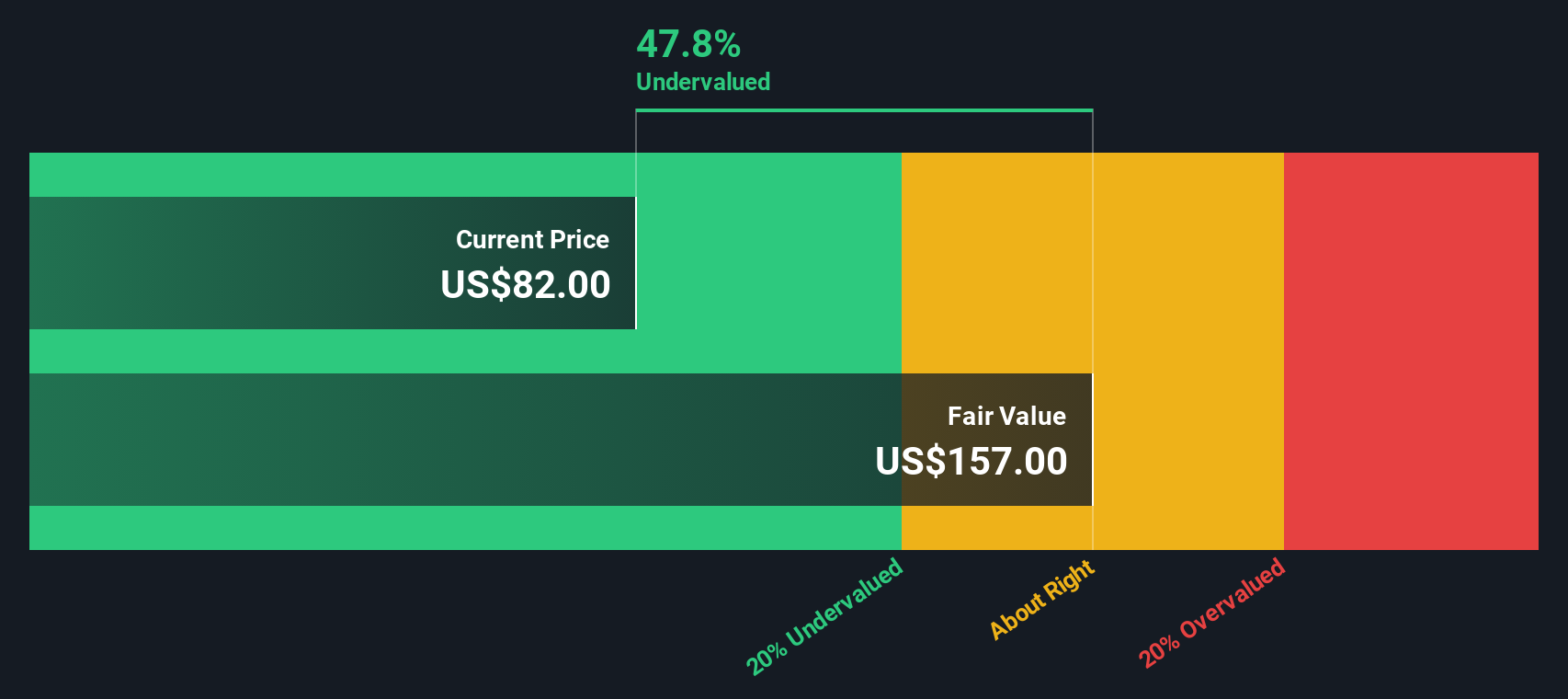

Yet with EchoStar now trading above the average analyst target but still showing a sizeable discount to some fair value estimates, investors face a tougher question: is this a fresh buying opportunity, or is future growth already priced in?

Most Popular Narrative: 20.6% Overvalued

The most followed narrative now pegs EchoStar’s fair value near $90 per share, notably below the $108.88 last close. This frames a rich valuation backdrop.

Analysts have raised their price target on EchoStar by approximately 13 percent to around $90 per share, reflecting a lower perceived discount rate and higher future valuation multiples that more than offset slightly softer long term revenue growth and margin assumptions.

Want to see why a slower revenue path still justifies a loftier multiple? The narrative quietly leans on future margins and valuation math that might surprise you.

Result: Fair Value of $90.29 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that optimism could unravel if regulatory uncertainty over key spectrum licenses drags on, or if heavy debt obligations force dilutive capital raises.

Find out about the key risks to this EchoStar narrative.

Another View: DCF Points to Upside

While the popular narrative flags EchoStar as roughly 21 percent overvalued around $109, our DCF model tells a different story. It suggests fair value closer to $169 per share, about 36 percent above today’s price and implying the market may still be overly cautious.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out EchoStar for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 898 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own EchoStar Narrative

If you want to dig into the numbers yourself or challenge this view, you can build a personalized EchoStar story in minutes: Do it your way.

A great starting point for your EchoStar research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

If EchoStar has sharpened your appetite for opportunity, do not stop here. Your next market win could be hiding in plain sight on another stock screen.

- Capture potential multi baggers early by targeting these 3629 penny stocks with strong financials that pair tiny market caps with robust balance sheets and clear earnings trajectories.

- Explore structural tech trends by reviewing these 24 AI penny stocks involved in automation, intelligent infrastructure, and next generation software platforms.

- Seek income and capital resilience through these 10 dividend stocks with yields > 3% that combine established payout histories with cash flow coverage supporting those distributions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if EchoStar might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SATS

EchoStar

Provides networking technologies and services in the United States and internationally.

Fair value with very low risk.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion