Advertisement

- United States

- /

- Media

- /

- NasdaqGS:SATS

EchoStar (SATS): Evaluating Valuation After AT&T’s Nationwide 5G Spectrum Deployment Deal

Simply Wall St

Reviewed by Simply Wall St

EchoStar (SATS) shares drew attention after AT&T announced the nationwide deployment of mid-band spectrum acquired from EchoStar. This move focuses on maximizing network potential and monetizing spectrum assets, which matters for investors.

See our latest analysis for EchoStar.

EchoStar’s rapid appreciation is not just a flash in the pan. Its 18.6% 90-day share price return and eye-catching 222.2% year-to-date gain suggest strong momentum has been building, particularly as the AT&T spectrum deal highlights the value of EchoStar’s assets. Over the long haul, total shareholder returns have outpaced the stock’s own price rise, underscoring substantial value creation.

If this kind of growth story resonates, it might be the perfect moment to discover fast growing stocks with high insider ownership

With EchoStar’s shares soaring and the AT&T deal underscoring its strategic assets, the key question for investors is whether EchoStar stock remains undervalued, or if the latest rally has already factored in all the future growth potential.

Most Popular Narrative: 8.2% Undervalued

The most followed narrative sets EchoStar’s fair value above the last close, implying the stock still has upside if current assumptions hold. Explore why this view is gathering attention among analysts and investors.

EchoStar's investment in a unique wideband LEO direct-to-device satellite constellation, leveraging its global S-band and AWS-4 spectrum rights, positions it to address skyrocketing global demand for ubiquitous connectivity across consumer, enterprise, government, and IoT applications. This is likely to create new, high-margin wholesale revenue streams and accelerate long-term revenue growth. The company's strong strategic focus on integrating terrestrial 5G access with non-terrestrial (satellite) networks enables differentiated, seamless global connectivity that appeals to carriers seeking to provide comprehensive coverage. This supports higher ARPU, lower churn, and improved customer stickiness, positively impacting net margins as the ecosystem matures.

Want to see what’s driving this fair value? The narrative builds its case on bold growth assumptions and a profit trajectory that could change the game. Curious about which deep-dive analyst models back this projection? The full narrative breaks down the crucial quantitative bets and transformative catalysts behind the price target. Don’t miss out. Find out what could push EchoStar even higher.

Result: Fair Value of $79.83 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing regulatory uncertainty and EchoStar's significant near-term debt maturities could quickly undermine the optimistic growth outlook if not carefully managed.

Find out about the key risks to this EchoStar narrative.

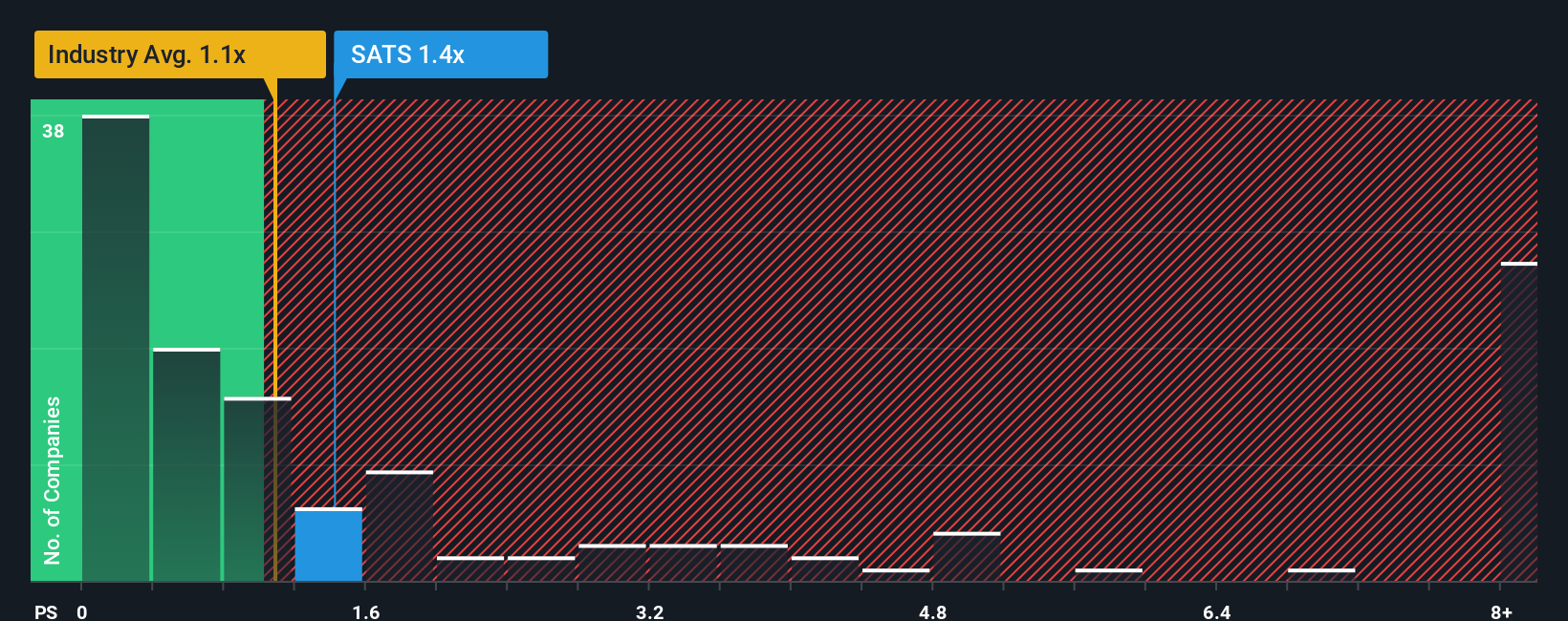

Another View: Valuing EchoStar by Price-to-Sales

Looking from a different angle, EchoStar’s current price-to-sales ratio of 1.4x stands above both the US media industry average (1.1x) and the fair ratio of 1.3x. This means the market is valuing EchoStar higher than its peers and above what regression analysis suggests is justified. This may increase the risk for investors if expectations are not met. Could this premium be a sign of lasting growth potential, or is it simply a warning to tread carefully?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own EchoStar Narrative

If you see things differently, or prefer to craft your own perspective, you can dive in and shape a custom EchoStar thesis in just a few minutes: Do it your way

A great starting point for your EchoStar research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors never settle for just one opportunity. Expand your portfolio beyond EchoStar by checking out these standout stock screens and seize your next win before others do.

- Uncover resilient income streams by targeting high-yield opportunities in these 15 dividend stocks with yields > 3% and fortify your returns for the long term.

- Ride the AI innovation surge and capitalize on exponential growth with these 25 AI penny stocks before the market catches on.

- Catch tomorrow’s leaders early and build wealth from the ground up with a focused list of these 3572 penny stocks with strong financials.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EchoStar might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SATS

EchoStar

Provides networking technologies and services in the United States and internationally.

Fair value with very low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative