Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:META

Meta Platforms (META) Margin Compression Challenges Bullish Growth Narratives In FY 2025 Results

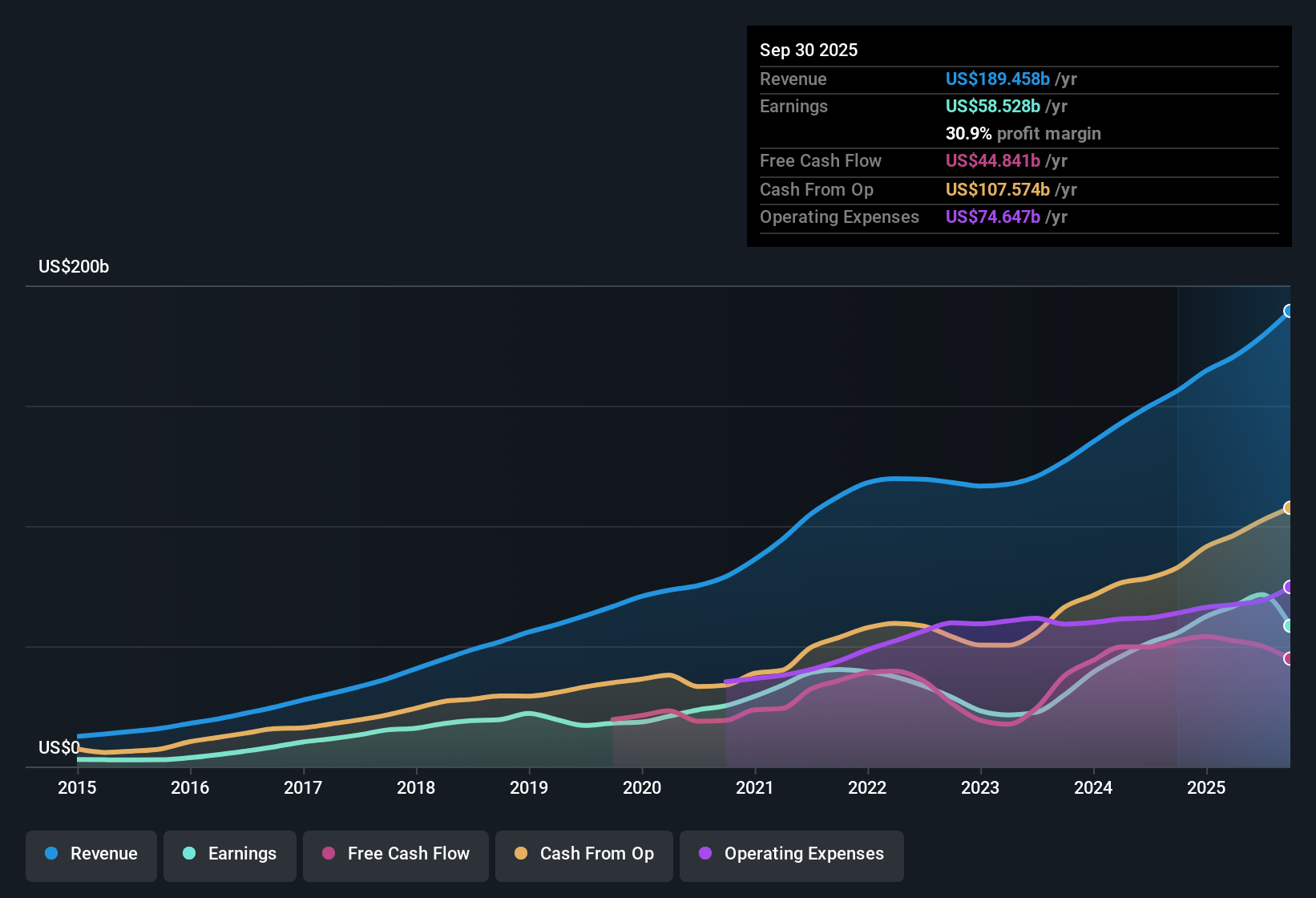

Meta Platforms FY 2025 earnings snapshot

Meta Platforms (META) has wrapped up FY 2025 with fourth quarter revenue of about US$59.9b and basic EPS of US$9.02, alongside net income of roughly US$22.8b. The latest twelve month figures show total revenue of about US$201.0b with basic EPS of US$23.98 and net income of around US$60.5b. The company has seen quarterly revenue move from roughly US$48.4b and EPS of US$8.24 in Q4 2024 to about US$59.9b and EPS of US$9.02 in Q4 2025, with trailing net margin sitting at 30.1%. This puts profitability and its recent compression in clear focus for investors weighing the current earnings print.

See our full analysis for Meta Platforms.With the headline numbers on the table, the next step is to see how this earnings profile lines up against the most widely held narratives around Meta, highlighting where the story fits the expectations and where the data challenges them.

Curious how numbers become stories that shape markets? Explore Community Narratives

Net margin slides from 37.9% to 30.1%

- Meta’s trailing net profit margin is 30.1%, compared with 37.9% a year earlier, on trailing twelve month revenue of about US$201.0b and net income of around US$60.5b.

- Critics highlight margin pressure as a bearish angle, and the 7.8 percentage point shift in net margin gives that view clear support, even though trailing twelve month net income of roughly US$60.5b and EPS of about US$23.98 still point to a sizeable profit base.

- Bears can point to the margin move from 37.9% to 30.1% as evidence that costs are taking a larger share of roughly US$201.0b of trailing revenue.

- At the same time, the earnings profile over the last five years, with average earnings growth of 16.8% per year, shows that the business has produced growing profits over a longer stretch, which softens the most pessimistic margin concerns.

Revenue growth forecasts outpace the US market

- Revenue is forecast to grow about 13.9% per year, compared with an expected 10.6% per year for the US market, while trailing twelve month revenue sits around US$201.0b.

- Supporters of a bullish view often lean on the idea that Meta’s scale can keep revenue expanding, and the 13.9% revenue growth forecast alongside a 14.8% earnings growth forecast lends weight to that, even as the recent drop in trailing margin to 30.1% shows that growth is not translating into wider profitability right now.

- For bulls, faster forecast revenue growth than the broader US market, at 13.9% versus 10.6%, lines up with the idea that the core business remains a strong growth engine.

- However, the same data set flags that trailing earnings growth over the most recent year was weaker than the five year average of 16.8% per year, which challenges a simple story that growth and profitability move in lockstep.

High P/E and DCF fair value send mixed pricing signals

- Meta trades on a trailing P/E of 30.8x, above the US Interactive Media & Services industry average of 15.8x and close to the peer average of 31.4x, while a DCF fair value of about US$1,058.33 sits roughly 30.2% above the current share price of US$738.31.

- What stands out is the tension between a valuation-based bearish concern about a 30.8x P/E that is far above the 15.8x industry average and a more optimistic take that points to the DCF fair value being meaningfully higher than the current price, with both views grounded in the same trailing earnings of about US$23.98 per share.

- Investors worried about an expensive stock can point to the P/E more than double the industry average, which implies the market is already paying a premium for the roughly US$60.5b of trailing net income.

- Investors who focus on cash flow models instead will notice that the DCF fair value of about US$1,058.33 is well above the current US$738.31 share price, which is cited as a reward signal in the analysis.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Meta Platforms's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Meta combines a sliding net margin with a P/E well above its industry average, which raises clear questions about paying a premium for its earnings.

If that premium makes you uneasy, use these 865 undervalued stocks based on cash flows today to focus on companies where pricing looks more conservative relative to their cash flows and earnings power.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:META

Meta Platforms

Engages in the development of products that enable people to connect and share with friends and family through mobile devices, personal computers, virtual reality (VR) headsets, and AI glasses in the United States, Canada, Europe, Asia-Pacific, and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

61 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3219.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GaryB on Palantir Technologies ·

Palantir hits 52 week low.

Fair Value:US$274.861.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

North49_ on iShares - iShares MSCI South Korea ETF ·

EWY:US NYSE Arca iShares Msci South Korea ETF, an opportunity to diversify your tech investments.

Fair Value:US$273.4525.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative