Advertisement

- United States

- /

- Entertainment

- /

- NasdaqGS:ATVI

Activision Blizzard's (NASDAQ:ATVI) Growth Prospects Have Shrunk

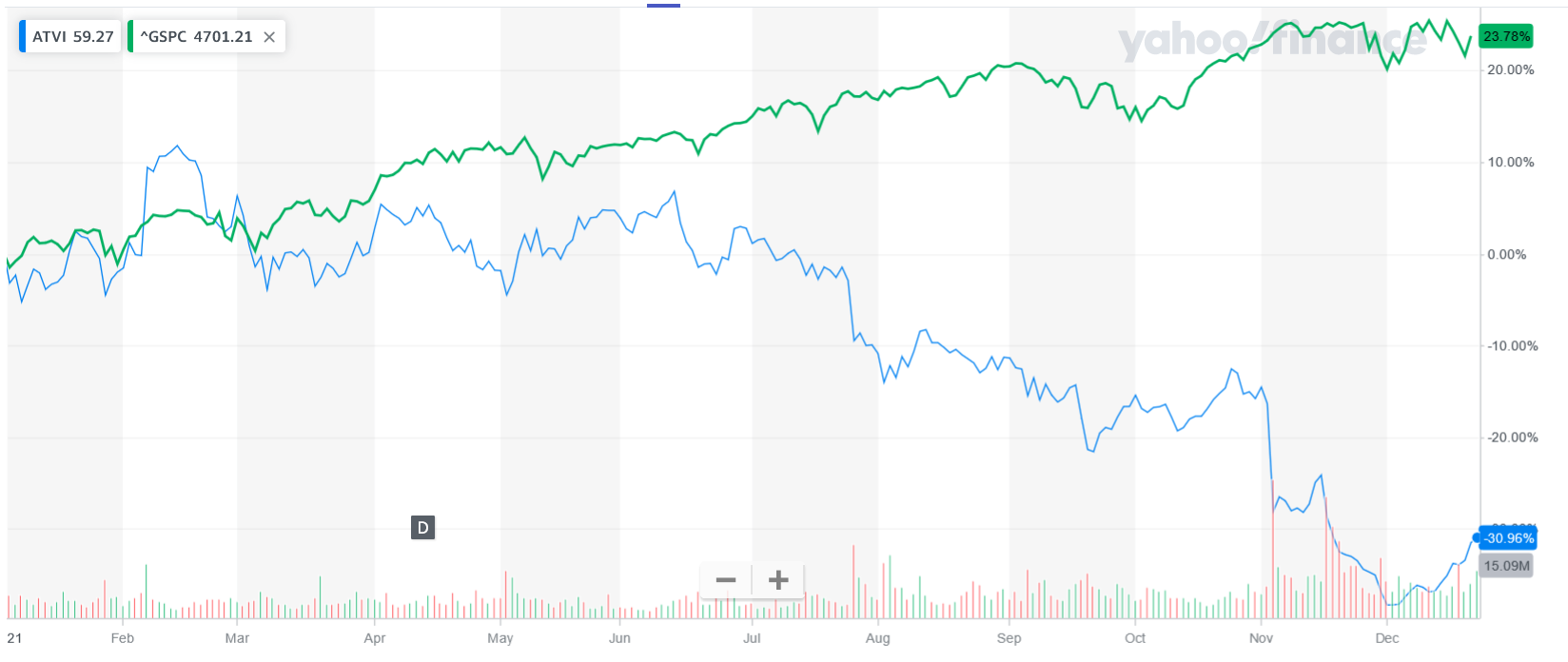

Despite favorable sector developments, Activision Blizzard, Inc. (NASDAQ: ATVI) had a lackluster year as the stock declined by over 30%. Plagued by delays and scandals, the stock does look undervalued at the moment – at least for those who believe in management turnarounds.

View our latest analysis for Activision Blizzard

Latest Developments

Stifel Nicolaus (NYSE: SF) just removed the company from its select list, unsatisfied with the workplace turmoil. Their analyst Drew Crum lowered the price target to US$77 from US$95, quoting negative sentiment regarding the company's leadership. As of yesterday, the stock closed at US$64.10.

This was just one of the cuts, as one month ago, J.P.Morgan reduced the rating from Overweight to Neutral, with a price target of US$88.

For some, price declines are opportunities, as L1 Capital International took a position in ATVI. They set the negative short-term sentiment aside and focused on the long-term franchise value.

Meanwhile, the market is still waiting for the company's management to start making changes. So far, the company stated that they're working on improving the gender/diversity representation as employees identifying as women make up only 24% of the workforce.

With the P/E ratio of 18.83, the stock trades way below its historical averages, and the divergence between it and the broad market is best shown through this chart.

For those optimistic about resolving this crisis, this situation presents an exciting opportunity as the video game market is expected to grow at the compounded annual growth rate (CAGR) of 13.2% over the next several years.

Estimating the Value of ATVI

We will be using the Discounted Cash Flow (DCF) model for our analysis.

We're using the 2-stage growth model, which means we take two stages of the company's growth. In the initial period, the company may have a higher growth rate, and the second stage is usually assumed to have a stable growth rate.

Where possible, we use analyst estimates, but when these aren't available, we extrapolate the previous free cash flow (FCF) from the last estimate or reported value. We assume companies with shrinking free cash flow will slow their rate of shrinkage and that companies with growing free cash flow will see their growth rate slow over this period.

A DCF is all about the idea that a dollar in the future is less valuable than a dollar today, and so the sum of these future cash flows is then discounted to today's value:

10-year free cash flow (FCF) estimate

| 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | |

| Levered FCF ($, Millions) | US$3.01b | US$3.59b | US$3.40b | US$3.08b | US$2.90b | US$2.80b | US$2.75b | US$2.73b | US$2.73b | US$2.75b |

| Growth Rate Estimate Source | Analyst x16 | Analyst x14 | Analyst x3 | Analyst x2 | Est @ -5.8% | Est @ -3.47% | Est @ -1.84% | Est @ -0.7% | Est @ 0.1% | Est @ 0.66% |

| Present Value ($, Millions) Discounted @ 6.4% | US$2.8k | US$3.2k | US$2.8k | US$2.4k | US$2.1k | US$1.9k | US$1.8k | US$1.7k | US$1.6k | US$1.5k |

("Est" = FCF growth rate estimated by Simply Wall St)

Present Value of 10-year Cash Flow (PVCF) = US$22b

The second stage is also known as Terminal Value. This is the business's cash flow after the first stage. For a number of reasons, a very conservative growth rate is used that cannot exceed that of a country's GDP growth. In this case, we have used the 5-year average of the 10-year government bond yield (2.0%) to estimate future growth. In the same way, as with the 10-year 'growth' period, we discount future cash flows to today's value, using a cost of equity of 6.4%.

Terminal Value (TV)= FCF2031 × (1 + g) ÷ (r – g) = US$2.8b× (1 + 2.0%) ÷ (6.4%– 2.0%) = US$63b

Present Value of Terminal Value (PVTV)= TV / (1 + r)10= US$63b÷ ( 1 + 6.4%)10= US$34b

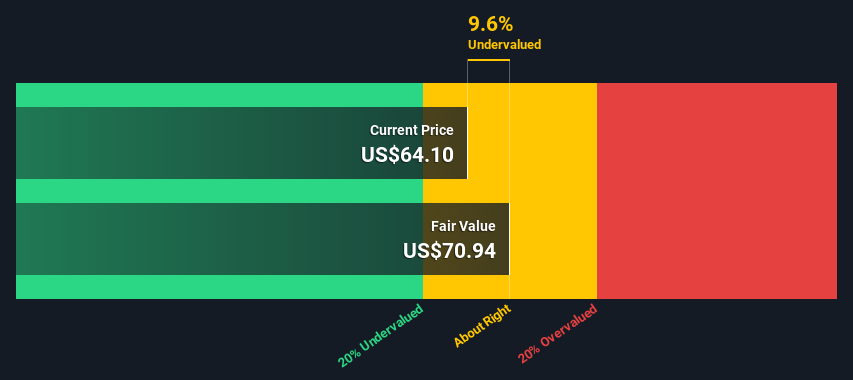

The total value, or equity value, is then the sum of the present value of the future cash flows, which in this case is US$55b. We divide the equity value by the number of shares outstanding in the final step. Compared to the current share price of US$64.1, the company appears about fair value at a 9.6% discount to where the stock price trades currently.

Important assumptions

The most important inputs to a discounted cash flow are the discount rate, and of course, the actual cash flows. The DCF does not consider the possible cyclicality of an industry or a company's future capital requirements, so it does not give a full picture of its potential performance.

Given that we are looking at Activision Blizzard as potential shareholders, the cost of equity is used as the discount rate rather than the cost of capital (or a weighted average cost of capital, WACC), which accounts for debt. We've used 6.4% in this calculation, which is based on a levered beta of 1.023. Beta is a measure of a stock's volatility compared to the market as a whole.

Moving On:

While the company trades at very low valuations compared to its historical averages, our valuation model doesn't see it significantly undervalued. If you check the future growth forecasts on our platform, you might notice that the company is expected to substantially underperform the industry's growth, according to the consensus of 29 analysts.

Meanwhile, the company's management needs to take decisive actions instead of relying on PR statements which looks like trying to extinguish a forest fire with one bucket of water.

There is more to stock research than valuations. For Activision Blizzard, we've put together three fundamental factors you should look at:

- Risks: As an example, we've found 1 warning sign for Activision Blizzard that you need to consider before investing here.

- Future Earnings: How does ATVI's growth rate compare to its peers and the wider market? Dig deeper into the analyst consensus number for the upcoming years by interacting with our free analyst growth expectation chart.

- Other Solid Businesses: Low debt, high returns on equity, and good past performance are fundamental to a strong business. Why not explore our interactive list of stocks with solid business fundamentals to see if there are other companies you may not have considered!

PS. The Simply Wall St app conducts a discounted cash flow valuation for every stock on the NASDAQGS every day. If you want to find the calculation for other stocks, just search here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NasdaqGS:ATVI

Activision Blizzard

Activision Blizzard, Inc., together with its subsidiaries, develops and publishes interactive entertainment content and services in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor