- United States

- /

- Basic Materials

- /

- NYSE:VMC

Vulcan Materials (VMC): Evaluating Valuation After Q3 2025 Aggregates Surge and Infrastructure-Driven Cash Flow Gains

Reviewed by Simply Wall St

Vulcan Materials (VMC) just posted a 12% jump in Q3 2025 aggregates shipments, along with better pricing and a 31% lift in operating cash flow, underscoring how infrastructure spending is quietly powering the stock.

See our latest analysis for Vulcan Materials.

At a share price of $288.34, Vulcan’s roughly 13% year to date share price return and strong three year total shareholder return of about 68% suggest momentum is still intact, with recent Q3 execution reinforcing the long term infrastructure story despite modest near term pullbacks.

If Vulcan’s infrastructure fueled run has you thinking about where else durable growth could come from, it is worth exploring fast growing stocks with high insider ownership as a curated way to spot the next wave of compounders.

With the stock trading about 11% below consensus targets but near record highs on robust earnings and infrastructure tailwinds, the real question now is whether Vulcan is still a buy or if markets already see the next leg of growth coming.

Most Popular Narrative Narrative: 9.2% Undervalued

With Vulcan Materials last closing at $288.34 versus a narrative fair value of $317.70, the prevailing view prices in more upside ahead.

Structural tailwinds from infrastructure resilience and the transition to green/renewable projects are driving long-term demand for aggregates in roads, storm-resistant infrastructure, and energy sites, enhancing Vulcan's long-term volume outlook and supporting higher blended pricing, which should lift both top-line revenue and profitability.

Curious how this demand story turns into a premium valuation multiple and richer margins over time, without heroic growth assumptions, or tech style forecasts, baked in?

Result: Fair Value of $317.70 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, delayed residential recovery and heavier reliance on Southeast infrastructure funding could pressure aggregate volumes and margins, challenging today’s upbeat growth narrative.

Find out about the key risks to this Vulcan Materials narrative.

Another Lens On Value

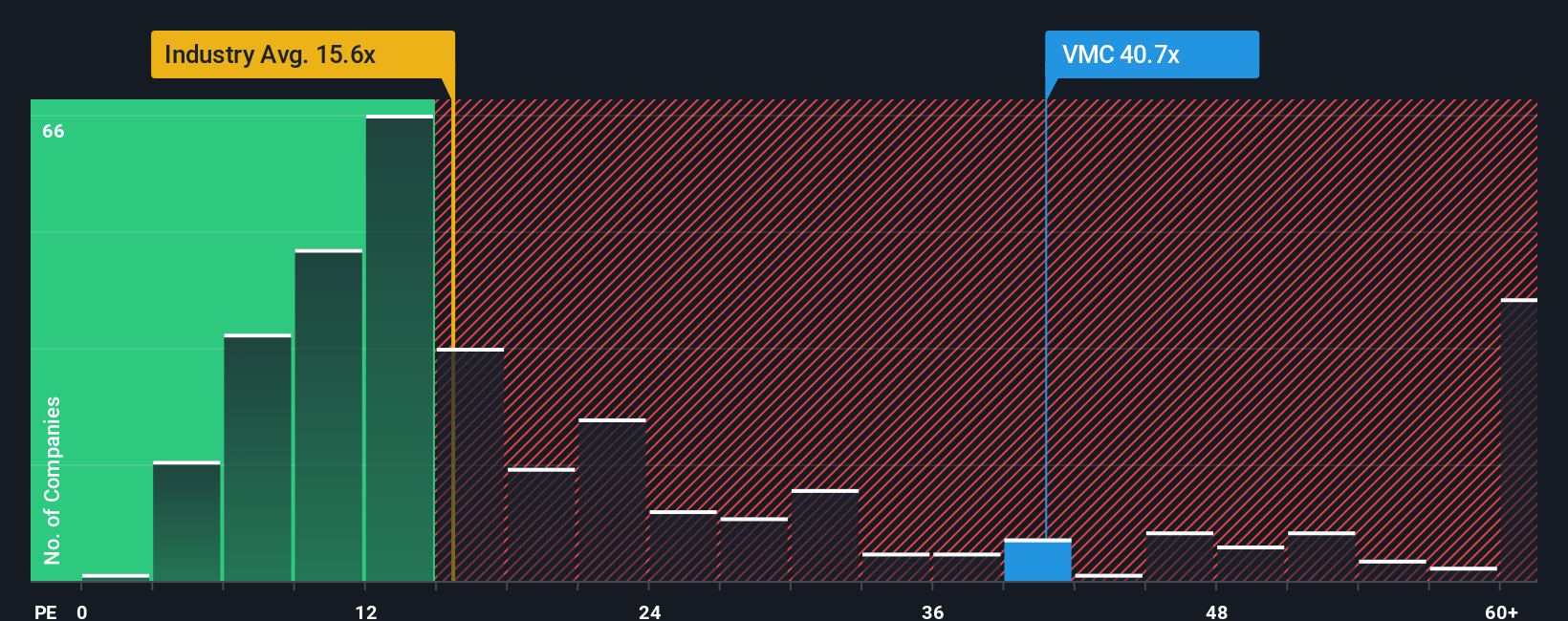

While the narrative fair value points to upside, our earnings based view tells a cooler story. Vulcan trades on a price to earnings ratio of 33.9x, compared with a 25.3x peer average, 15.1x for the broader basic materials space, and a fair ratio of 23.5x. This suggests clear valuation risk if sentiment cools. Is the market paying too much for visibility rather than growth?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Vulcan Materials Narrative

If you see the story differently or want to dig into the numbers yourself, you can craft a personalized view in minutes: Do it your way.

A great starting point for your Vulcan Materials research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready to hunt for your next opportunity?

Put Vulcan in context by lining it up against fresh ideas on the Simply Wall St Screener, before the next leg of this market passes you by.

- Capture potential bargains early by targeting companies the market may be mispricing through these 916 undervalued stocks based on cash flows and build a watchlist before sentiment shifts.

- Capitalize on innovation by tracking fast moving names shaping automation, data, and smarter software with these 24 AI penny stocks while the trend is still building.

- Lock in reliable cash returns by scanning for steady payers via these 13 dividend stocks with yields > 3% and avoid scrambling for income when yields compress.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VMC

Vulcan Materials

Produces and supplies construction aggregates in the United States.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion