Advertisement

- United States

- /

- Basic Materials

- /

- NYSE:VMC

Does Vulcan Materials’ Strong Q2 Growth Signal Sustained Margin Improvements for VMC?

Simply Wall St

Reviewed by Simply Wall St

- Vulcan Materials reported its second quarter 2025 results, posting sales of US$2.10 billion and net income of US$320.9 million, both higher than a year ago, along with increased basic and diluted earnings per share.

- An important insight from the report is that Vulcan Materials has shown consistent improvement in earnings metrics, reflecting ongoing operational performance enhancements.

- We'll take a closer look at how year-over-year growth in sales and profit shapes Vulcan Materials' current investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Vulcan Materials Investment Narrative Recap

To be a Vulcan Materials shareholder, you generally need to believe in sustained demand for U.S. construction aggregates and the company's ability to manage operating costs amid cyclical shifts in construction. The recent quarterly results reinforced this narrative by showing higher sales and profit year-over-year; however, while the performance was solid, it did not significantly alter the most important near-term catalyst, ongoing public infrastructure investment, or shift the biggest current risk, which remains uncertainty in private construction demand and interest rate trends.

Of the company's recent announcements, the affirmation of consistent quarterly dividends stands out for investors tracking cash returns during market volatility. As infrastructure activity is often slow-moving, these dividends can offer reassurance, yet they are closely tied to underlying earnings, which are still influenced by macroeconomic headwinds such as affordability and interest rate risks.

In contrast, there’s still one risk that investors cannot overlook...

Read the full narrative on Vulcan Materials (it's free!)

Vulcan Materials' narrative projects $9.6 billion revenue and $1.5 billion earnings by 2028. This requires 8.6% yearly revenue growth and a $555 million earnings increase from $944.9 million currently.

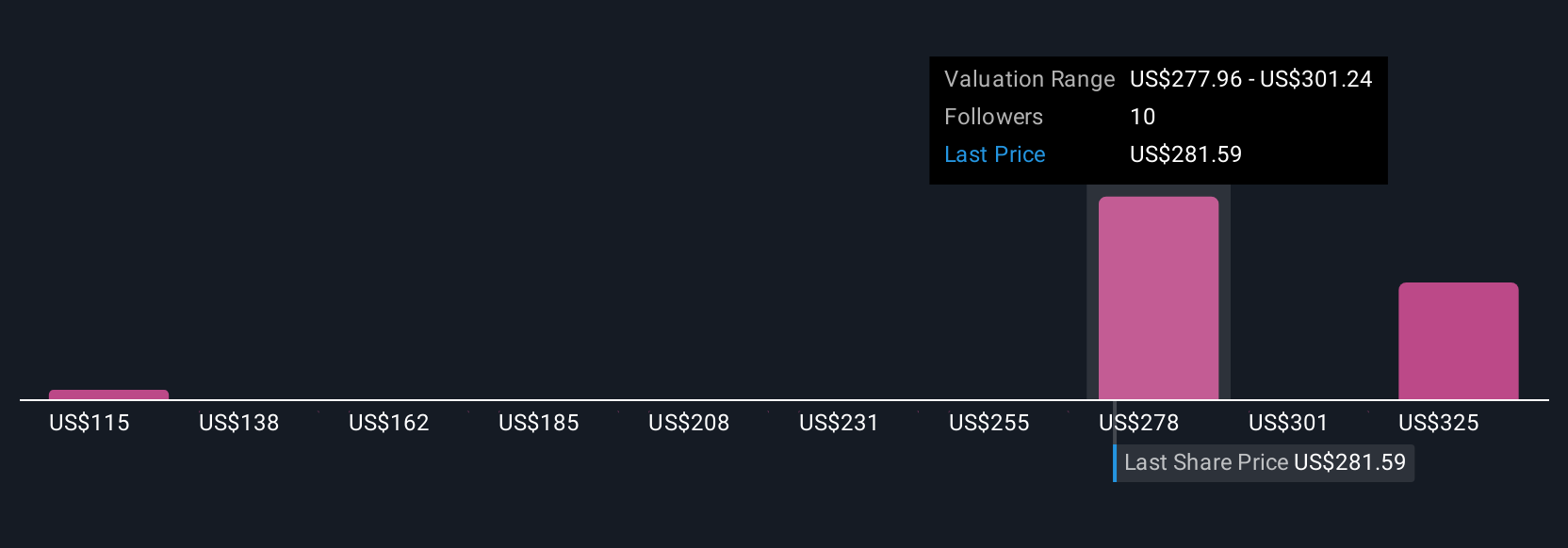

Uncover how Vulcan Materials' forecasts yield a $298.52 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community members placed fair value estimates between US$115 and US$373.99, reflecting wide differences in opinion. While infrastructure-related catalysts are boosting outlooks, uncertainty in private construction demand continues to shape expectations for Vulcan Materials’ future performance, explore how your view compares to others.

Explore 3 other fair value estimates on Vulcan Materials - why the stock might be worth less than half the current price!

Build Your Own Vulcan Materials Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Vulcan Materials research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Vulcan Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vulcan Materials' overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've found 22 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 25 companies in the world exploring or producing it. Find the list for free.

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VMC

Vulcan Materials

Produces and supplies construction aggregates in the United States.

Proven track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|57.7% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.6% undervalued

ZW

Community Contributor