Advertisement

- United States

- /

- Chemicals

- /

- NYSE:SHW

Sherwin-Williams (SHW) Valuation in Focus After CFO Transition and Earnings Update

Simply Wall St

Reviewed by Simply Wall St

Sherwin-Williams (NYSE:SHW) shares are in focus after the company announced a CFO transition. Allen J. Mistysyn is set to retire and Benjamin E. Meisenzahl will step into the role starting in January. Investors are also digesting fresh quarterly earnings and updated full-year guidance, both of which are key signals for the market.

See our latest analysis for Sherwin-Williams.

Following news of the upcoming CFO transition and a fresh earnings update, Sherwin-Williams shares have shown some short-term volatility but have not gained much ground. The stock is now trading at $340.16, and while the recent 1-day share price return of 1.95% suggests some optimism, the 1-year total shareholder return stands at -11.3%. This indicates that momentum has cooled off from previous strong performance. Over the longer term, holders have still seen robust compounding with a 3-year total shareholder return of 47.3%.

If steady performers like Sherwin-Williams have you rethinking your next move, it could be the perfect moment to broaden your horizons and discover fast growing stocks with high insider ownership

With the latest executive changes and earnings now digested, is Sherwin-Williams currently an overlooked value buy? Alternatively, are investors already fully pricing in its growth prospects for the years ahead?

Most Popular Narrative: 10% Undervalued

According to the most widely followed narrative, Sherwin-Williams’ fair value is $378.43, which is higher than its latest closing price of $340.16. Analysts believe the company’s strategic growth moves and margin improvements set the foundation for a recovery.

“Heightened investment in targeted customer-facing growth initiatives during a period of competitor retrenchment, layoffs, and price disruptions in the industry is likely to accelerate share gains with professional contractors and commercial projects. This supports long-term topline growth substantially above industry averages.”

Want to know which bold market assumptions are hidden beneath this premium? There is a profit growth play, margin expansion, and a multiple that rivals high-flying tech stocks. Uncover what really powers this fair value projection—it is not what you expect.

Result: Fair Value of $378.43 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent weak demand and continued margin pressure could derail Sherwin-Williams’ recovery story and put its fair value narrative at risk.

Find out about the key risks to this Sherwin-Williams narrative.

Another View: What Do the Numbers Say?

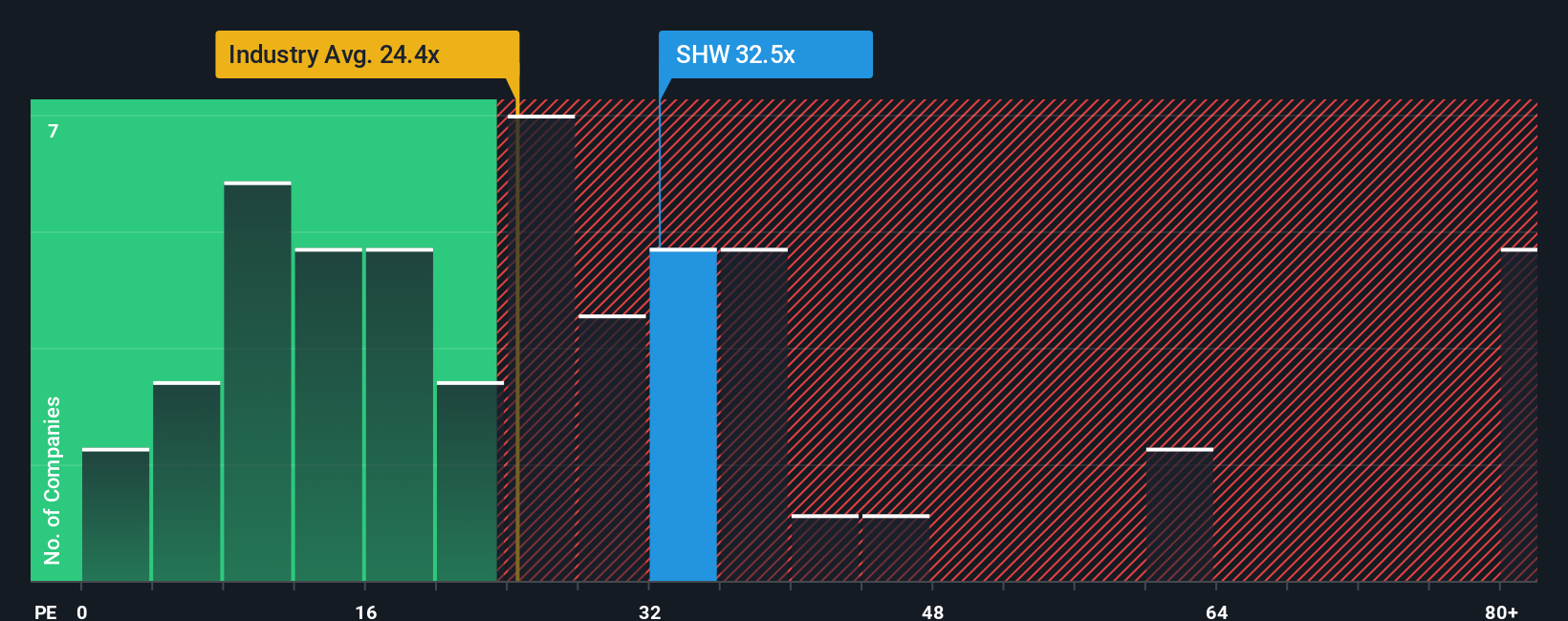

While the consensus suggests Sherwin-Williams is 10% undervalued, looking closer at its price-to-earnings ratio gives us pause. SHW is currently trading at 32.6x earnings, well above both the US Chemicals industry average (22.1x) and its fair ratio of 24.1x. This gap could indicate valuation risk. Are investors betting too much on a rebound, or is there something else justifying the premium?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Sherwin-Williams Narrative

If you think the story here is different or want to dig into the numbers yourself, you can build your own narrative in just a few minutes. Do it your way

A great starting point for your Sherwin-Williams research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Great opportunities are waiting if you look beyond the obvious. Tap into new trends and spot potential winners with powerful tools made for investors like you.

- Accelerate your hunt for rapid growth with these 24 AI penny stocks, which are redefining what is possible for tomorrow's technology leaders.

- Secure income potential right now by checking out these 16 dividend stocks with yields > 3%, featuring stocks with attractive yields and consistent returns.

- Capitalize on global transformation as you review these 27 quantum computing stocks, pushing the boundaries in advanced computation and industry innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SHW

Sherwin-Williams

Engages in the development, manufacture, distribution, and sale of paint, coatings, and related products to professional, industrial, commercial and retail customers.

Average dividend payer with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor