- United States

- /

- Chemicals

- /

- NYSE:SCL

Stepan (SCL): Deep Discount to Fair Value Fuels Bulls Despite Five-Year Earnings Decline

Reviewed by Simply Wall St

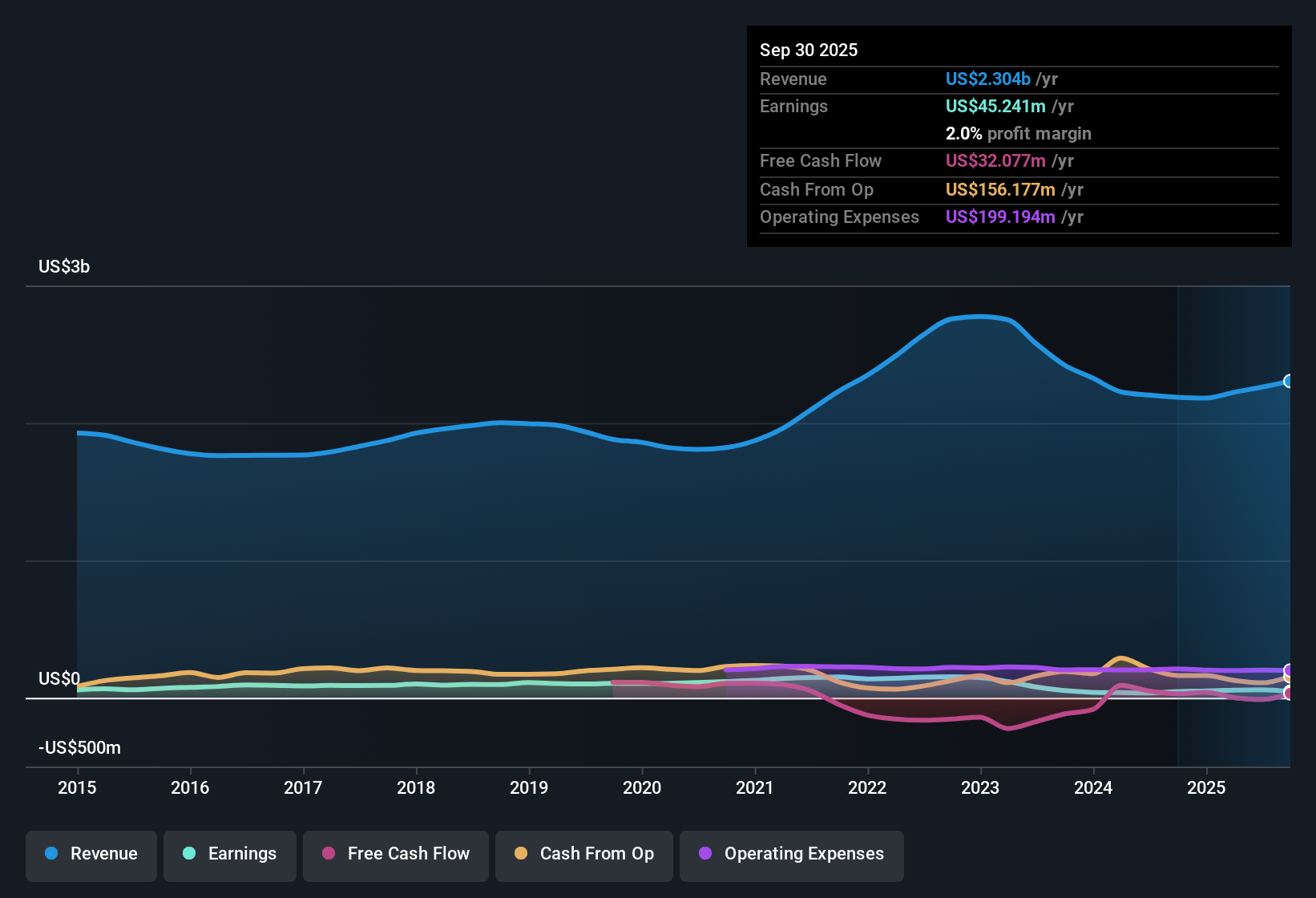

Stepan (SCL) reported that earnings have declined 26.1% per year over the last five years, and its current net profit margin is 2%, slightly below last year's 2.1%. Revenue is forecast to rise 5.3% annually, which trails the broader US market growth rate of 10.3%. However, earnings are projected to surge 53.4% per year, far ahead of the US average forecast of 15.7%. With valuation multiples below both industry and peer averages, investors may see recent trends as a setup for potential upside if the company hits its robust earnings growth projections.

See our full analysis for Stepan.The next section compares these headline results to the prevailing narratives around Stepan, spotlighting where consensus holds up and where the latest numbers might upend market expectations.

See what the community is saying about Stepan

Margins Poised for a Turnaround

- Analysts expect Stepan’s profit margin to more than double from the current 2.5% to 5.6% in three years, even though recent historical margins were flat to slightly down.

- According to the analysts' consensus view, this improvement is driven by:

- Strong growth in specialty alkoxylation, which was up 19% in Q1, and a more profitable mix in the Surfactants segment, supported by high-margin new customers and broader industry demand.

- The Pasadena site is scheduled to come online in late 2025. Consensus expects this will increase volumes and provide better supply chain leverage, both crucial for margin recovery.

- Consensus narrative makes the case that this fundamental turnaround depends on maintaining cost control as input prices and competitive pressures rise.

What may surprise some investors is how quickly the story could change if these segment-level improvements deliver as forecast. Analysts across the board are already including higher profitability in their long-range models. 📊 Read the full Stepan Consensus Narrative.

Cash Flow Watch: Risks Linger Despite Growth Forecasts

- Stepan reported negative free cash flow of $25.8 million, reflecting pressures from higher working capital needs and increased raw material purchases even as revenue growth is expected to improve.

- Critics highlight within the consensus narrative that:

- While new customer wins and volume gains in key sectors bode well for top-line growth, persistent raw material cost inflation and macroeconomic headwinds could limit the positive impact on cash conversion.

- The ability to manage pass-through of costs in areas like Surfactants and to address pricing pressures in Polymers will be vital for restoring cash flow, a point that gives bears plenty to monitor if improvement stalls.

Valuation Still at a Discount to Peers

- Stepan trades at a price-to-earnings ratio of 21.5x, notably lower than both the US chemicals industry average of 26.7x and its peer group at 37.4x, despite robust earnings growth projections for the next three years.

- Consensus narrative points out that:

- Good relative value is reinforced by the current share price ($42.92) trading well below the DCF fair value estimate of $128.84, making the stock appear discounted on both peer comparison and intrinsic value.

- This creates a margin of safety for investors who believe in the long-term catalysts, including the success of new facilities and steady improvements in profit margin and revenue growth.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Stepan on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Looking at the results from another angle? Shape your own view on Stepan in just a few minutes and join the discussion. Do it your way

A great starting point for your Stepan research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Despite strong earnings growth forecasts, Stepan’s volatile cash flow and margin pressures signal ongoing vulnerability to rising costs and economic headwinds.

If steady performance is your priority, use our stable growth stocks screener (2095 results) to focus on companies that consistently deliver reliable growth and resilient cash generation through changing conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SCL

Stepan

Produces and sells specialty and intermediate chemicals to other manufacturers for use in various end products worldwide.

Good value with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Meta’s Bold Bet on AI Pays Off

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Visa Stock: The Toll Booth at the Center of Global Commerce

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion