Advertisement

- United States

- /

- Chemicals

- /

- NYSE:OLN

Will Olin's (OLN) Cost Controls Offset Demand Uncertainty in Its Evolving Investment Narrative?

Reviewed by Sasha Jovanovic

- Olin Corporation recently reported third-quarter 2025 earnings, returning to profitability with net income of US$42.8 million and sales of US$1.71 billion, but issued significantly lower guidance for the fourth quarter citing seasonal weakness, inventory reductions, and subdued demand.

- Analysts highlighted that the earnings improvement was mainly attributable to gains in the Chlor Alkali Products and Vinyls segment as well as a US$32 million pretax benefit associated with a clean hydrogen production tax credit, while key headwinds emerged in the Winchester and Epoxy segments.

- Next, we'll consider how Olin's cautious Q4 forecast and efforts to optimize costs could influence its broader investment story and outlook.

Find companies with promising cash flow potential yet trading below their fair value.

Olin Investment Narrative Recap

To be a shareholder in Olin today, you need to believe that the company's cost optimization initiatives and strategic refocusing can overcome persistent pricing and demand pressures in its chemicals and ammunition businesses. The latest guidance for Q4, featuring substantially reduced EBITDA estimates and a clear acknowledgment of ongoing softness in demand, has put the spotlight on Olin’s ability to deliver tangible margin improvements, while the main short-term catalyst remains successful execution on cost reduction, and the biggest risk continues to be a prolonged global oversupply and weak pricing environment in chlor-alkali and vinyls. The recent update does not materially change these fundamental drivers, but elevates scrutiny of operational execution through what management warns is seasonally the weakest quarter.

Among the latest company actions, Olin announced the repurchase of 500,000 shares for US$10.1 million during the third quarter, finalizing just over 21% of the buyback program launched in mid-2022. This ongoing share repurchase effort is important as it signals confidence in capital return even as near-term earnings headwinds remain a concern for investors tracking progress on both catalysts and risks.

Yet unlike the market’s initial focus on low EDC prices, investors should also be aware of the risks posed by ongoing high inventories and weak demand in the Winchester ammunition segment...

Read the full narrative on Olin (it's free!)

Olin's outlook anticipates $7.4 billion in revenue and $375.3 million in earnings by 2028. This projection is based on an annual revenue growth rate of 3.6% and an increase in earnings of $389.4 million from the current level of -$14.1 million.

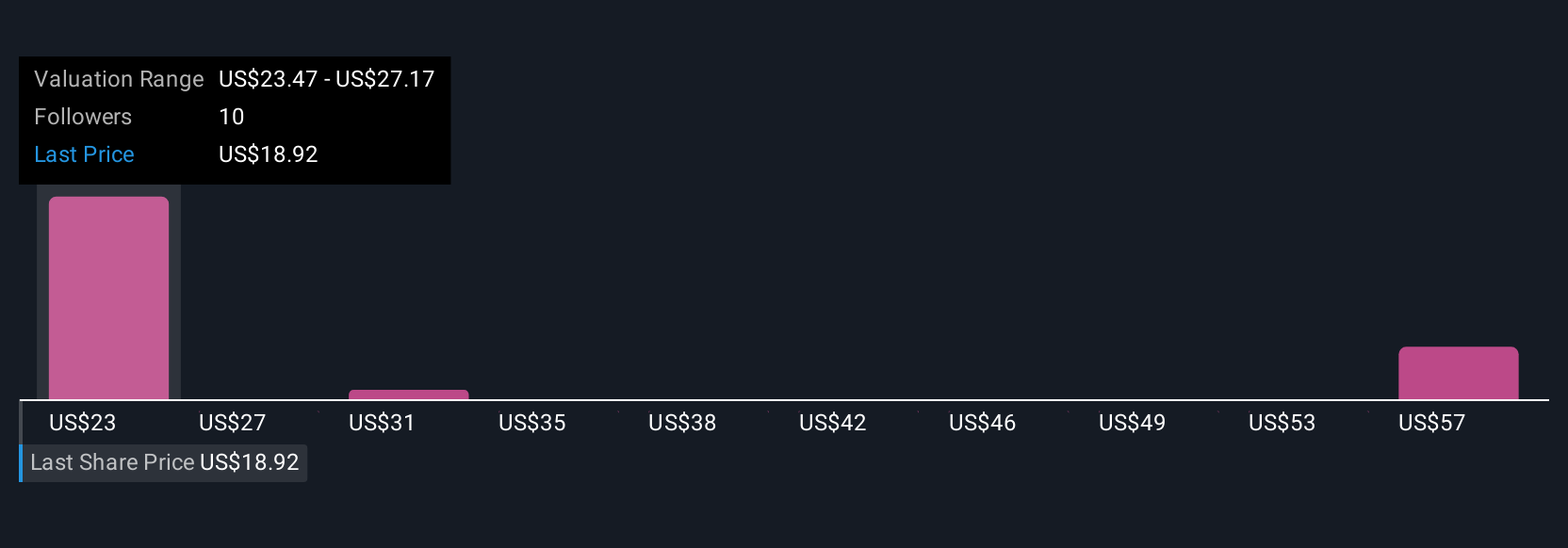

Uncover how Olin's forecasts yield a $24.73 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Five fair value estimates from the Simply Wall St Community range from US$24.73 to US$60.08, revealing a wide spectrum of investor opinions. With cost reduction still a key catalyst, this underscores how expectations for operational improvement drive differing outlooks on Olin’s future performance.

Explore 5 other fair value estimates on Olin - why the stock might be worth over 2x more than the current price!

Build Your Own Olin Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Olin research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Olin research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Olin's overall financial health at a glance.

No Opportunity In Olin?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:OLN

Olin

Manufactures and distributes chemical products in the United States, Europe, Asia Pacific, the Middle East, Africa, and India Middle East, Africa, India, Latin America, and Canada.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0778.3% undervalued

199 followersusers have followed this narrative

1 commentusers have commented on this narrative

28 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.4% undervalued

42 followersusers have followed this narrative

2 commentsusers have commented on this narrative

19 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0725.2% undervalued

6 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3819.4% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

HE

HedgeY on Constellium ·

Constellium jet another cyclical aluminum processor, or a mispriced aluminum platform?

Fair Value:US$3420.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Northern Solar Holdings Berhad ·

Northern Solar: Explosive earnings growth makes this solar story harder to ignore

Fair Value:RM 1.968.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

tripledub on SHAPE Australia ·

50% ROE in a Burning Building

Fair Value:AU$7.154.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9829.9% undervalued

53 followersusers have followed this narrative

0 commentsusers have commented on this narrative

38 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.7% undervalued

40 followersusers have followed this narrative

3 commentsusers have commented on this narrative

41 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

36 followersusers have followed this narrative

10 commentsusers have commented on this narrative

30 likesusers have liked this narrative