Advertisement

- United States

- /

- Metals and Mining

- /

- NYSE:MP

Why MP Materials (MP) Is Down 12.4% After Major Defense Partnership to Build US Rare Earth Supply Chain

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this month, MP Materials announced it has entered a multibillion-dollar public-private partnership with the U.S. Department of Defense to rapidly build a domestic rare earth magnet supply chain, including a new facility slated for commissioning in 2028 and expanded capabilities at Mountain Pass, California.

- This partnership aims to reduce foreign dependency, solidify MP Materials as a national strategic asset, and address escalating demand for rare earth materials in both defense and commercial sectors.

- We'll explore how government investment in a fully integrated U.S. rare earth magnet supply chain may reshape MP Materials' investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

MP Materials Investment Narrative Recap

For MP Materials shareholders, the core thesis centers on the company’s ability to capitalize on rising US demand for rare earth magnets, supported by government backing and long-term contracts. The newly announced multibillion-dollar public-private partnership with the Department of Defense bolsters near-term optimism for domestic capacity, but execution risks around large-scale facility ramp-up still represent the main short-term catalyst and risk; delays or cost overruns could quickly alter earnings visibility, making operational milestones especially important.

Of the recent announcements, the $500 million supply deal with Apple stands out, aligning with efforts to secure major anchor customers as MP scales up production. This kind of agreement, combined with policy support, has the potential to stabilize revenues but also highlights the company's exposure to customer concentration risks if any single partner’s priorities shift or contracts are renegotiated.

Yet, despite increased government support for MP Materials, investors should be aware that reliance on a small group of large customers could...

Read the full narrative on MP Materials (it's free!)

MP Materials' outlook anticipates $1.0 billion in revenue and $236.3 million in earnings by 2028. This scenario requires a 61.3% annual revenue growth and a $337.7 million increase in earnings from current earnings of -$101.4 million.

Uncover how MP Materials' forecasts yield a $80.71 fair value, a 14% upside to its current price.

Exploring Other Perspectives

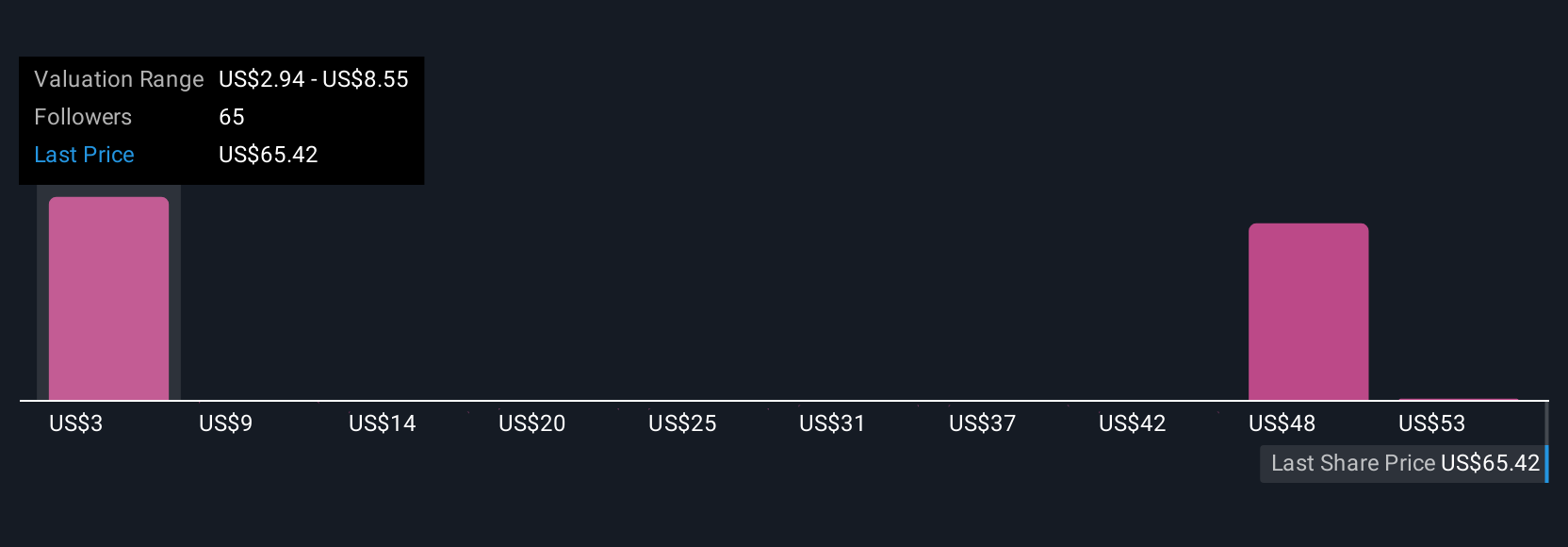

Across 24 different Simply Wall St Community fair value estimates for MP Materials, opinions range widely from US$2.34 to US$85 per share. While many expect government funding and price floors to drive more stable revenue, the company’s ability to manage expansion risks could determine how the share price ultimately tracks these contrasting expectations.

Explore 24 other fair value estimates on MP Materials - why the stock might be worth less than half the current price!

Build Your Own MP Materials Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your MP Materials research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free MP Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MP Materials' overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MP

High growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor