Martin Marietta Materials (MLM) stock has seen a slight uptick recently, capturing some investor attention as the company continues to deliver steady performance. Its presence in infrastructure and construction materials keeps it in focus for those tracking long-term industry trends.

Martin Marietta Materials has kept up its positive momentum, with the share price up more than 22% year-to-date and its three-year total shareholder return reaching an impressive 73%. Recent gains reflect ongoing optimism about long-term infrastructure spending and stable industry demand.

With shares rising steadily and performance figures impressing analysts, the key question remains: is Martin Marietta Materials undervalued at current levels, or has the market already accounted for its growth potential? Could this be a buying opportunity, or is future momentum priced in?

Advertisement

Most Popular Narrative: 6.5% Undervalued

The current narrative suggests Martin Marietta Materials may be trading below its fair value, as the narrative's fair value calculation outpaces the latest closing price. This difference is driven by strong forward growth projections and an expectation of expanding margins.

Ongoing adoption of advanced cost management, digital tools, and operational efficiency measures, evidenced by record improvements in gross and EBITDA margins, are likely to deliver sustained net margin expansion and higher profitability, even through cyclical slowdowns.

Want a peek behind the curtain? This narrative leans on bold expectations: accelerating earnings growth and margin expansion typically reserved for leaders in faster-moving industries. Hungry to find out which future forecasts give this company its valuation edge? Tap through to see what is setting the price target just above the current share price.

However, persistent affordability issues in residential construction or reduced government infrastructure spending could quickly challenge the positive outlook and growth assumptions for Martin Marietta Materials.

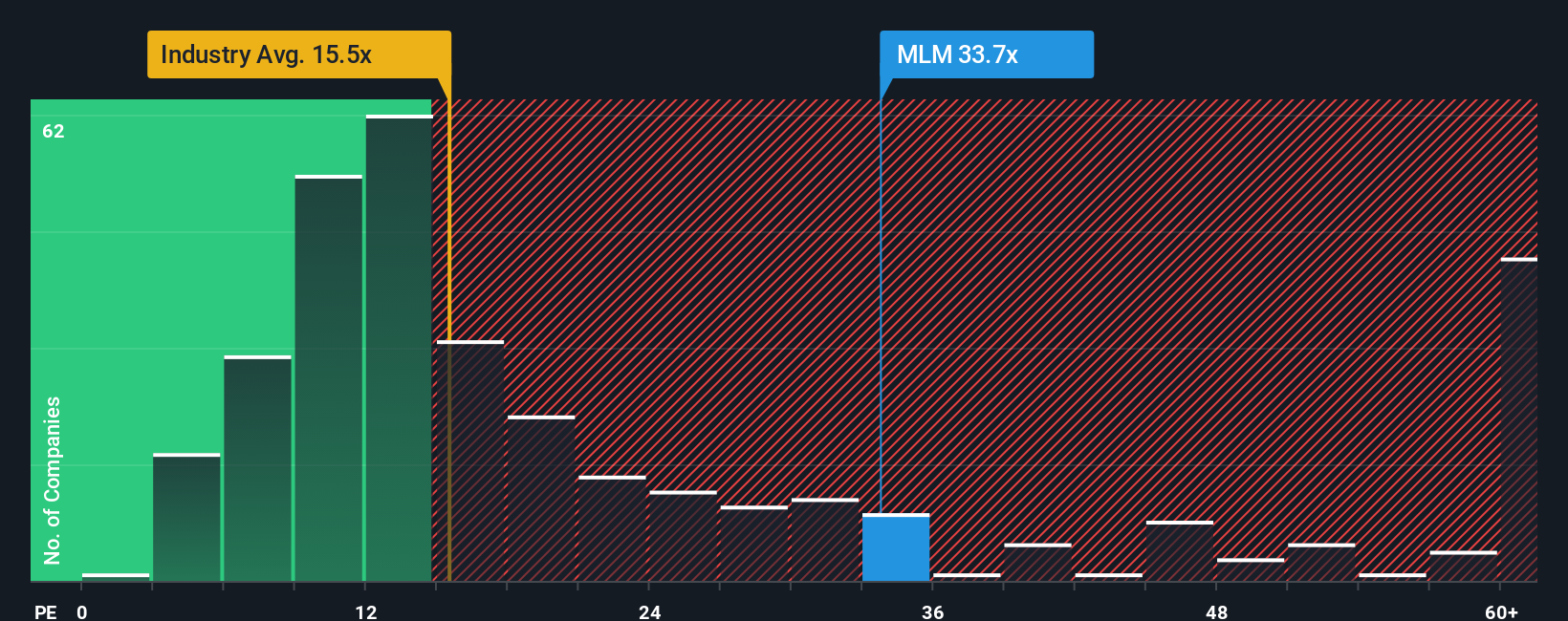

Another View: Do Multiples Tell a Different Story?

While the fair value model points to potential upside, looking at the company’s price-to-earnings multiple paints a less optimistic picture. Martin Marietta trades at 31.7x earnings, which is much higher than both the US Basic Materials industry average of 15x and peers at 25.8x, and well above its fair ratio of 22.9x. This premium suggests investors are pricing in a lot of growth, which might create valuation risk if expectations slip.

Build Your Own Martin Marietta Materials Narrative

If you have a different take or want to dig deeper into the numbers yourself, crafting your own perspective is quick and straightforward. Make your own in just a few minutes with Do it your way.

A great starting point for your Martin Marietta Materials research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don't limit your portfolio to just one opportunity. The market is full of promising stocks across innovative growth themes, and you’ll want to catch the best right now.

Supercharge your search by spotting tomorrow's disruptors among these 25 AI penny stocks as they ride the AI wave into new industries and applications.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

A natural resource-based building materials company, supplies aggregates and heavy-side building materials to the construction industry in the United States and internationally.