Advertisement

- United States

- /

- Metals and Mining

- /

- NYSE:HL

What Hecla Mining Company's (NYSE:HL) 41% Share Price Gain Is Not Telling You

Hecla Mining Company (NYSE:HL) shareholders would be excited to see that the share price has had a great month, posting a 41% gain and recovering from prior weakness. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 24% in the last twelve months.

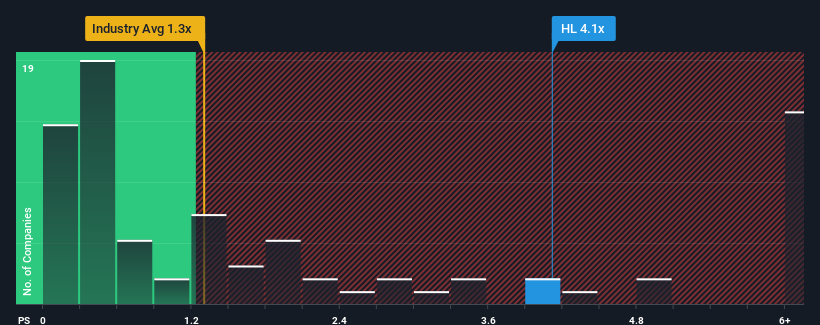

Following the firm bounce in price, given around half the companies in the United States' Metals and Mining industry have price-to-sales ratios (or "P/S") below 1.3x, you may consider Hecla Mining as a stock to avoid entirely with its 4.1x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

See our latest analysis for Hecla Mining

What Does Hecla Mining's Recent Performance Look Like?

Recent times have been pleasing for Hecla Mining as its revenue has risen in spite of the industry's average revenue going into reverse. The P/S ratio is probably high because investors think the company will continue to navigate the broader industry headwinds better than most. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Hecla Mining's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, Hecla Mining would need to produce outstanding growth that's well in excess of the industry.

If we review the last year of revenue, the company posted a result that saw barely any deviation from a year ago. Likewise, not much has changed from three years ago as revenue have been stuck during that whole time. So it seems apparent to us that the company has struggled to grow revenue meaningfully over that time.

Looking ahead now, revenue is anticipated to climb by 4.2% per year during the coming three years according to the seven analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 7.1% per annum, which is noticeably more attractive.

With this in consideration, we believe it doesn't make sense that Hecla Mining's P/S is outpacing its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

The strong share price surge has lead to Hecla Mining's P/S soaring as well. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've concluded that Hecla Mining currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Hecla Mining that you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Hecla Mining might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:HL

Hecla Mining

Provides precious and base metal properties in the United States, Canada, Japan, Korea, and China.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|35.9% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|15.6% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|2.5% overvalued

TO

Community Contributor