Advertisement

- United States

- /

- Chemicals

- /

- NYSE:ESI

Element Solutions (ESI) Stock May Trade Near Fair Value While Earnings Carry A Premium

Reviewed by Bailey Pemberton

Element Solutions stock has more than doubled over the last three years, yet its valuation checks send a mixed signal, with the Discounted Cash Flow (DCF) estimate pointing to a share price that sits close to intrinsic value while market multiples suggest the stock trades at a premium.

- Element Solutions has delivered a 145.4% return over three years, which puts added pressure on today's valuation to be supported by the business fundamentals rather than past share price gains alone.

- Expectations for steady cash generation from Element Solutions' specialty chemicals portfolio can support the current price, but any disappointment in margins or capital allocation may quickly influence how much investors are willing to pay.

- On Simply Wall St's broader checks, Element Solutions scores 0 out of 6 for value, which indicates the stock does not screen as a clear bargain right now.

The issue now is whether Element Solutions' strong three year run has already priced in most of its fundamentals, or if the current level still offers enough value for new investors coming in today.

Is Element Solutions Fairly Priced on Cash Flow?

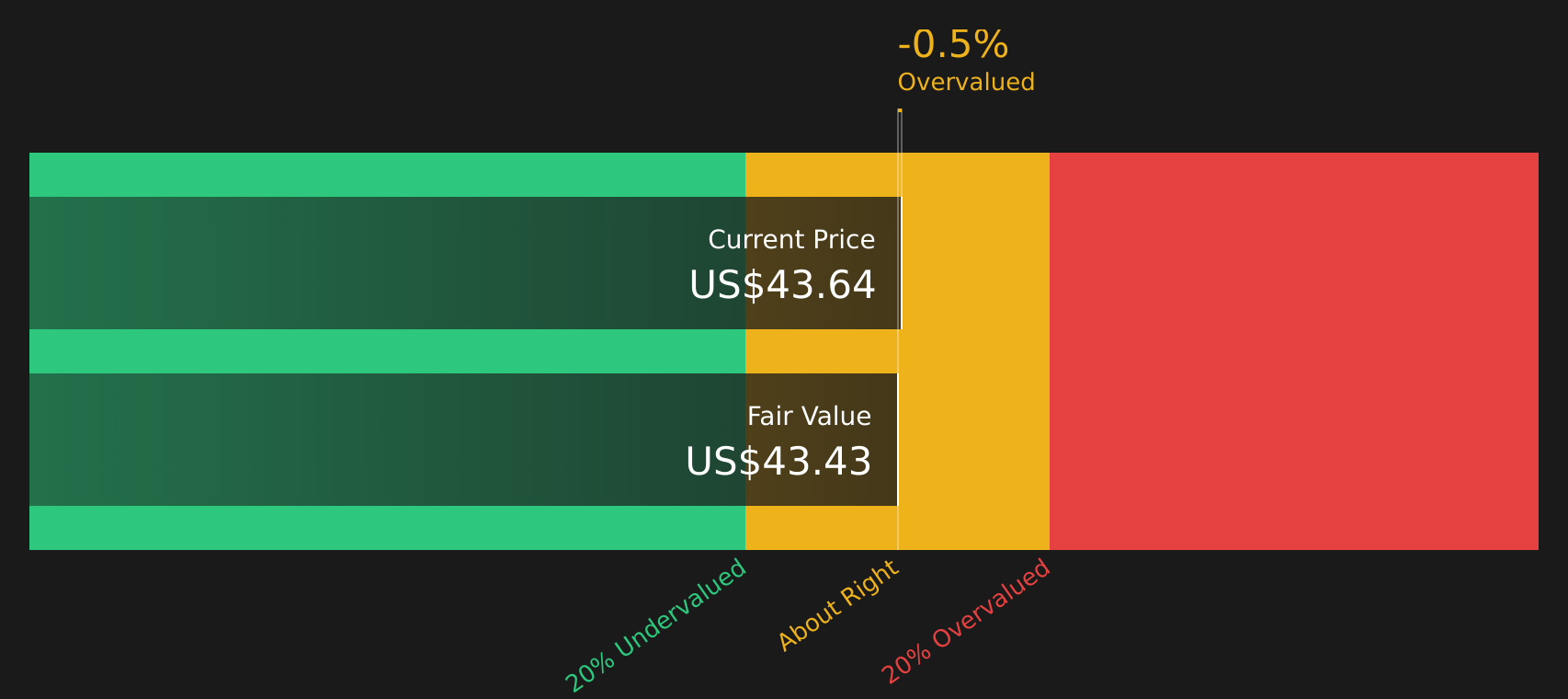

The Discounted Cash Flow (DCF) model estimates what Element Solutions is worth based on the cash it can generate for shareholders. On this view, the company is modeled with growing free cash flows, from latest twelve month free cash flow of about $123.9 million to higher levels over the coming years, using a 2 Stage Free Cash Flow to Equity approach.

Those projections translate into an estimated intrinsic value of about $43.36 per share. Compared with the current share price, the DCF output implies the stock is roughly 0.6% above that estimate, which is effectively a very small premium. For investors, that means the current market price for Element Solutions appears closely aligned with what its modeled cash generation supports rather than offering a clear discount or a clear excess.

On this cash flow view, Element Solutions stock appears to be approximately fairly valued at today’s price.

Element Solutions is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Is Element Solutions Getting Expensive on Earnings?

The P/E ratio is a common way to check what investors are willing to pay for each dollar of Element Solutions' earnings. Right now, the stock trades at about 71.5x earnings, which is well above the Chemicals industry average of roughly 25.7x and also higher than the peer group average of about 32.3x.

Simply Wall St's fair P/E estimate for Element Solutions, which reflects factors such as its industry, size and risk profile, is around 31.4x. That is less than half of the current multiple, indicating the market is assigning a relatively high price to the existing earnings base compared with what this framework would point to as a more typical level.

On the P/E lens, Element Solutions stock currently appears overvalued compared with both its sector and the modelled fair multiple.

See what the numbers say about this price — find out in our valuation breakdown.

The Element Solutions Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Element Solutions pick up where this valuation puzzle leaves off by spelling out the specific combinations of future growth, margins and earnings that would need to occur for the stock to look meaningfully cheaper or more expensive than it does today, based on frameworks shared on the Community page. Each narrative connects its number to a clear view of how Element Solutions' growth profile, profitability and key risks might evolve, giving you a reference point you can revisit as new information becomes available.

Share a narrative on Element Solutions to put your own number driven view on where its growth, margins and execution go from here, and see how that thesis stacks up as new results come through.

By adding your angle now, you can be one of the first voices in the Simply Wall St community that others refer back to as the Element Solutions story evolves.

Do you think there's more to the story for Element Solutions? Head over to our Community to see what others are saying!

The Bottom Line

For Element Solutions, the Discounted Cash Flow (DCF) work suggests the stock sits close to intrinsic value, so the bigger question is whether the earnings multiple premium can stay in place. Market pricing looks overvalued on P/E, which, together with the weaker value checks, implies you are paying up for the current earnings profile. The key swing factor from here is whether margins and cash generation can meet expectations strongly enough to justify that richer multiple, or whether sentiment cools and the valuation settles closer to sector norms.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Element Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ESI

Element Solutions

Operates as a specialty chemicals technology company in the United States, China, and internationally.

Moderate growth potential with questionable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.1% undervalued

73 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.7% undervalued

52 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

27 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32039.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EU

European_Hidden_Gem_Stocks on Creotech Instruments ·

$CRI Creotech Instruments (WSE:CRI): Two Minute Drill

Fair Value:zł822.191.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IV

Ivoed on LVMH Moët Hennessy - Louis Vuitton Société Européenne ·

LVMH’s Cash Flow Is Holding Up, But The Stock Still Needs A Better Entry Point

Fair Value:€5255.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

63 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0544.6% undervalued

55 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

Trending Discussion

NO

Nominal_Llama_qnhq on Kratos Defense & Security Solutions ·

Has anyone determined why many of the KTOS insiders are selling so much of their stock holdings. It...

0

|0