W. R. Berkley (WRB) has captured investor attention thanks to steady returns over the past year. The insurance company's shares have delivered gains both in the past month and over the past three months, outperforming many sector peers.

Momentum is clearly building for W. R. Berkley, with a 1.03% one-day share price gain and a robust 34.63% year-to-date price return showing renewed investor confidence. Over the long term, the insurance giant has delivered an impressive 203.11% total shareholder return over five years, making its outperformance tough to ignore.

If you’re interested in what other companies are demonstrating strong momentum, it could be the right moment to broaden your horizons and discover fast growing stocks with high insider ownership

But with shares running ahead of analyst price targets and solid gains already delivered, the big question is whether W. R. Berkley remains undervalued, or if the market is already pricing in all future growth potential.

Advertisement

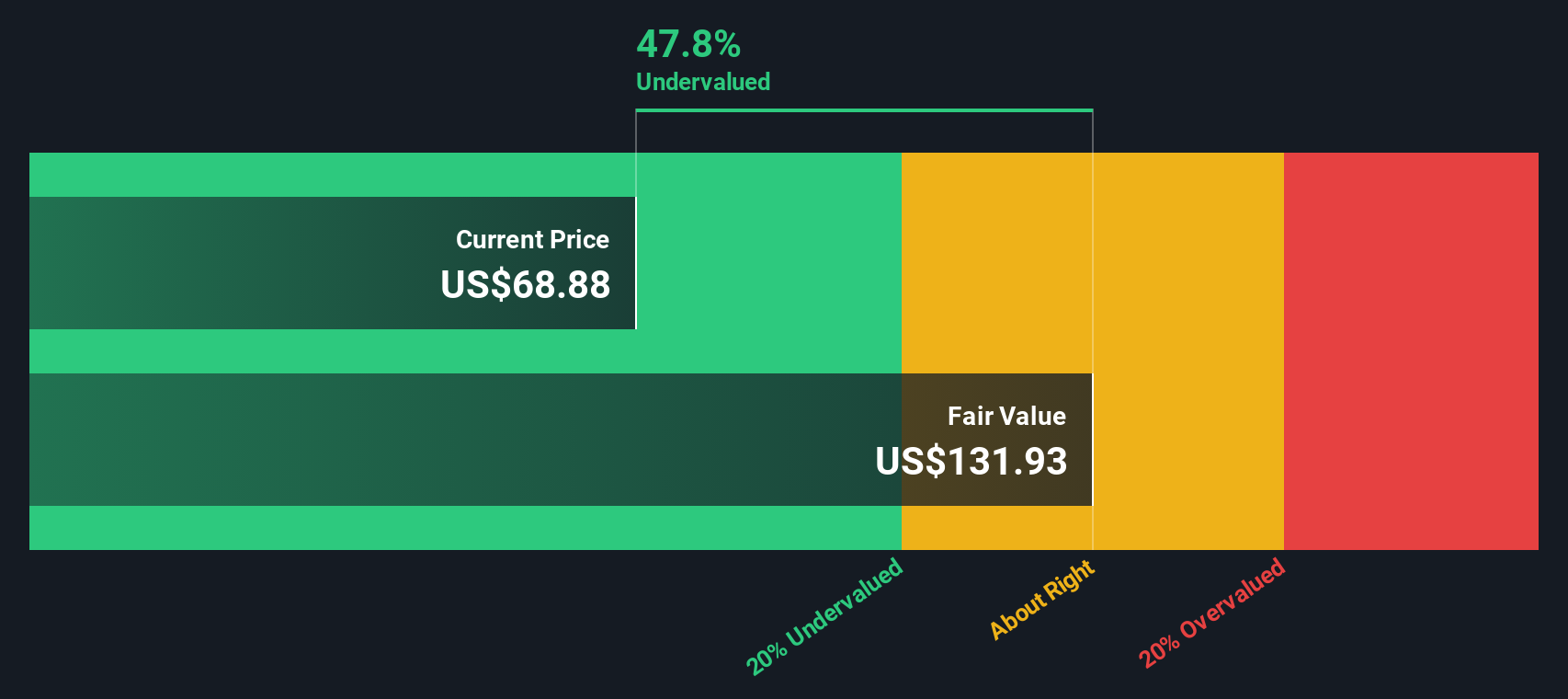

Most Popular Narrative: 5.3% Overvalued

According to the narrative’s fair value, W. R. Berkley’s recent close exceeds the analyst consensus price target, highlighting a premium in how the stock is currently trading. This points to tensions in expectations as investors weigh recent performance against forward-looking valuation frameworks.

“Prudent capital management, shown by a growing investment portfolio benefitting from higher new money yields and conservative reserving, is increasing investment income and book value per share. This lays a foundation for higher long-term earnings and the potential for resumed share buybacks.”

Want to know what’s fueling the company’s high valuation? The narrative’s fair value hinges on projected improvements in margins and profit multiples that challenge industry norms. Curious which bold assumptions and growth levers the analysts are betting on? Dive in to see what could push this stock even higher or spell a reversal.

However, persistent margin pressures and rising competition could quickly alter the outlook and push analysts to reassess fair value for W. R. Berkley.

Another View: Discounted Cash Flow Sheds New Light

While the consensus price target values W. R. Berkley above fair value, our SWS DCF model offers a very different perspective, suggesting the stock is actually trading at a hefty 34% discount to its intrinsic value. Could the market be missing the company’s long-term cash generation story?

If you have your own perspective on W. R. Berkley’s story or want to dig into the numbers yourself, starting your own narrative takes just a few minutes. Do it your way

A great starting point for your W. R. Berkley research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready for More Smart Investment Opportunities?

Why limit your potential to just one story? With Simply Wall Street’s Screener, you can pinpoint exciting stocks poised to outperform and unlock new possibilities for your portfolio.

Tap into future-defining tech by scanning these 26 AI penny stocks, which are shaping advances in artificial intelligence and automation across industries.

Catch tomorrow's breakthroughs early by targeting these 26 quantum computing stocks at the forefront of quantum computing innovation and disruption.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if W. R. Berkley might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.