- United States

- /

- Insurance

- /

- NYSE:AIZ

Assessing Assurant (AIZ) Valuation After Another Earnings Beat and Ongoing Share Price Momentum

Reviewed by Simply Wall St

Assurant (AIZ) just backed up its recent share momentum with another earnings beat, topping forecasts on both adjusted EPS and revenue, and extending a multi quarter streak of upside surprises.

See our latest analysis for Assurant.

The latest 1 day share price return of 1.6 percent and 7 day share price return of 6.3 percent continue a steady run higher from recent 52 week highs. In addition, a 3 year total shareholder return of just over 100 percent shows that this momentum has been building for some time.

If Assurant’s run has you thinking about where else momentum and fundamentals might line up, now is a good time to explore fast growing stocks with high insider ownership.

But with Assurant trading near record highs, a hefty three year return behind it, and analysts still seeing upside, is the stock quietly undervalued or is the market already pricing in its next leg of growth?

Most Popular Narrative: 6.6% Undervalued

With Assurant closing at $237.04 against a narrative fair value near $253.67, the story points to upside that still is not fully captured.

The analysts have a consensus price target of $241.0 for Assurant based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $14.2 billion, earnings will come to $1.2 billion, and it would be trading on a PE ratio of 11.9x, assuming you use a discount rate of 6.8%.

Curious how steady top line growth, rising margins and a lower future earnings multiple can still support a higher value than today? Discover the full narrative drivers.

Result: Fair Value of $253.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, a softer property and casualty cycle, or heightened regulatory scrutiny on lender placed products, could quickly challenge today’s upbeat growth and margin assumptions.

Find out about the key risks to this Assurant narrative.

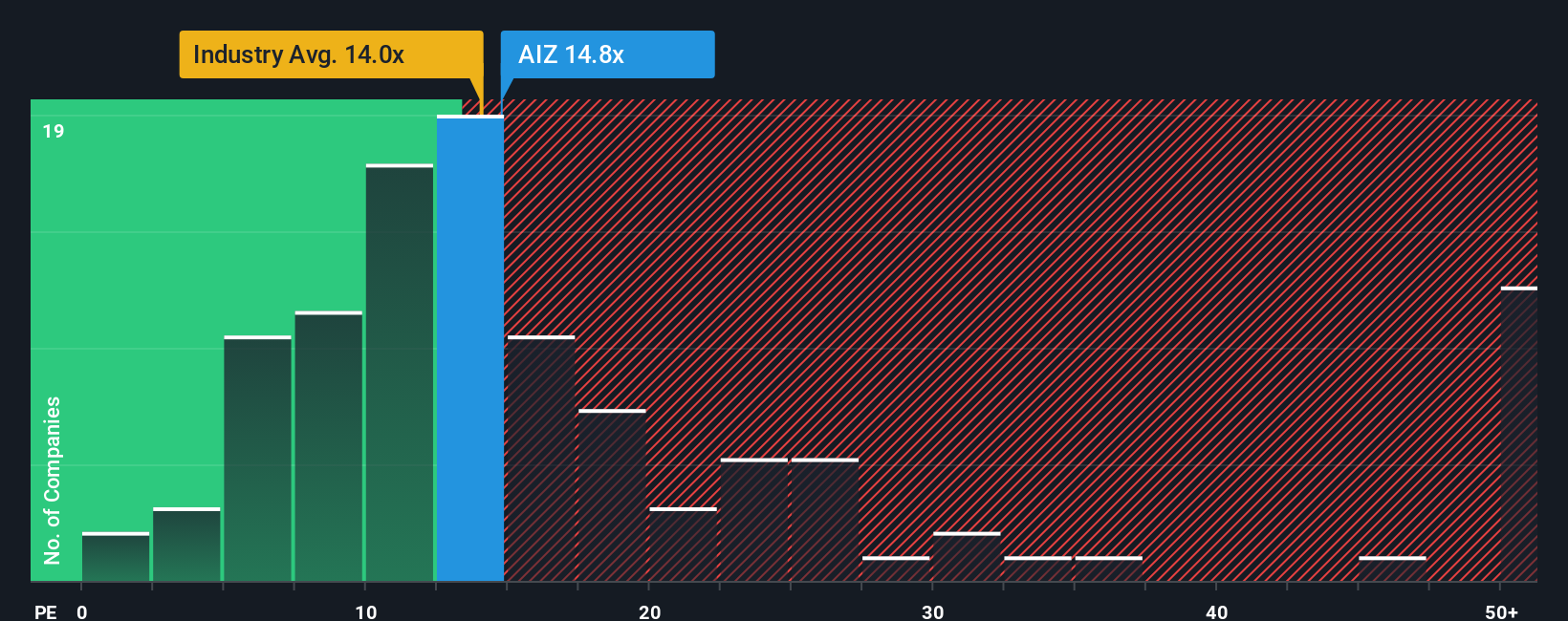

Another Angle on Valuation

On earnings multiples, Assurant looks less cheap. It trades on about 14 times earnings, slightly above both peers and the wider US insurance sector at 13.4 times. Our fair ratio sits nearer 15.2 times. Is this a modest premium or the start of multiple fatigue?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Assurant Narrative

If you see the story differently or want to analyze the numbers yourself, you can create a personalized view in just minutes using Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Assurant.

Looking for more investment ideas?

Before this rally passes you by, expand your watchlist with fresh opportunities using focused stock screeners on Simply Wall St that match your strategy and risk appetite.

- Capture potential turnarounds by targeting beaten down businesses with solid fundamentals using these 909 undervalued stocks based on cash flows before the market fully catches on.

- Explore cutting edge innovation by pinpointing companies involved in intelligent automation with these 26 AI penny stocks and consider positioning yourself for the next growth wave.

- Strengthen your income stream by focusing on companies with a history of regular dividend payments through these 13 dividend stocks with yields > 3% and assess whether current yields align with your long term goals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AIZ

Assurant

Provides protection services to connected devices, homes, and automobiles in North America, Latin America, Europe, and the Asia Pacific.

Solid track record established dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion