Advertisement

- United States

- /

- Household Products

- /

- NasdaqGS:KMB

Kimberly-Clark (NYSE:KMB) Will Pay A Larger Dividend Than Last Year At $1.26

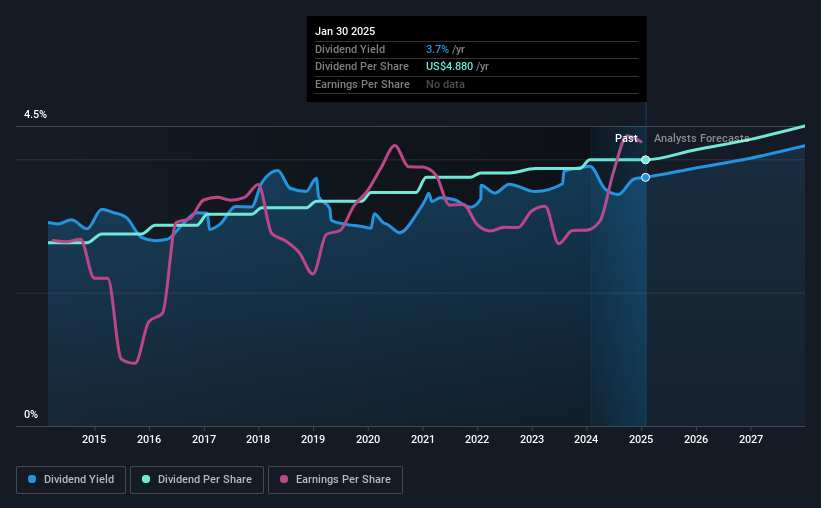

Kimberly-Clark Corporation (NYSE:KMB) will increase its dividend on the 2nd of April to $1.26, which is 3.3% higher than last year's payment from the same period of $1.22. This takes the dividend yield to 3.7%, which shareholders will be pleased with.

See our latest analysis for Kimberly-Clark

Kimberly-Clark's Payment Could Potentially Have Solid Earnings Coverage

If the payments aren't sustainable, a high yield for a few years won't matter that much. Prior to this announcement, Kimberly-Clark's dividend was comfortably covered by both cash flow and earnings. This indicates that quite a large proportion of earnings is being invested back into the business.

Over the next year, EPS is forecast to expand by 8.6%. If the dividend continues on this path, the payout ratio could be 61% by next year, which we think can be pretty sustainable going forward.

Kimberly-Clark Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. Since 2015, the annual payment back then was $3.36, compared to the most recent full-year payment of $4.88. This implies that the company grew its distributions at a yearly rate of about 3.8% over that duration. Slow and steady dividend growth might not sound that exciting, but dividends have been stable for ten years, which we think makes this a fairly attractive offer.

The Dividend's Growth Prospects Are Limited

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Earnings have grown at around 4.1% a year for the past five years, which isn't massive but still better than seeing them shrink. The company has been growing at a pretty soft 4.1% per annum, and is paying out quite a lot of its earnings to shareholders. This isn't bad in itself, but unless earnings growth pick up we wouldn't expect dividends to grow either.

We Really Like Kimberly-Clark's Dividend

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. All of these factors considered, we think this has solid potential as a dividend stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 1 warning sign for Kimberly-Clark that investors need to be conscious of moving forward. Is Kimberly-Clark not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Kimberly-Clark might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:KMB

Kimberly-Clark

Manufactures and markets personal care products in the United States.

Very undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor