Advertisement

- United States

- /

- Personal Products

- /

- NYSE:ELF

e.l.f. Beauty (ELF): Exploring Valuation After Analyst Downgrades and Mixed Earnings Signals

Simply Wall St

Reviewed by Simply Wall St

After the recent fireside chat with Goldman Sachs, e.l.f. Beauty (ELF) has come under investor scrutiny. Downgrades in earnings forecasts and uncertainties from its latest earnings report have weighed on near-term sentiment and valuation.

See our latest analysis for e.l.f. Beauty.

Despite all the buzz from the recent Goldman Sachs chat and a flurry of analyst reactions, e.l.f. Beauty’s share price has tumbled in 2024, with a 41% drop year-to-date, and its one-year total shareholder return sits at -41.98%. Still, when you zoom out, its long-term investors remain well ahead, as demonstrated by a 228% five-year total return. Current volatility marks a sharp shift from what had been strong momentum.

If recent volatility has you rethinking your next move, it could be the perfect time to broaden your search and discover fast growing stocks with high insider ownership

With e.l.f. Beauty trading well below analyst price targets and future growth on the horizon, the key question remains: is the current weakness a genuine buying opportunity, or has the market already factored in the recovery?

Most Popular Narrative: 40.8% Undervalued

The most widely followed narrative suggests that e.l.f. Beauty’s fair value sits far above its recent close of $72.11. This signals a potentially major gap between what the market is willing to pay now and what some believe it's truly worth. The narrative pairs this valuation with optimism about multi-year growth drivers and profitability levers, setting the stage for a possible turnaround.

The company is highly effective at leveraging influencer marketing, social media virality, and community-driven innovation (for example, TikTok Shop exclusives and a rapid launch cadence). This enables lower customer acquisition costs and highly efficient brand-building, supporting both top-line growth and sustainable net margin expansion.

What is really fueling this bold price target? An aggressive outlook on sales trends, margin potential, and the payoff from digital and product expansion. But is there a surprise in just how ambitious those profit forecasts get? You’ll want to see what assumptions drive this fair value calculation.

Result: Fair Value of $121.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent reliance on Chinese manufacturing and the risk of tariff hikes could quickly pressure margins, which may challenge even the most bullish growth assumptions.

Find out about the key risks to this e.l.f. Beauty narrative.

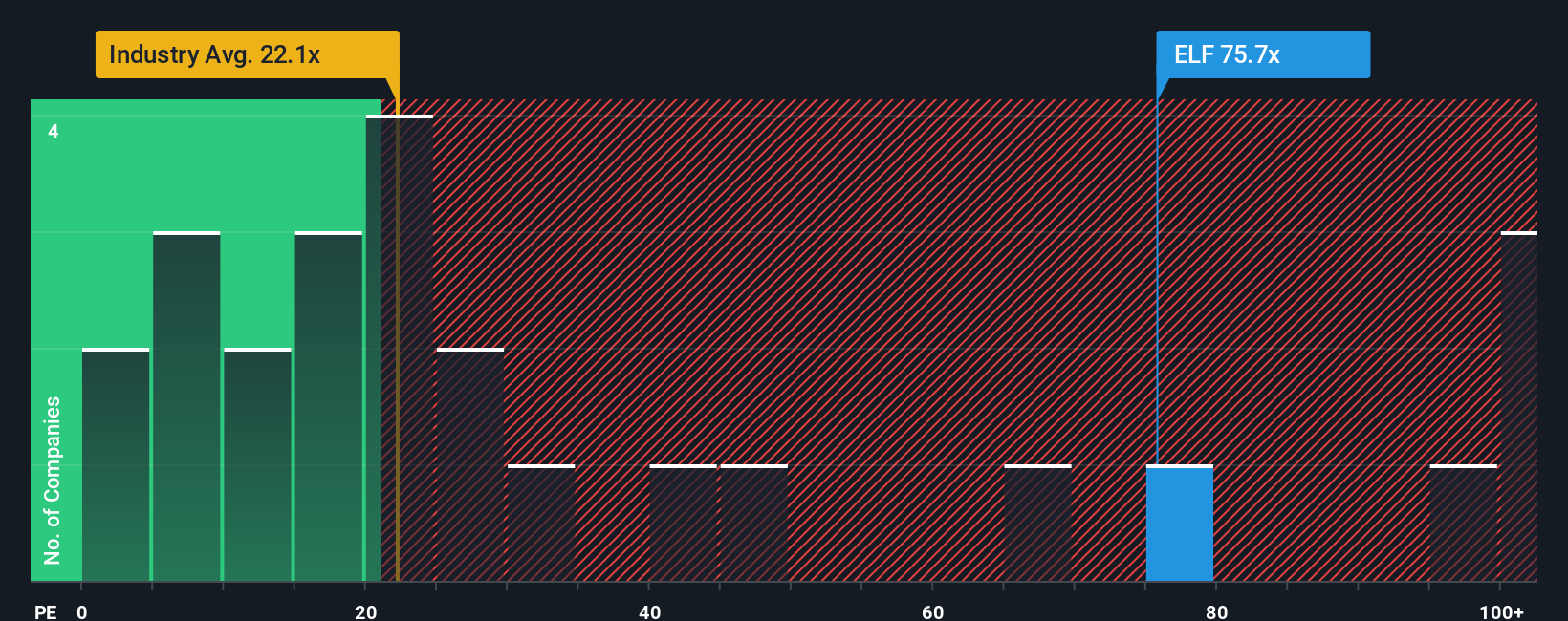

Another View: Market Multiples Raise Caution

While the fair value estimate hints at a bargain, the current market ratio for e.l.f. Beauty stands at 52.6x, far above its industry average of 22.1x and peer average of 14.4x. The fair ratio, which the market might eventually revert to, is even lower at 34.2x. This wide gap suggests there could be valuation risk if investors reassess growth expectations. Is this premium truly justified?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own e.l.f. Beauty Narrative

If you see things differently or want to dig into the numbers firsthand, you can shape your own e.l.f. Beauty story in just a few minutes: Do it your way

A great starting point for your e.l.f. Beauty research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Smart Investing Opportunities?

Don’t let your portfolio miss out. The smartest investors continually scan for powerful trends and untapped growth. Let Simply Wall Street’s screeners give you an edge:

- Accelerate your portfolio with future-shaping tech by tapping into these 26 AI penny stocks, home to companies pioneering artificial intelligence.

- Build lasting wealth with reliable payouts when you scan these 14 dividend stocks with yields > 3%, highlighting top stocks with robust dividend yields over 3%.

- Capitalize on overlooked companies trading below their intrinsic value by heading to these 925 undervalued stocks based on cash flows for hidden gems in today’s market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ELF

e.l.f. Beauty

A beauty company, provides cosmetics and skin care products worldwide.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.5% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative