Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Veru Inc. (NASDAQ:VERU) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Veru

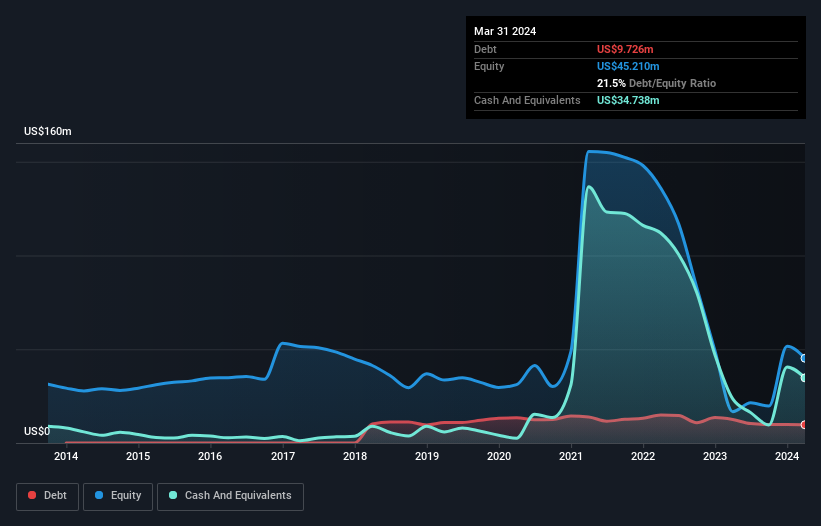

What Is Veru's Net Debt?

As you can see below, Veru had US$9.73m of debt at March 2024, down from US$12.5m a year prior. However, its balance sheet shows it holds US$34.7m in cash, so it actually has US$25.0m net cash.

How Healthy Is Veru's Balance Sheet?

According to the last reported balance sheet, Veru had liabilities of US$9.57m due within 12 months, and liabilities of US$17.0m due beyond 12 months. On the other hand, it had cash of US$34.7m and US$2.79m worth of receivables due within a year. So it can boast US$10.9m more liquid assets than total liabilities.

This surplus suggests that Veru has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Veru has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Veru's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Veru made a loss at the EBIT level, and saw its revenue drop to US$13m, which is a fall of 37%. That makes us nervous, to say the least.

So How Risky Is Veru?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Veru had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of US$40m and booked a US$39m accounting loss. With only US$25.0m on the balance sheet, it would appear that its going to need to raise capital again soon. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 6 warning signs for Veru you should be aware of, and 3 of them don't sit too well with us.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:VERU

Veru

A late clinical stage biopharmaceutical company, focuses on developing medicines for treatment of metabolic diseases, oncology, and viral-induced acute respiratory distress syndrome (ARDS).

Adequate balance sheet slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor