Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:HIMS

A Fresh Look at Hims & Hers Health’s Valuation After Policy Support and Buyback Announcement

Simply Wall St

Reviewed by Simply Wall St

Shares of Hims & Hers Health (HIMS) recently climbed after the White House signaled plans to extend Obamacare subsidies, a shift that is expected to secure enrollment and strengthen revenue streams for online healthcare providers.

See our latest analysis for Hims & Hers Health.

The impressive momentum behind Hims & Hers Health is hard to miss, with a 7.2% share price return over the past week helping to recover ground lost during last month's broader pullback. In addition to policy tailwinds, the company’s $250 million share repurchase program and expansion into diagnostic offerings like Labs have fueled bullish sentiment. Looking at the bigger picture, Hims & Hers’ 52% year-to-date share price return and over 520% total return for shareholders in the past three years reinforce that growth optimism remains strong despite periodic volatility.

If recent healthcare breakthroughs have you curious about tomorrow's winners, now is a perfect chance to discover more with our curated list: See the full list for free.

With shares rebounding and new initiatives driving headlines, the central question remains: is Hims & Hers Health trading at a discount with room to run, or is the market already pricing in the company’s next phase of growth?

Most Popular Narrative: 55% Undervalued

With the latest close at $38.40 and a widely followed fair value estimate of $86.09, the stage is set for an ambitious upside argument. According to user BlackGoat, the narrative highlights dramatic platform potential, robust growth signals, and a value proposition many see as still early in its lifecycle.

Hims is vertically integrating diagnosis, fulfilment, treatment, and retention under one platform. By avoiding insurance entirely and personalizing care at scale, the company aims for faster growth, higher margins, and better patient outcomes.

Want to know the growth blueprint behind this high valuation? The key element of this narrative is bold revenue and margin projections that rival the hottest disruptors. Curious which numbers are fueling these ambitious price targets? Only the full narrative reveals what is really driving such a significant upside.

Result: Fair Value of $86.09 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, regulatory crackdowns or unexpected changes to partnership agreements could quickly challenge the bullish narrative and put pressure on Hims & Hers Health’s growth strategy.

Find out about the key risks to this Hims & Hers Health narrative.

Another View: Multiples Show a Higher Bar

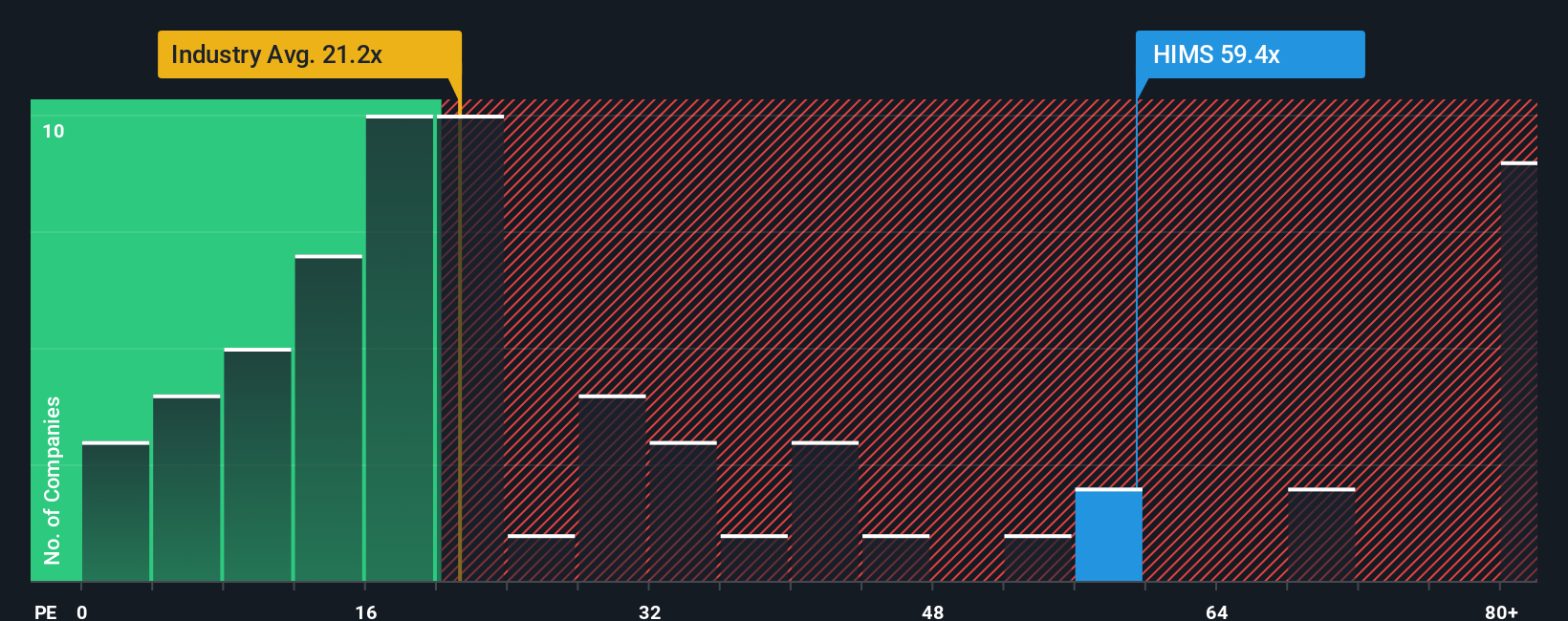

While discounted cash flow models point to a notable undervaluation, a look at the price-to-earnings ratio tells a different story. Hims & Hers Health trades at 65.3 times earnings, which is over twice the average for US healthcare peers and a significant premium to its fair ratio of 45.7. This high multiple suggests investors are banking on future performance, raising the stakes if growth slows. Is the market too optimistic, or is this the cost of leadership in a sector ripe for disruption?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Hims & Hers Health Narrative

If the above perspectives do not align with your views, or you want to analyze the numbers firsthand, it takes just moments to craft your own perspective. Do it your way

A great starting point for your Hims & Hers Health research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for More Smart Investment Angles?

Stop waiting on the sidelines and start fueling your strategy with hand-picked opportunities. See what's trending now and seize the edge before others catch on.

- Unlock fast-growing opportunities by checking out these 25 AI penny stocks which are designed to benefit from the AI revolution reshaping entire industries.

- Grab the chance for strong cash flow potential with these 926 undervalued stocks based on cash flows that are already showing signs of being mispriced by the market.

- Boost your income stream by selecting from these 15 dividend stocks with yields > 3% providing reliable yields above 3% for a more stable portfolio foundation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hims & Hers Health might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HIMS

Hims & Hers Health

Operates a telehealth platform that connects consumers to licensed healthcare professionals in the United States, the United Kingdom, and internationally.

High growth potential with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative