- United States

- /

- Healthcare Services

- /

- NYSE:CAH

The Return Trends At Cardinal Health (NYSE:CAH) Look Promising

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, we've noticed some promising trends at Cardinal Health (NYSE:CAH) so let's look a bit deeper.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Cardinal Health is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

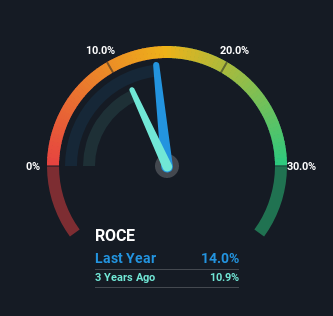

0.14 = US$1.6b ÷ (US$44b - US$33b) (Based on the trailing twelve months to December 2022).

Therefore, Cardinal Health has an ROCE of 14%. On its own, that's a standard return, however it's much better than the 9.4% generated by the Healthcare industry.

Check out our latest analysis for Cardinal Health

Above you can see how the current ROCE for Cardinal Health compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Cardinal Health here for free.

SWOT Analysis for Cardinal Health

- Debt is well covered by earnings and cashflows.

- Dividend is low compared to the top 25% of dividend payers in the Healthcare market.

- Expected to breakeven next year.

- Has sufficient cash runway for more than 3 years based on current free cash flows.

- Good value based on P/S ratio and estimated fair value.

- Total liabilities exceed total assets, which raises the risk of financial distress.

- Paying a dividend but company is unprofitable.

What Does the ROCE Trend For Cardinal Health Tell Us?

We're pretty happy with how the ROCE has been trending at Cardinal Health. The data shows that returns on capital have increased by 26% over the trailing five years. That's a very favorable trend because this means that the company is earning more per dollar of capital that's being employed. Interestingly, the business may be becoming more efficient because it's applying 43% less capital than it was five years ago. A business that's shrinking its asset base like this isn't usually typical of a soon to be multi-bagger company.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. Essentially the business now has suppliers or short-term creditors funding about 75% of its operations, which isn't ideal. Given it's pretty high ratio, we'd remind investors that having current liabilities at those levels can bring about some risks in certain businesses.

In Conclusion...

In a nutshell, we're pleased to see that Cardinal Health has been able to generate higher returns from less capital. And with a respectable 55% awarded to those who held the stock over the last five years, you could argue that these developments are starting to get the attention they deserve. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

If you'd like to know about the risks facing Cardinal Health, we've discovered 2 warning signs that you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:CAH

Cardinal Health

Operates as a healthcare services and products company in the United States, Canada, Europe, Asia, and internationally.

Undervalued with solid track record and pays a dividend.