Advertisement

- United States

- /

- Medical Equipment

- /

- NYSE:BLCO

Bausch + Lomb (BLCO): Assessing Valuation After Icahn-Linked Board Shake-Up

Simply Wall St

Reviewed by Simply Wall St

Bausch + Lomb (NYSE:BLCO) recently experienced a shakeup in its boardroom that could have long-term implications for investors. Brett M. Icahn and Gary Hu stepped down as directors after the company’s appointment and nomination agreement with Carl Icahn and his affiliates was terminated. This decision was prompted when the Icahn group’s stake in Bausch Health, the parent company, fell below a critical threshold. While the company expressed appreciation for their contributions, board turnover of this kind often sparks fresh debate about the direction of governance and future priorities at Bausch + Lomb.

It is worth noting how these changes fit into a dynamic year for BLCO. The stock has seen meaningful gains, climbing almost 33% over the past three months after lagging earlier in the year, though the one-year return is still down 8%. That type of price action suggests shifting sentiment among investors, possibly as perceptions about risk and the company’s growth story evolve. Recent board exits present another consideration for market watchers weighing strategic stability against new opportunities.

With BLCO’s recent jump, some may wonder whether investors are seeing a genuine value opportunity after last year’s underperformance, or if the market is already factoring in future growth and a reset in governance.

Price-to-Sales of 1.1x: Is it justified?

Bausch + Lomb appears undervalued based on its price-to-sales (P/S) ratio compared to both industry peers and broader sector averages.

The P/S ratio measures a company’s stock price relative to its revenues. This offers insight into how the market values each dollar of sales. This metric is especially relevant for healthcare companies like Bausch + Lomb, where profitability may fluctuate, but revenue growth remains a key indicator of business traction.

At 1.1x, BLCO trades well below the US Medical Equipment industry average of 2.8x, the peer average of 2.4x, and also under the estimated fair ratio of 2.2x. This may indicate that the market is discounting the company’s future growth potential or its current unprofitability.

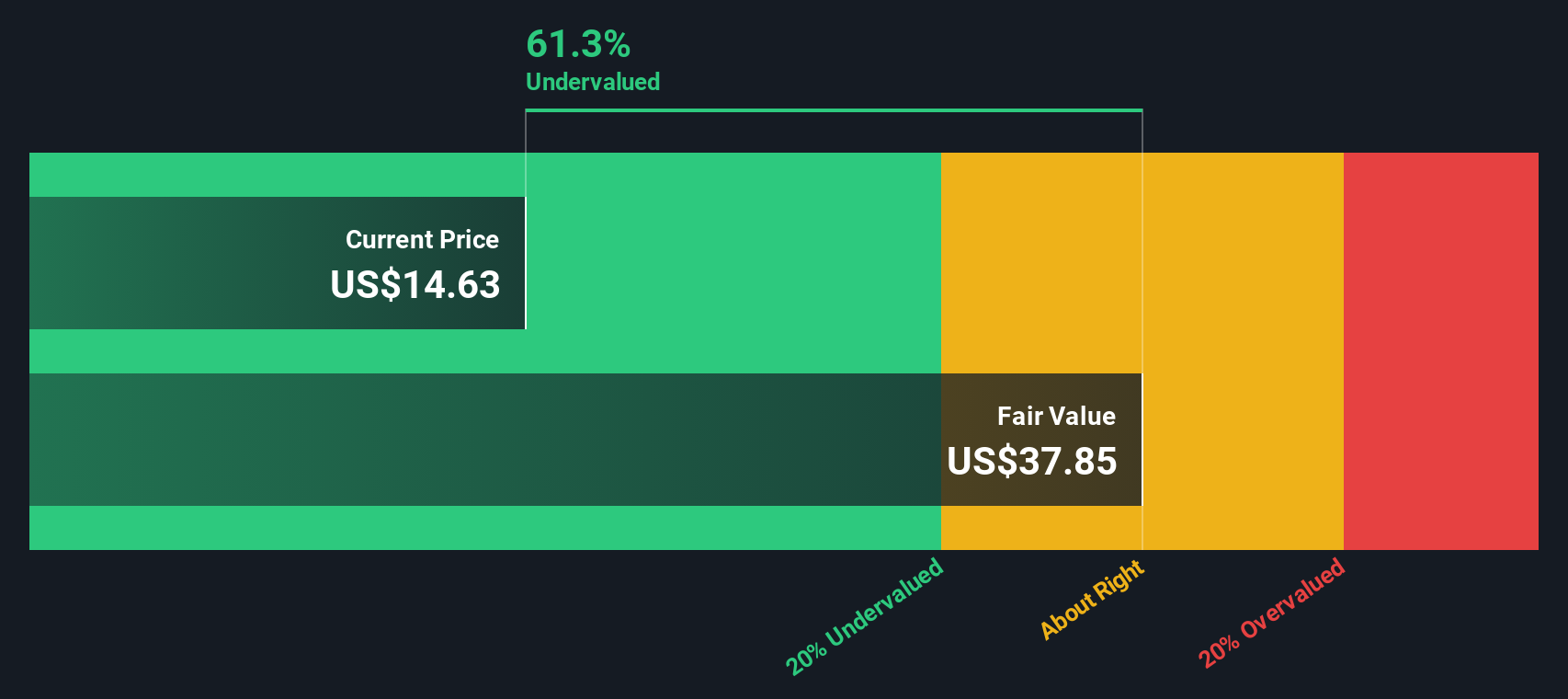

Result: Fair Value of $37.83 (UNDERVALUED)

See our latest analysis for Bausch + Lomb.However, slowing revenue growth and continued net losses could limit further upside if market sentiment shifts or if operational improvements fall short of expectations.

Find out about the key risks to this Bausch + Lomb narrative.Another View: DCF Model Insight

The SWS DCF model offers a different perspective and also points toward undervaluation for Bausch + Lomb. This approach calculates value based on projected future cash flows rather than focusing only on current sales. Could both models be missing something?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Bausch + Lomb Narrative

If you see things differently or want to dive deeper into the numbers, you can build your own narrative in just a few minutes. do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Bausch + Lomb.

Looking for more investment ideas?

Great investors always keep their watchlists fresh. If you want an edge, now is the moment to act. The market continues to reward those who seek out new opportunities. Let Simply Wall Street’s tailored screeners help you uncover your next potential winner, so you don’t get left behind.

- Target reliable income streams by reviewing dividend stocks with yields > 3% and spot companies offering robust yields with sustainable payouts.

- Take advantage of emerging tech trends as you scan AI penny stocks and uncover innovative firms pushing boundaries in artificial intelligence.

- Lessen your risk and boost long-term potential by finding undervalued stocks based on cash flows that could be trading for less than their true worth right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bausch + Lomb might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BLCO

Bausch + Lomb

Operates as an eye health company in the United States, Puerto Rico, China, France, Japan, Germany, the United Kingdom, Canada, Russia, Spain, Italy, Mexico, Poland, and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|50.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|8.5% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|20.3% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|54.2% overvalued

RO

Community Contributor