Advertisement

- United States

- /

- Healthtech

- /

- NasdaqCM:STRM

Streamline Health Solutions, Inc.'s (NASDAQ:STRM) Share Price Boosted 46% But Its Business Prospects Need A Lift Too

Those holding Streamline Health Solutions, Inc. (NASDAQ:STRM) shares would be relieved that the share price has rebounded 46% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. But the last month did very little to improve the 68% share price decline over the last year.

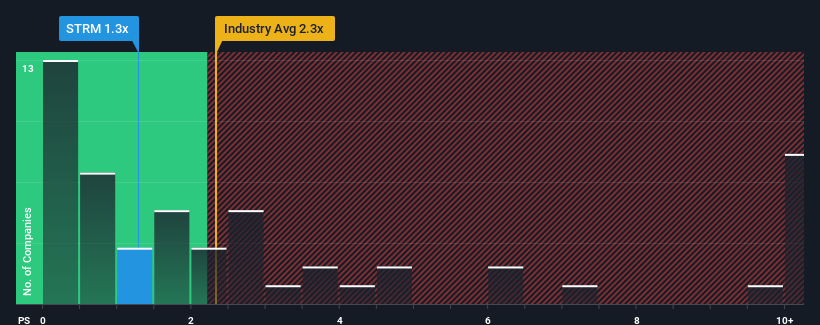

In spite of the firm bounce in price, Streamline Health Solutions' price-to-sales (or "P/S") ratio of 1.3x might still make it look like a buy right now compared to the Healthcare Services industry in the United States, where around half of the companies have P/S ratios above 2.3x and even P/S above 5x are quite common. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Streamline Health Solutions

What Does Streamline Health Solutions' Recent Performance Look Like?

Streamline Health Solutions hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. The P/S ratio is probably low because investors think this poor revenue performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Streamline Health Solutions.What Are Revenue Growth Metrics Telling Us About The Low P/S?

Streamline Health Solutions' P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 11%. However, a few very strong years before that means that it was still able to grow revenue by an impressive 89% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Turning to the outlook, the next three years should generate growth of 3.2% each year as estimated by the sole analyst watching the company. With the industry predicted to deliver 12% growth per year, the company is positioned for a weaker revenue result.

In light of this, it's understandable that Streamline Health Solutions' P/S sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

Streamline Health Solutions' stock price has surged recently, but its but its P/S still remains modest. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Streamline Health Solutions' analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. The company will need a change of fortune to justify the P/S rising higher in the future.

Having said that, be aware Streamline Health Solutions is showing 5 warning signs in our investment analysis, and 2 of those don't sit too well with us.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:STRM

Streamline Health Solutions

Provides health information technology solutions and associated services for hospitals and health systems in North America.

Slight risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor