- United States

- /

- Healthcare Services

- /

- NasdaqGS:PNTG

Is It Too Late To Consider Pennant Group After Its Strong Multi Year Share Price Rally?

Reviewed by Bailey Pemberton

- If you are wondering whether Pennant Group is still attractively priced today, or if most of the potential upside has already been captured, you are in the right place to unpack what the market might be missing.

- The stock has eased slightly over the last week, down about 1.3%. It is still up around 10.0% over the past month, 10.9% year to date, and 194.9% over three years, although it remains down 51.9% over five years.

- Those swings sit against a backdrop of steady operational progress and ongoing consolidation in post acute care and senior living. Smaller regional operators like Pennant may benefit from aging demographics and shifting reimbursement dynamics. At the same time, regulatory scrutiny and staffing pressures remain front of mind for investors, which helps explain why the market has not re rated the stock in a straight line.

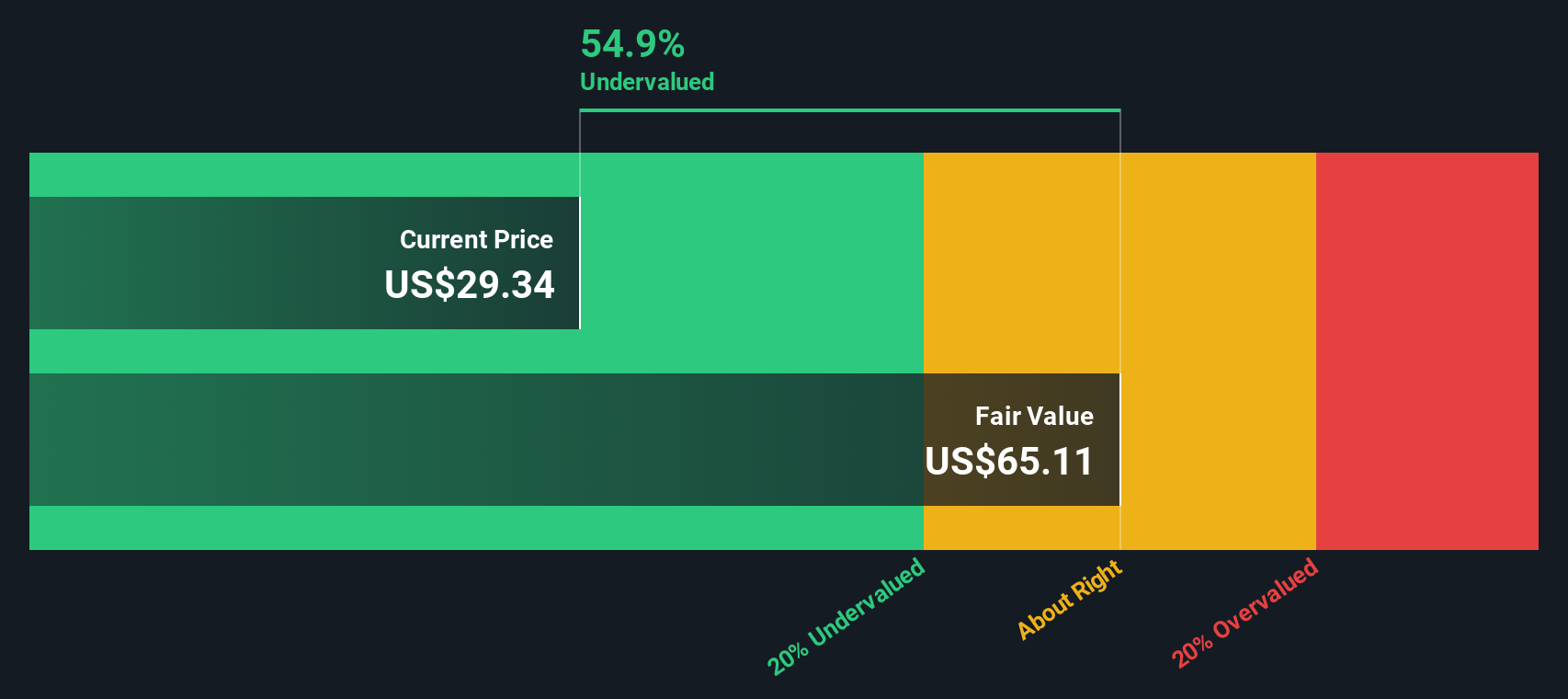

- Right now Pennant scores a 4/6 valuation check for being undervalued, which suggests there may still be some mispricing to explore. Next we will walk through the usual valuation tools, and later on we will look at a way to tie those numbers back to the company’s long term narrative.

Approach 1: Pennant Group Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and discounting those cash flows back to today in dollar terms. For Pennant Group, the latest twelve month Free Cash Flow is about $27.3 million. Analysts and model assumptions see this rising steadily, with projected Free Cash Flow of roughly $117.4 million in 10 years, based on a two stage Free Cash Flow to Equity framework that blends analyst inputs through 2027 with longer term growth assumptions beyond that.

When these projected cash flows are discounted back to today, Simply Wall St’s DCF model arrives at an intrinsic value of about $65.11 per share. Compared with the current share price, this implies the stock is trading at a 54.9% discount to its estimated fair value, suggesting meaningful upside if the cash flow trajectory plays out as expected.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Pennant Group is undervalued by 54.9%. Track this in your watchlist or portfolio, or discover 913 more undervalued stocks based on cash flows.

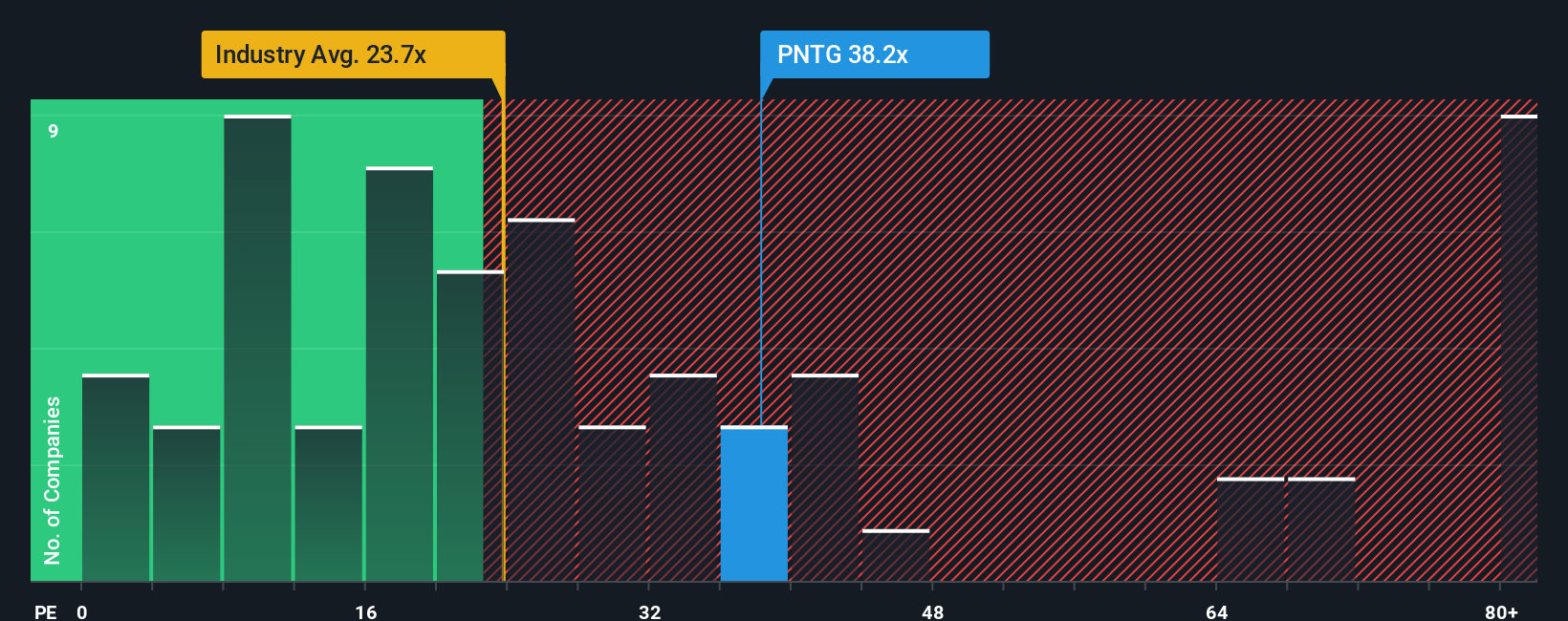

Approach 2: Pennant Group Price vs Earnings

For a profitable company like Pennant Group, the price to earnings ratio is a useful yardstick because it links what investors pay today with the earnings the business is already generating. In general, faster growing and less risky companies tend to command higher PE multiples, while slower growth or higher uncertainty usually justify a lower, more conservative PE.

Pennant currently trades on a PE of about 38.0x, which is higher than the broader Healthcare industry average of roughly 23.7x and also below the very rich peer group average of about 100.9x. To refine that comparison, Simply Wall St uses a proprietary Fair Ratio. This is an estimate of what Pennant’s PE should be once factors like its earnings growth outlook, margins, industry, market cap and risk profile are all taken into account. This makes it more tailored than a simple peer or sector comparison, which can be skewed by outliers or companies at very different stages of maturity.

For Pennant, the Fair Ratio is around 27.1x. This means the current 38.0x multiple sits above what would be considered justified by its fundamentals, pointing to some overvaluation on a PE basis.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1464 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Pennant Group Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply your story about a company expressed through the numbers you expect it to deliver in the future.

On Simply Wall St’s Community page, Narratives let you connect Pennant Group’s business story to a concrete financial forecast by setting out your expectations for future revenue, earnings, margins and an assumed fair value, then comparing that fair value to today’s share price to decide if you want to buy, hold or sell.

Because these Narratives are dynamic, they update as new information like earnings, regulatory news or acquisitions comes in. This means your investment view can evolve instead of staying locked in a static model.

For Pennant Group, for example, one investor might build a bullish Narrative around demographic tailwinds and margin expansion that supports a fair value near the high analyst target of 40.0 dollars. A more cautious investor could focus on regulatory and labor risks and land closer to the low target of 28.0 dollars, showing how different stories lead to different, but clearly framed, valuations.

Do you think there's more to the story for Pennant Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PNTG

Good value with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion