- United States

- /

- Medical Equipment

- /

- NasdaqGS:MASI

Masimo (MASI): Reassessing Valuation After a Steady Slide in Share Price

Reviewed by Simply Wall St

Masimo (MASI) has been drifting lower recently, and that slide is catching investors attention as they reassess what the current price implies about the company future earnings power and competitive position.

See our latest analysis for Masimo.

The latest dip comes on top of a much steeper slide, with the share price down around 20 percent year to date and the one year total shareholder return similarly weak. This signals that momentum has clearly been fading as investors reassess growth and risk.

If Masimo recent pullback has you rethinking your sector exposure, this could be a good moment to explore other healthcare stocks that might offer a different balance of growth and resilience.

With the share price lagging and analysts still seeing upside to their targets, the key question now is whether Masimo is quietly undervalued or if the market is already discounting any meaningful recovery in growth.

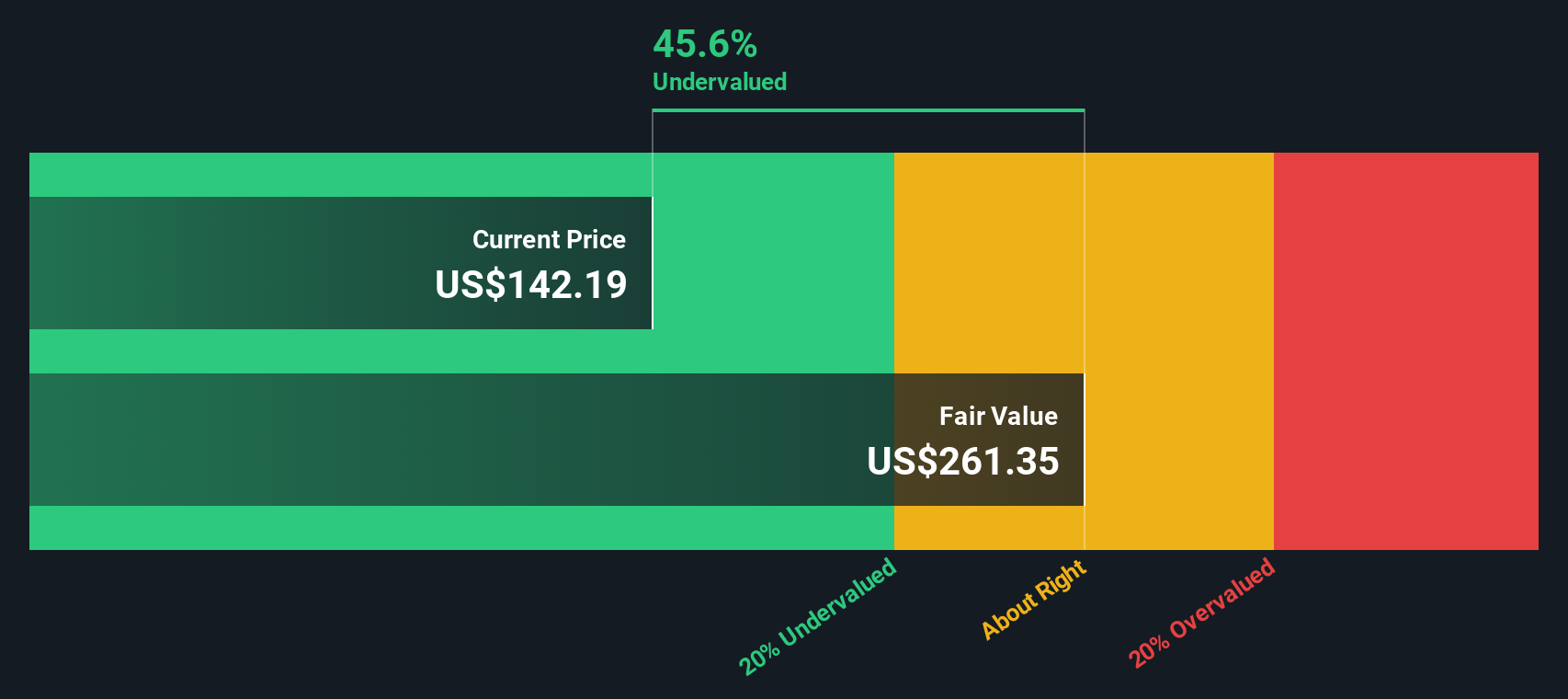

Most Popular Narrative Narrative: 26.8% Undervalued

Compared to Masimo last close at $134.04, the most widely followed narrative pegs fair value much higher, implying sizable upside if its assumptions play out.

Ongoing innovation including next-gen monitors featuring advanced AI algorithms and redeployment of novel sensor technologies positions Masimo to command premium pricing and capture greater value as hospitals prioritize technologically advanced, multiparameter solutions, supporting both revenue expansion and improved gross margins.

Curious how falling headline revenues can still line up with a higher valuation. The story hinges on a sharp margin reset and a rich future earnings multiple. Want to see how those moving parts combine into that fair value call.

Result: Fair Value of $183.13 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upbeat narrative could unravel if tariffs escalate or hospital capital budgets stay tight, delaying equipment upgrades and pressuring Masimo revenue trajectory.

Find out about the key risks to this Masimo narrative.

Another View on Value

While the popular narrative sees Masimo as 26.8 percent undervalued, our DCF model tells a very different story. On those cash flow assumptions, fair value sits nearer $98.04, meaning today price looks stretched rather than cheap. Which set of expectations do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Masimo for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 914 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Masimo Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Masimo.

Looking for more investment ideas?

Before you move on, put Simply Wall Street to work for you and lock in a watchlist of fresh opportunities that most investors are still overlooking.

- Capitalize on overlooked value by scanning these 914 undervalued stocks based on cash flows that strong cash flows suggest the market is mispricing right now.

- Ride powerful structural trends by targeting these 29 healthcare AI stocks bringing data driven breakthroughs to hospitals, diagnostics, and treatment pathways.

- Position yourself at the edge of financial innovation with these 79 cryptocurrency and blockchain stocks shaping the future of payments, security, and decentralized infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MASI

Masimo

Develops, manufactures, and markets various patient monitoring technologies, and automation and connectivity solutions worldwide.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Q3 Outlook modestly optimistic

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion