Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:MASI

Masimo (MASI) Posts Higher Sales but Swings to Loss After Buybacks Is the Growth Story at Risk?

Simply Wall St

Reviewed by Sasha Jovanovic

- Masimo Corporation recently reported third-quarter 2025 results, highlighting year-over-year sales growth to US$371.5 million but posting a net loss of US$100.4 million compared to net income in the prior-year period.

- The company also completed a major share repurchase tranche, buying back over 1.26 million shares for US$184.2 million as part of its ongoing buyback program.

- To assess how these developments may impact Masimo’s investment outlook, we'll explore the effect of higher sales yet a swing to net loss on its growth narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Masimo Investment Narrative Recap

To be a Masimo shareholder today, you need confidence in its ability to translate product innovation and commercial expansion into sustainable profitability despite a challenging market environment. The recent third-quarter update, while showing higher sales, also revealed a swing to a net loss, which raises new questions about margin recovery and the durability of earnings, but does not materially alter the short-term focus on cost containment and successful hospital contract wins.

Among recent announcements, Masimo’s completion of a major share buyback, repurchasing over 1.26 million shares for US$184.2 million, stands out, reflecting ongoing efforts to return capital to shareholders. This is particularly relevant for investors tracking the company’s ability to manage cash flows and bolster shareholder value while navigating the pressures of profitability and execution in growth segments.

Yet, in contrast to these efforts to support shareholder returns, investors should be aware that continued losses and pressure on gross margins may...

Read the full narrative on Masimo (it's free!)

Masimo's narrative projects $1.8 billion revenue and $293.5 million earnings by 2028. This requires a 5.1% annual revenue decline and a $563.2 million increase in earnings from the current level of $-269.7 million.

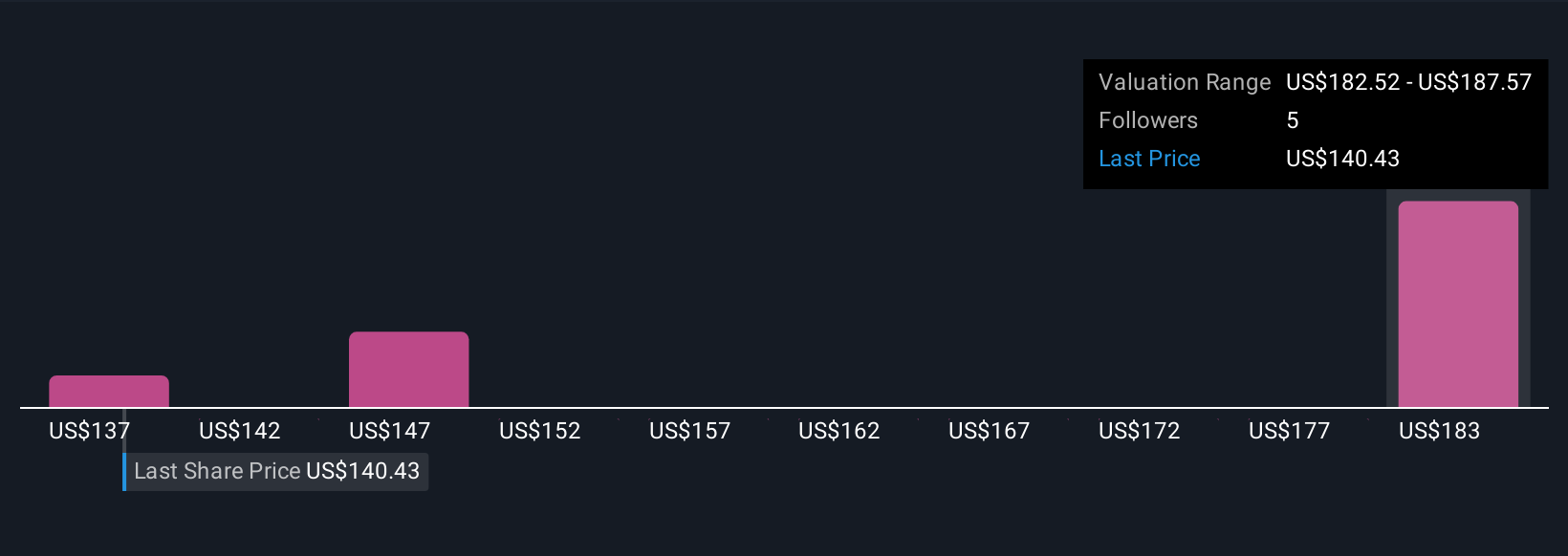

Uncover how Masimo's forecasts yield a $187.57 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Three distinct fair value estimates from the Simply Wall St Community range widely, from US$137.02 to US$263.07 per share. While community views highlight substantial differences in outlook, the current risk of margin compression due to global tariffs could weigh on the company’s future performance, underscoring the need to compare several points of view before forming an opinion.

Explore 3 other fair value estimates on Masimo - why the stock might be worth 9% less than the current price!

Build Your Own Masimo Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Masimo research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Masimo research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Masimo's overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 36 companies in the world exploring or producing it. Find the list for free.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MASI

Masimo

Develops, manufactures, and markets various patient monitoring technologies, and automation and connectivity solutions worldwide.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor