Advertisement

- United States

- /

- Healthcare Services

- /

- NasdaqGS:HQY

Assessing HealthEquity After New Digital Health Rollouts and a 9.2% Share Price Climb

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if HealthEquity is a hidden bargain or priced to perfection? You are not alone. Many investors are taking a closer look at its current value.

- The stock has moved 1.4% over the last week and climbed 9.2% during the past month. This suggests renewed interest and possible shifts in how the market perceives its prospects and risks.

- In recent weeks, HealthEquity made headlines with strategic partnerships and new digital health product rollouts that have captured investor attention. These developments are helping to shape momentum in the stock and provide essential context for understanding the recent upward moves.

- On our current valuation checks, HealthEquity scores a 2 out of 6. This means it appears undervalued on two key fronts. Next, we will break down how this score is calculated and cover a range of valuation approaches. Stick around to the end to discover a perspective beyond the numbers.

HealthEquity scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: HealthEquity Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a valuation approach that projects a company's expected future cash flows and discounts them back to today using an appropriate rate. This helps estimate the present value of the business based on its expected ability to generate cash in years to come.

For HealthEquity, the current Free Cash Flow stands at approximately $135.6 million. Analyst projections suggest substantial growth over the coming years, with cash flows expected to rise to $490.2 million by 2028. Looking further, extrapolations estimate annual Free Cash Flow exceeding $742 million by 2035. These forecasts utilize a two-stage growth framework, taking into account both analyst outlooks and systematically modeled estimates for later years.

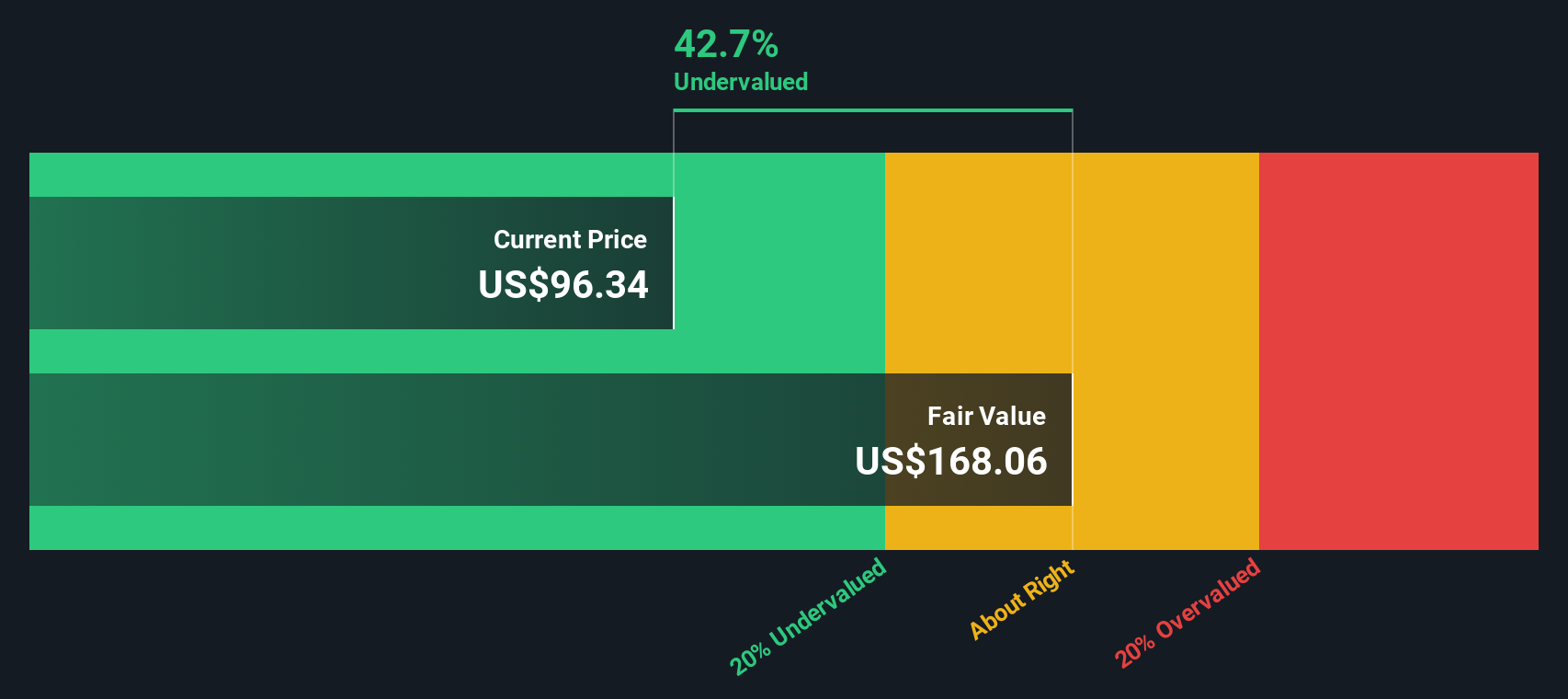

Based on these projections, the DCF model yields an intrinsic value of $168.36 per share. Relative to the current market price, this calculation suggests HealthEquity is trading at around a 37.6% discount and may be undervalued by the market.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests HealthEquity is undervalued by 37.6%. Track this in your watchlist or portfolio, or discover 926 more undervalued stocks based on cash flows.

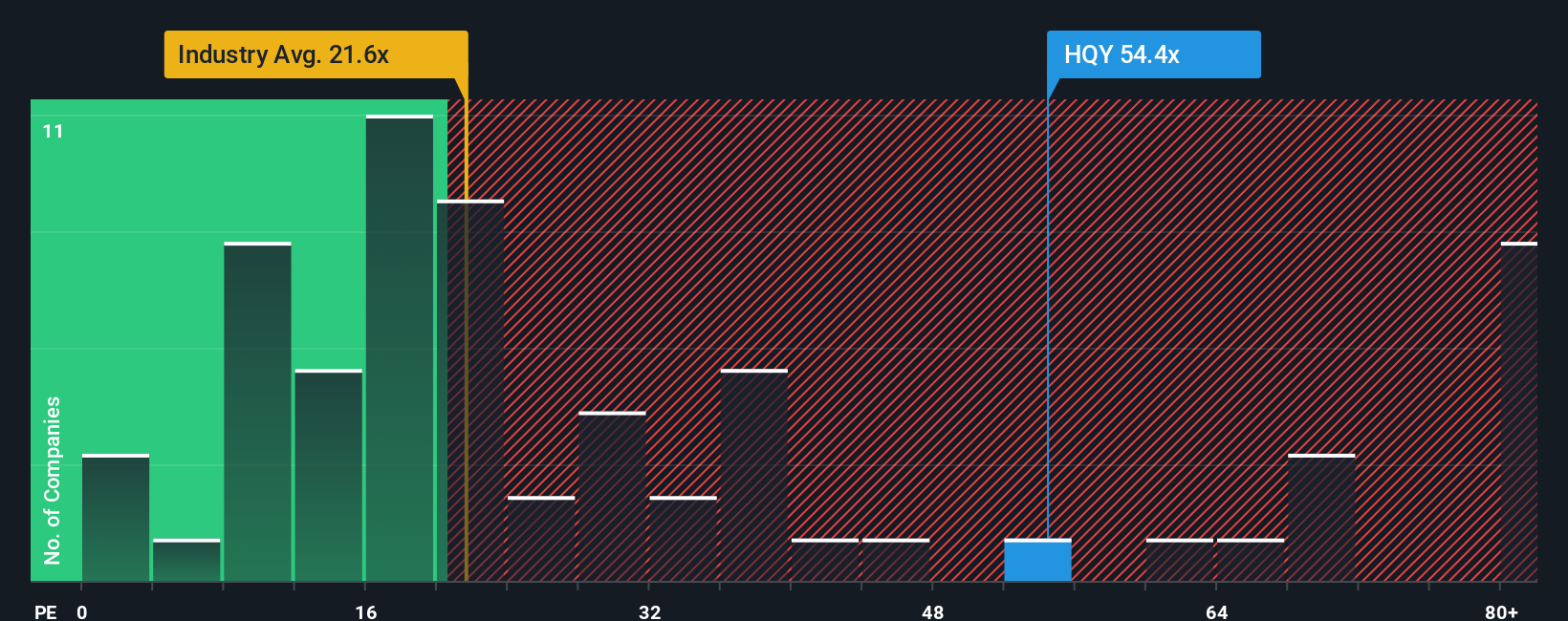

Approach 2: HealthEquity Price vs Earnings (PE Ratio)

For profitable companies, the Price-to-Earnings (PE) ratio is one of the most widely used valuation tools. It measures how much investors are willing to pay today for a dollar of the company’s current earnings. A higher PE typically reflects higher growth expectations or lower perceived risk, while a lower PE may signal caution or undervaluation by the market.

HealthEquity’s current PE ratio stands at 62x. To put this in perspective, the broader Healthcare industry averages 22.8x, and similar peer companies trade at about 21.5x. Clearly, HealthEquity is valued at a significant premium compared to both its industry and peer group, likely reflecting strong growth expectations from investors.

However, Simply Wall St’s proprietary Fair Ratio for HealthEquity is 31.7x. The Fair Ratio is a more refined benchmark. It factors in specifics like HealthEquity’s expected earnings growth, its profit margins, its unique market position, the risk profile, and its market cap, alongside industry context. This approach is more reliable than peer or industry averages, since it adjusts for factors unique to HealthEquity that could justify a higher or lower multiple.

Comparing the Fair Ratio (31.7x) to the company’s current PE (62x) suggests the stock is trading well above where it should be based on these fundamentals, implying it is likely overvalued at current levels.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1433 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your HealthEquity Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply your investment story, the reasoning and assumptions behind your outlook for a company, including your fair value estimate and projections for growth in revenue, profits, and margins.

With Narratives, you connect what is unique about a company, such as HealthEquity’s regulatory tailwinds or digital transformation efforts, to a specific financial forecast and a resulting fair value, all in one clear, personalized view. Narratives are accessible to everyone through the Community page on Simply Wall St, a tool powered by millions of real investor insights.

Narratives empower you to decide whether to buy or sell by comparing your estimated fair value to the current share price, and they update dynamically when fresh news, earnings, or regulatory changes happen so your perspective can evolve with the market.

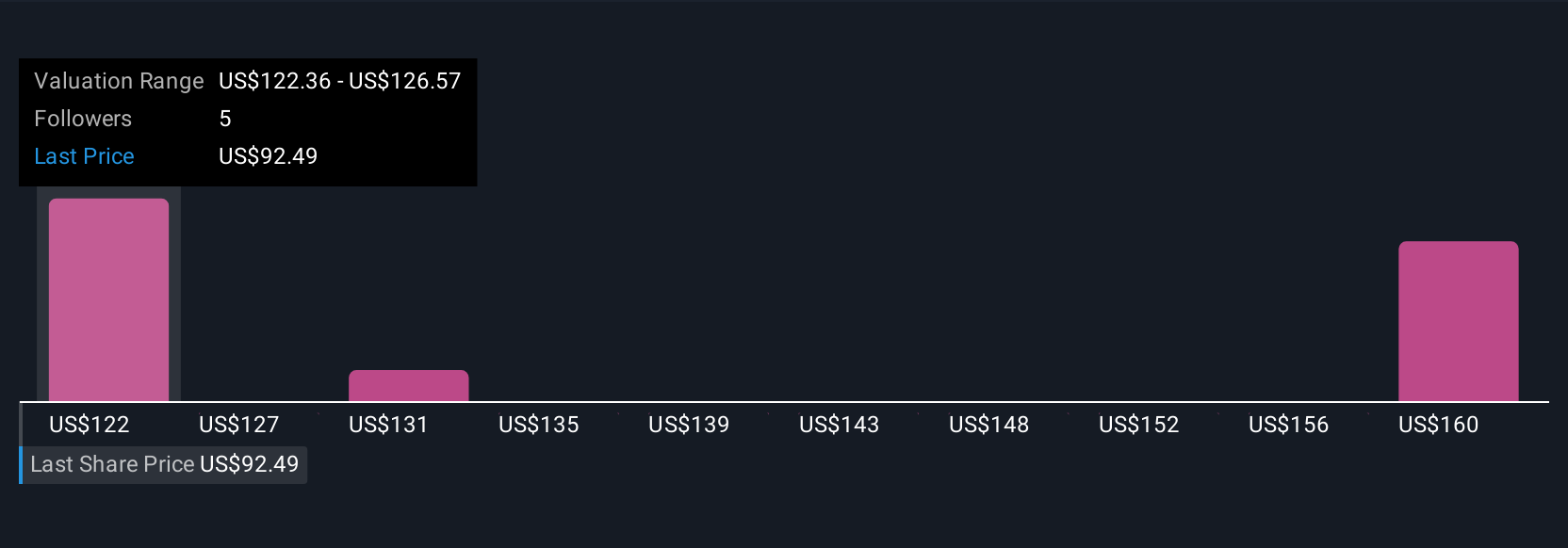

For example, some investors see HealthEquity’s major market expansion justifying price targets as high as $134.00, while others highlight risks and assign a lower fair value around $108.00. This serves as a reminder that your narrative reflects your unique beliefs, not just the numbers.

Do you think there's more to the story for HealthEquity? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HealthEquity might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HQY

HealthEquity

Provides technology-enabled services platforms to consumers and employers in the United States.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative