Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:EMBC

Embecta Corp. Just Recorded A 22% EPS Beat: Here's What Analysts Are Forecasting Next

As you might know, Embecta Corp. (NASDAQ:EMBC) just kicked off its latest quarterly results with some very strong numbers. The company beat both earnings and revenue forecasts, with revenue of US$276m, some 4.9% above estimates, and statutory earnings per share (EPS) coming in at US$0.61, 22% ahead of expectations. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

View our latest analysis for Embecta

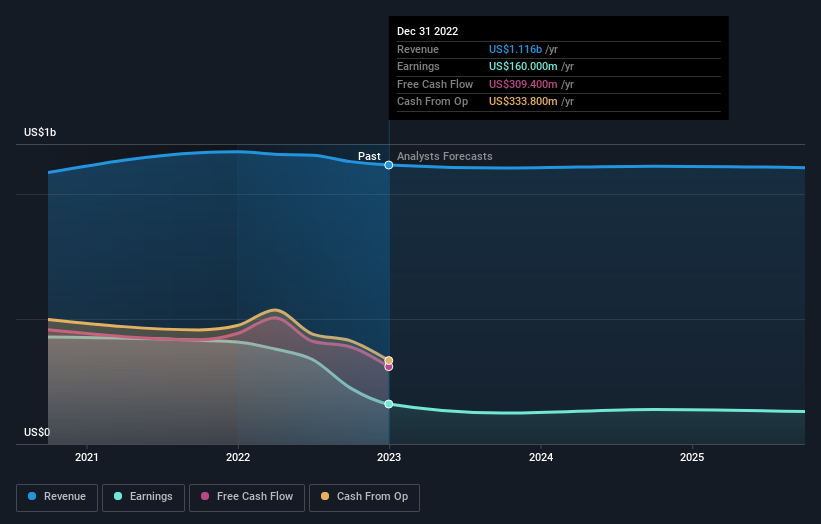

Following last week's earnings report, Embecta's three analysts are forecasting 2023 revenues to be US$1.10b, approximately in line with the last 12 months. Statutory earnings per share are expected to crater 23% to US$2.14 in the same period. In the lead-up to this report, the analysts had been modelling revenues of US$1.06b and earnings per share (EPS) of US$1.78 in 2023. So it seems there's been a definite increase in optimism about Embecta's future following the latest results, with a sizeable expansion in the earnings per share forecasts in particular.

Despite these upgrades, the consensus price target fell 5.4% to US$26.50, perhaps signalling that the uplift in performance is not expected to last. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic Embecta analyst has a price target of US$28.00 per share, while the most pessimistic values it at US$25.00. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or thatthe analysts have a strong view on its prospects.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would also point out that the forecast 1.4% annualised revenue decline to the end of 2023 is better than the historical trend, which saw revenues shrink 4.6% annually over the past year By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 7.6% per year. So it's pretty clear that, while it does have declining revenues, the analysts also expect Embecta to suffer worse than the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Embecta following these results. Fortunately, they also upgraded their revenue estimates, although our data indicates sales are expected to perform worse than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Embecta's future valuation.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Embecta going out to 2025, and you can see them free on our platform here.

Before you take the next step you should know about the 6 warning signs for Embecta (2 don't sit too well with us!) that we have uncovered.

Valuation is complex, but we're here to simplify it.

Discover if Embecta might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:EMBC

Embecta

A medical device company, focuses on the provision of various solutions to enhance the health and wellbeing of people living with diabetes in the United States and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor