Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:COO

Should Browning West's Push for Vision Care Focus Prompt Action From Cooper Companies (COO) Investors?

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 19, 2025, Browning West LP, a major shareholder of Cooper Companies, publicly urged the board to consider significant governance changes, including a shift to a pure-play vision care company, the appointment of new directors, and a reassessment of the company’s dual business structure amid ongoing underperformance.

- This shareholder activism highlights growing concerns about management oversight, strategic direction, and capital allocation at Cooper Companies, with calls for stronger board expertise in vision care and medical devices.

- We’ll now examine how Browning West’s push for a streamlined vision care focus may influence Cooper Companies’ investment narrative and outlook.

Find companies with promising cash flow potential yet trading below their fair value.

Cooper Companies Investment Narrative Recap

To be a Cooper Companies shareholder, you need confidence in the long-term growth potential of the global vision care market and the ability of CooperVision to deliver premium product innovation and margin expansion. The push from Browning West for a pure-play model puts additional pressure on Cooper’s board to address structural inefficiencies, but does not materially change the near-term catalyst, which remains the smooth execution and market take-up of MyDAY, nor the key risk of pricing competition and uncertain contact lens demand.

One announcement particularly relevant to shareholder activism is the company's increased equity buyback authorization to US$2,000,000,000. While this move is designed to return capital to shareholders and support the stock, how it aligns with Browning West’s call for improved capital allocation remains a point of interest for investors watching for signs of disciplined execution amid activist pressure.

But with intensifying price competition in the Asia Pacific region, investors should also be aware that ...

Read the full narrative on Cooper Companies (it's free!)

Cooper Companies’ outlook anticipates $4.9 billion in revenue and $786.2 million in earnings by 2028. This implies a 6.4% annual revenue growth rate and a $378.4 million increase in earnings from the current $407.8 million.

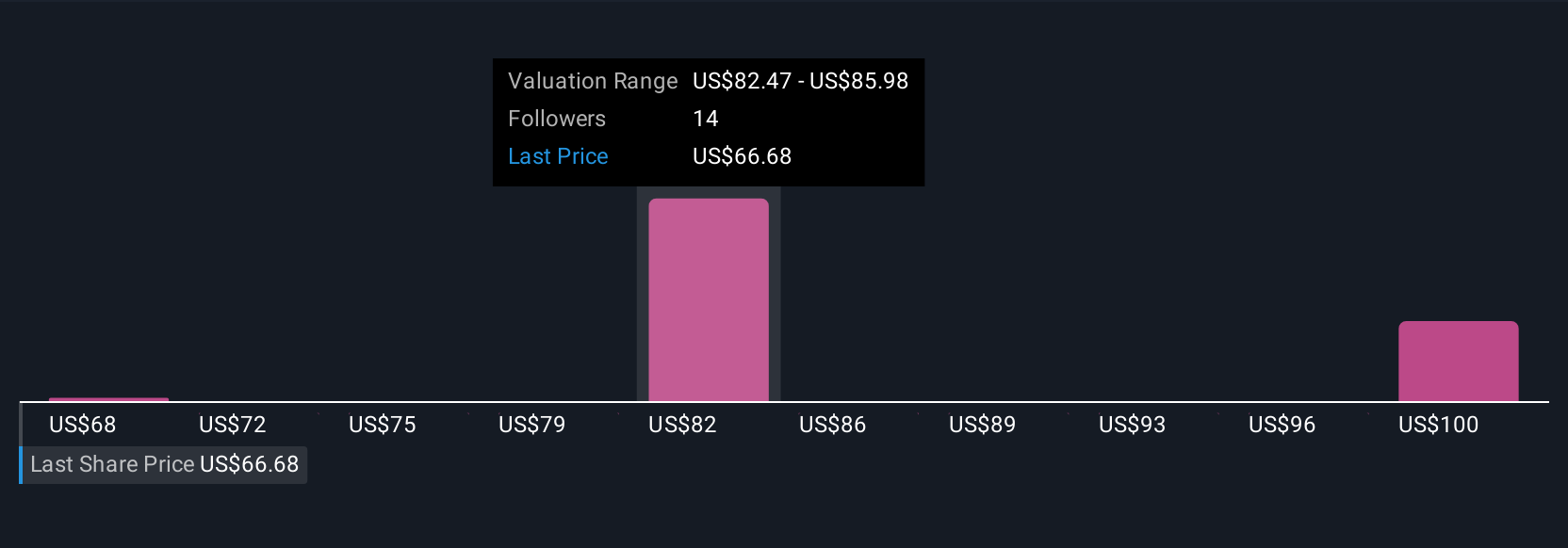

Uncover how Cooper Companies' forecasts yield a $83.00 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Three community members on Simply Wall St valued Cooper Companies between US$68.44 and US$99.11 per share. While these analyses reflect a wide spectrum of expectations, consider how ongoing board and business structure changes could affect future market performance and invite you to think critically about alternative views.

Explore 3 other fair value estimates on Cooper Companies - why the stock might be worth as much as 31% more than the current price!

Build Your Own Cooper Companies Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cooper Companies research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Cooper Companies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cooper Companies' overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:COO

Cooper Companies

Develops, manufactures, and markets contact lens wearers.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor