Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGM:ATRC

AtriCure (NASDAQ:ATRC) Has Debt But No Earnings; Should You Worry?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that AtriCure, Inc. (NASDAQ:ATRC) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

What Is AtriCure's Debt?

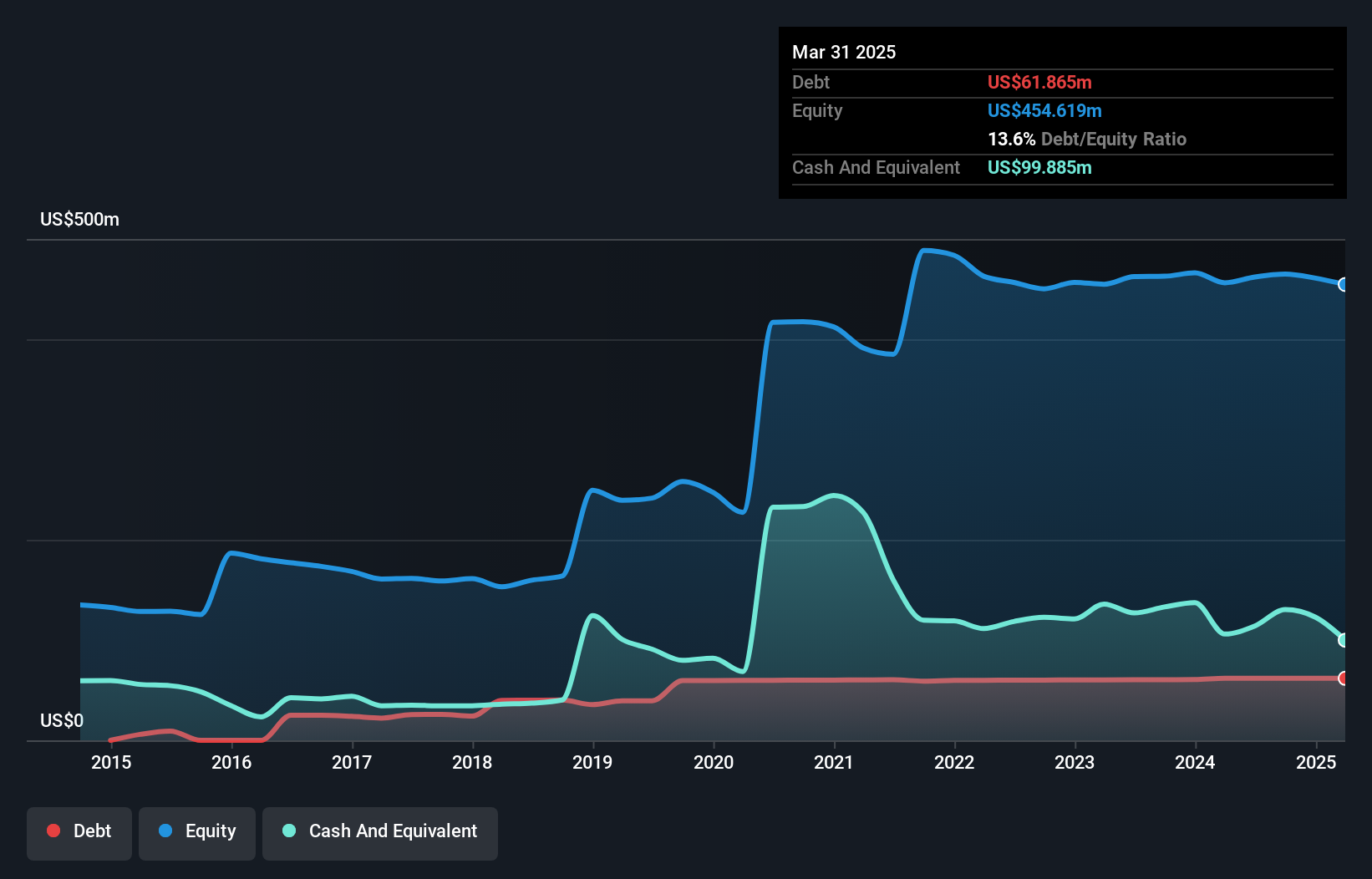

The chart below, which you can click on for greater detail, shows that AtriCure had US$61.9m in debt in March 2025; about the same as the year before. But on the other hand it also has US$99.9m in cash, leading to a US$38.0m net cash position.

How Healthy Is AtriCure's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that AtriCure had liabilities of US$61.2m due within 12 months and liabilities of US$75.8m due beyond that. Offsetting this, it had US$99.9m in cash and US$63.3m in receivables that were due within 12 months. So it can boast US$26.2m more liquid assets than total liabilities.

Having regard to AtriCure's size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the US$1.57b company is short on cash, but still worth keeping an eye on the balance sheet. Succinctly put, AtriCure boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine AtriCure's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Check out our latest analysis for AtriCure

In the last year AtriCure wasn't profitable at an EBIT level, but managed to grow its revenue by 16%, to US$480m. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is AtriCure?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that AtriCure had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through US$672k of cash and made a loss of US$38m. While this does make the company a bit risky, it's important to remember it has net cash of US$38.0m. That means it could keep spending at its current rate for more than two years. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting AtriCure insider transactions.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:ATRC

AtriCure

Develops, manufactures, and sells devices for surgical ablation of cardiac tissue, exclusion of the left atrial appendage, and temporarily blocking pain by ablating peripheral nerves to medical centers in the United States, the Asia-Pacific, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|6.3% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.8% undervalued

GM

Community Contributor