- United States

- /

- Tobacco

- /

- NYSE:MO

Altria Group (NYSE:MO) Announces Quarterly Dividend of US$1.02 Per Share

Reviewed by Simply Wall St

Altria Group (NYSE:MO) recently affirmed its regular quarterly dividend of $1.02 per share, marking consistency in its shareholder returns amid its share price increase of 9% over the last quarter. This upward trajectory coincides with market indices, such as the S&P 500, adding to investor confidence. Despite reporting a dip in quarterly sales and net income compared to the previous year, the company's share re-purchase activity and consistent dividend declarations likely added weight to the broader market's positive movement, offering reassurance to investors navigating the mixed economic indicators and ongoing geopolitical developments.

Altria Group's (NYSE:MO) decision to maintain its quarterly dividend, as stated in the introduction, aligns with its history of consistent shareholder returns. Over the past five years, the total shareholder return was 130.73%, indicating a robust longer-term performance. This compares favorably with a 20.5% earnings growth over the past year, which exceeded the broader US Market's return of 11.2% and the US Tobacco industry's 5.1% return in the same timeframe. Although the company's recent quarterly sales and net income reported declines, its firm dividend and buyback activities continue to bolster investor sentiments.

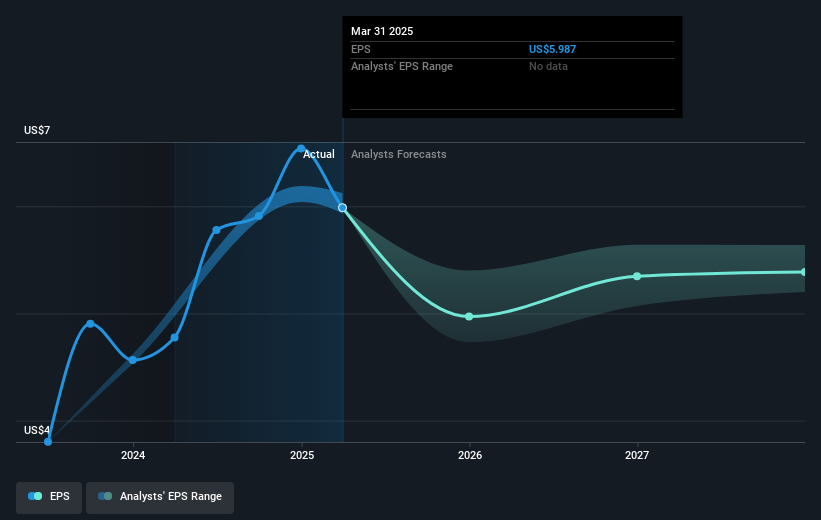

The recent developments regarding Altria's price dynamics and consensus analyst price target of US$58.37 offer crucial insights. With its current share price at US$60.48, it's only slightly above the target, suggesting that analysts view the stock as nearly fairly valued. This near-parity may influence revenue and earnings forecasts, particularly given the outlined regulatory and economic challenges. Analysts expect some decline in revenue and profit margins over the next few years, partially due to competition and regulatory issues in the e-vapor category. Should these affect consumer behavior or operational costs significantly, they might alter the anticipated stability in Altria's earnings and the stokc's long-term valuation.

Review our historical performance report to gain insights into Altria Group's track record.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MO

Altria Group

Through its subsidiaries, manufactures and sells smokeable and oral tobacco products in the United States.

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Community Narratives