PepsiCo (PEP) shares have recently seen a slight increase, catching the attention of investors curious about its performance over the past month. The company’s steady results and long-term returns continue to invite closer examination.

PepsiCo’s share price has climbed nearly 8% over the past month, suggesting renewed optimism after a stretch of weaker performance. Despite this momentum, the total shareholder return has been negative over the past year, reminding investors to keep an eye on the bigger picture as sentiment shifts.

With recent gains and a strong long-term track record, investors may wonder if PepsiCo’s current price reflects its growth potential or if there is still an opportunity to buy before the market fully recognizes it.

Advertisement

Most Popular Narrative: 70% Undervalued

PepsiCo’s most followed narrative values shares at much more than the recent close, citing major strategic changes and growth drivers that could reshape its market standing. Investors are watching whether anticipated international gains and evolving product portfolios can justify the stark disconnect to the market price.

Operational efficiencies from technology investments, including AI, ERP systems, and the integration of North American businesses, are enabling ongoing multiyear productivity gains. These initiatives are lowering fixed and variable costs and supporting net margin improvement. (Expected impact: Operating margins and long-term earnings.)

Curious about the bold financial moves and efficiency assumptions behind this valuation gap? Unlock what lies at the heart of these forecasts and how market leadership, not just numbers, is driving the story. Will future margins really leap, and what’s fueling the optimism? See the details behind the headline growth and profit expectations. Read the full narrative to get the inside scoop.

However, slower adoption of healthier products and ongoing input cost pressures could challenge PepsiCo’s growth and test the strength of this optimistic narrative.

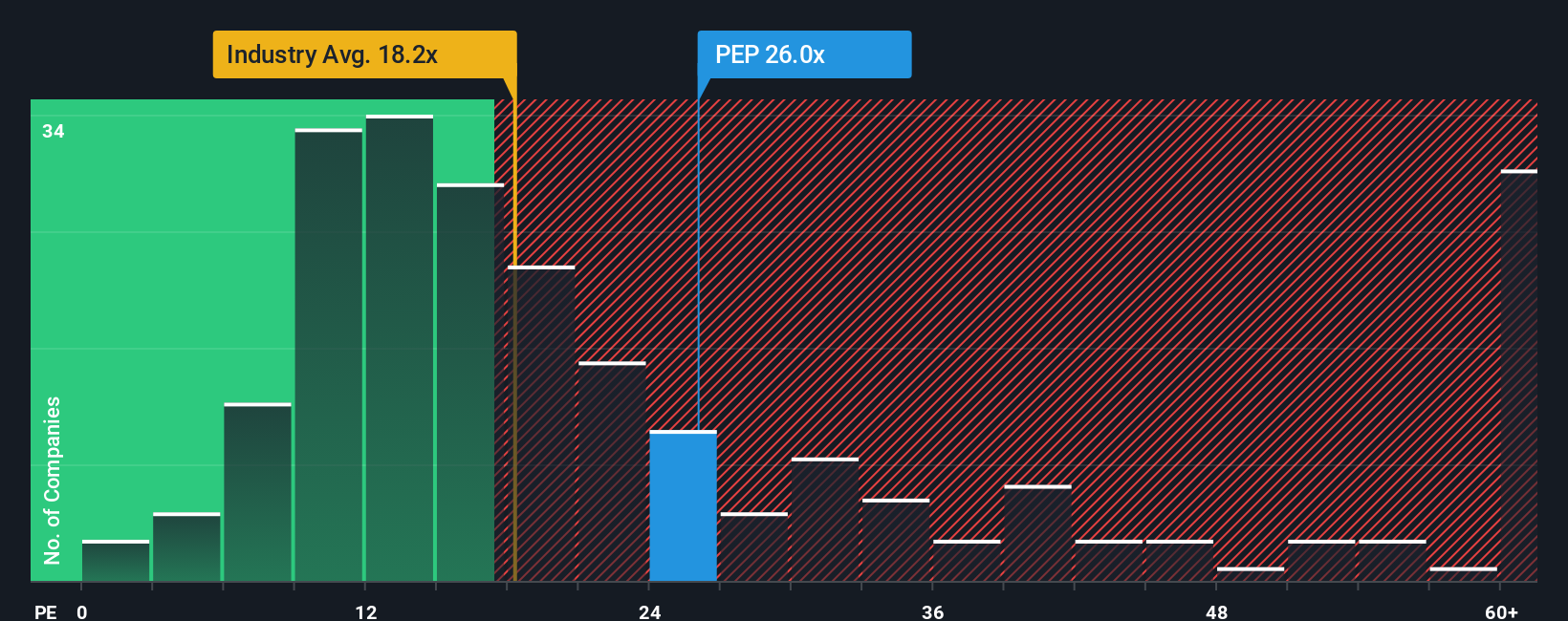

Another way to value PepsiCo is by comparing its price-to-earnings ratio to industry benchmarks. Currently, PepsiCo trades at 28.7 times earnings, which is significantly more expensive than both the global beverage industry average (17.7x) and its peer average (26.1x). The fair ratio estimate, based on historical trends, sits slightly higher at 29.3x. This suggests the market may eventually narrow the gap, but at this price, investors are paying up for perceived quality. Does this premium reflect real potential, or is there caution in these high expectations?

If you have a different perspective, or want to investigate the numbers for yourself, it's easy to shape your own analysis in just minutes. Do it your way

Smart investors never settle for just one opportunity. Stay ahead of the market by putting your money to work where trends, innovation, and value meet real potential.

Seize new trends in medicine and innovation by reviewing these 33 healthcare AI stocks, where artificial intelligence powers advancements in healthcare outcomes and investment potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks