- United States

- /

- Food

- /

- NasdaqGS:KHC

Does Kraft Heinz’s 21% 2025 Slide Signal a Growing Value Opportunity?

Reviewed by Bailey Pemberton

- If you are wondering whether Kraft Heinz is quietly turning into a value play while the market looks elsewhere, you are not alone, and the numbers are starting to get interesting.

- Despite a modest decline of around 1.4% over the last week and 4.5% over the last month, the stock is down roughly 21.5% year to date and 16.0% over the past year. This naturally raises the question of whether the market has gone too far on the downside.

- Recently, sentiment around Kraft Heinz has been shaped by ongoing cost-cutting initiatives, portfolio simplification, and efforts to reinvest in core brands as management aims to stabilize growth. At the same time, investors are weighing macro pressures on consumer staples and shifting shopper preferences. This helps explain why the share price has drifted even as the underlying business remains resilient.

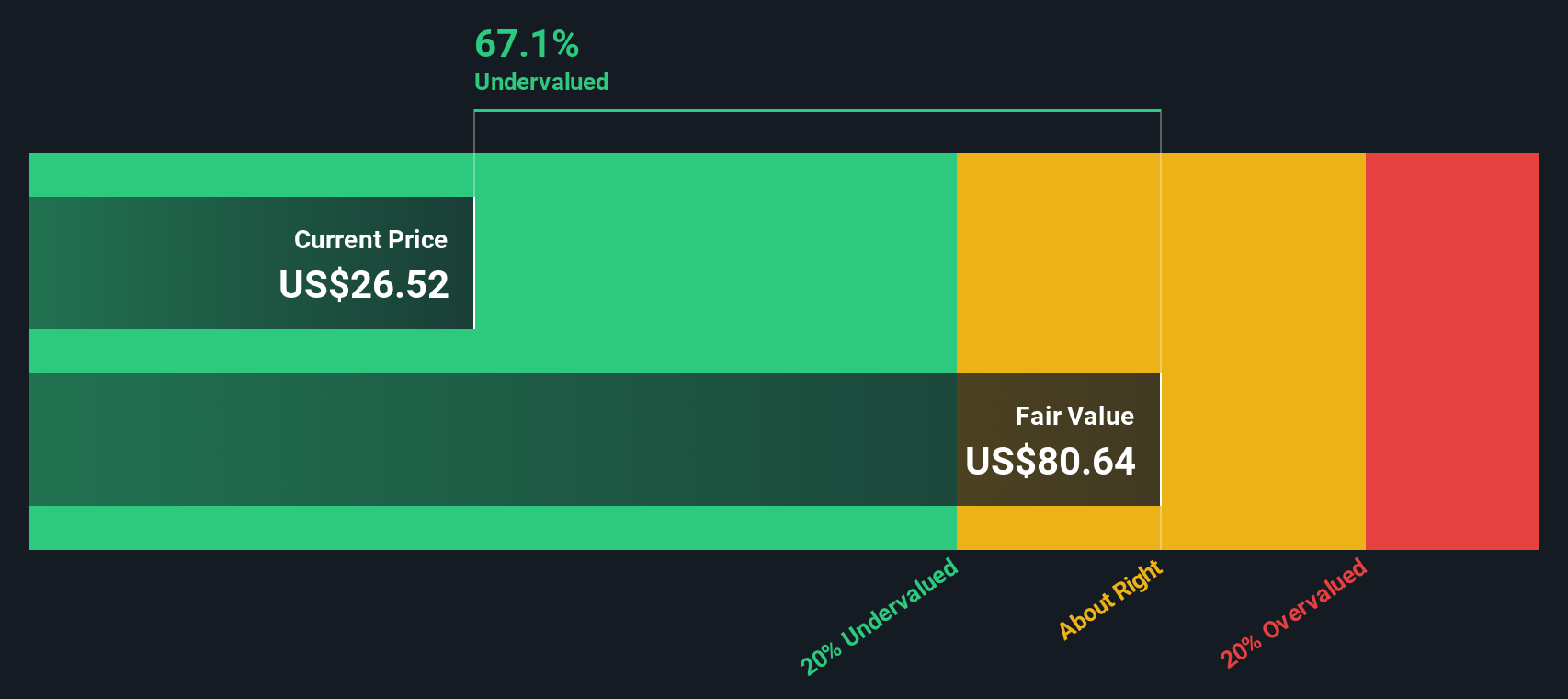

- On our framework, Kraft Heinz scores a 4 out of 6 valuation checks, suggesting the stock screens as undervalued on most metrics. Next, we will unpack those different valuation approaches before circling back to a more comprehensive way to think about its true worth.

Find out why Kraft Heinz's -16.0% return over the last year is lagging behind its peers.

Approach 1: Kraft Heinz Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting its future cash flows and discounting them back to the present. For Kraft Heinz, the model uses a 2 Stage Free Cash Flow to Equity approach based on $3.54 billion of last twelve months free cash flow, then extends analyst forecasts and Simply Wall St extrapolations over the coming years.

Analysts project free cash flow of about $3.22 billion in 2026, rising gradually to roughly $3.99 billion by 2035. This steady growth path, combined with an appropriate discount rate, leads to an estimated intrinsic value of $68.79 per share under the DCF model.

Compared with the current share price, this indicates Kraft Heinz is trading at roughly a 64.9% discount to its calculated fair value. This suggests the market is pricing in far weaker long term cash generation than the model assumes.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Kraft Heinz is undervalued by 64.9%. Track this in your watchlist or portfolio, or discover 899 more undervalued stocks based on cash flows.

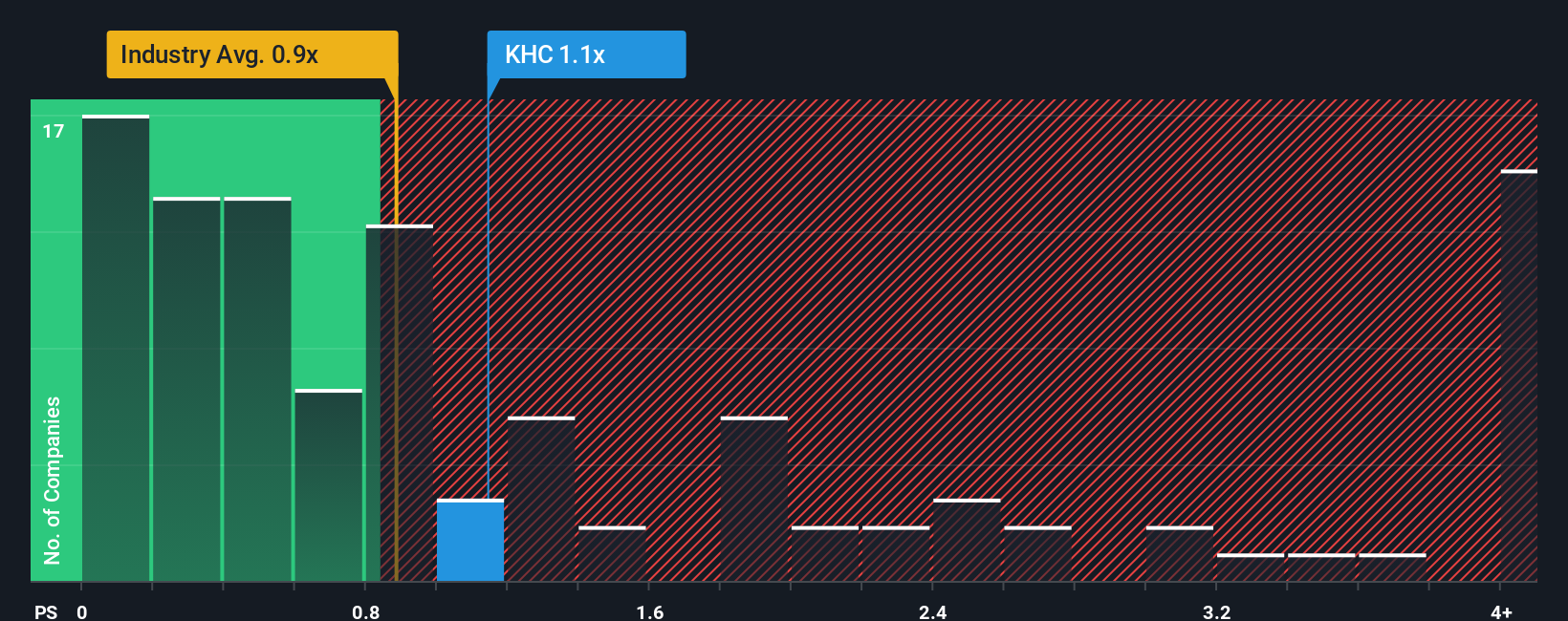

Approach 2: Kraft Heinz Price vs Sales

For consumer staples like Kraft Heinz, the price to sales ratio is a useful yardstick because revenue tends to be steadier than earnings, which can be distorted by restructuring charges, interest costs, or accounting items. Investors are essentially asking how many dollars they are willing to pay for each dollar of sales, given the company’s growth prospects and risk profile.

In general, faster growing and less risky businesses can justify higher price to sales multiples, while slower or more cyclical companies should trade on lower multiples. Kraft Heinz currently trades on a price to sales ratio of about 1.14x. That sits above the broader Food industry average of roughly 0.66x, but below the peer group average of around 1.94x, indicating the market is assigning it a mid range valuation within its space.

Simply Wall St’s Fair Ratio for Kraft Heinz is 1.38x, which is a proprietary estimate of what a reasonable price to sales multiple should be once you factor in the company’s expected growth, profitability, industry dynamics, size, and risk profile. This is more informative than a simple peer or industry comparison because it is tailored to Kraft Heinz’s specific fundamentals. With the stock trading at 1.14x versus a Fair Ratio of 1.38x, the shares screen as modestly undervalued on this metric.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1458 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Kraft Heinz Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are simple, story driven views of a company that connect your assumptions about Kraft Heinz’s future revenue, earnings, and margins to a financial forecast and then to a personal fair value estimate. All of this is available within an easy tool on Simply Wall St’s Community page that millions of investors use to decide when to buy or sell by comparing their Fair Value to the current share price. Each Narrative updates dynamically as fresh news or earnings arrive. For example, one Kraft Heinz investor might build an optimistic Narrative around accelerating innovation, improving margins near 12.7%, and a recovery toward a fair value in the low $50s. Another might construct a more cautious Narrative focused on weaker guidance, slower growth near 0.5%, and a fair value anchored in the high $20s. Both are using the same framework to turn their views into numbers and actionable decisions.

Do you think there's more to the story for Kraft Heinz? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Kraft Heinz might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:KHC

Kraft Heinz

Manufactures and markets food and beverage products in North America and internationally.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion