- United States

- /

- Food

- /

- NasdaqGS:HAIN

Hain Celestial Group (HAIN): Evaluating Valuation After Garden Veggie Snacks Relaunch and Recent Earnings Decline

Reviewed by Kshitija Bhandaru

If you’ve been eyeing Hain Celestial Group (HAIN) lately, the recent shake-up in its Garden Veggie Snacks line is probably grabbing your attention. The brand’s biggest recipe overhaul ever, featuring avocado oil snacks, sweet potato straws, and revamped packaging, hits Target shelves soon and aims firmly at parents and kids with a promise of healthier, tastier options. But investors know there’s more to the story, especially since this announcement landed alongside deeply negative earnings news and a wave of goodwill and asset impairment charges.

Despite the excitement around this product launch, Hain Celestial Group’s share price has been on a rollercoaster. The company’s stock fell over the past month, even as it clawed back some ground in the last quarter. Over the past year, the share price remains sharply down, reflecting both operational challenges and the market’s cautious mood. The company’s steady revenue base is now offset by significant losses and asset write-downs, leaving investors searching for signs of turnaround momentum.

Which brings us to the big question: are markets underestimating Hain’s turnaround potential, or is the current valuation already factoring in all the risks and possible upside?

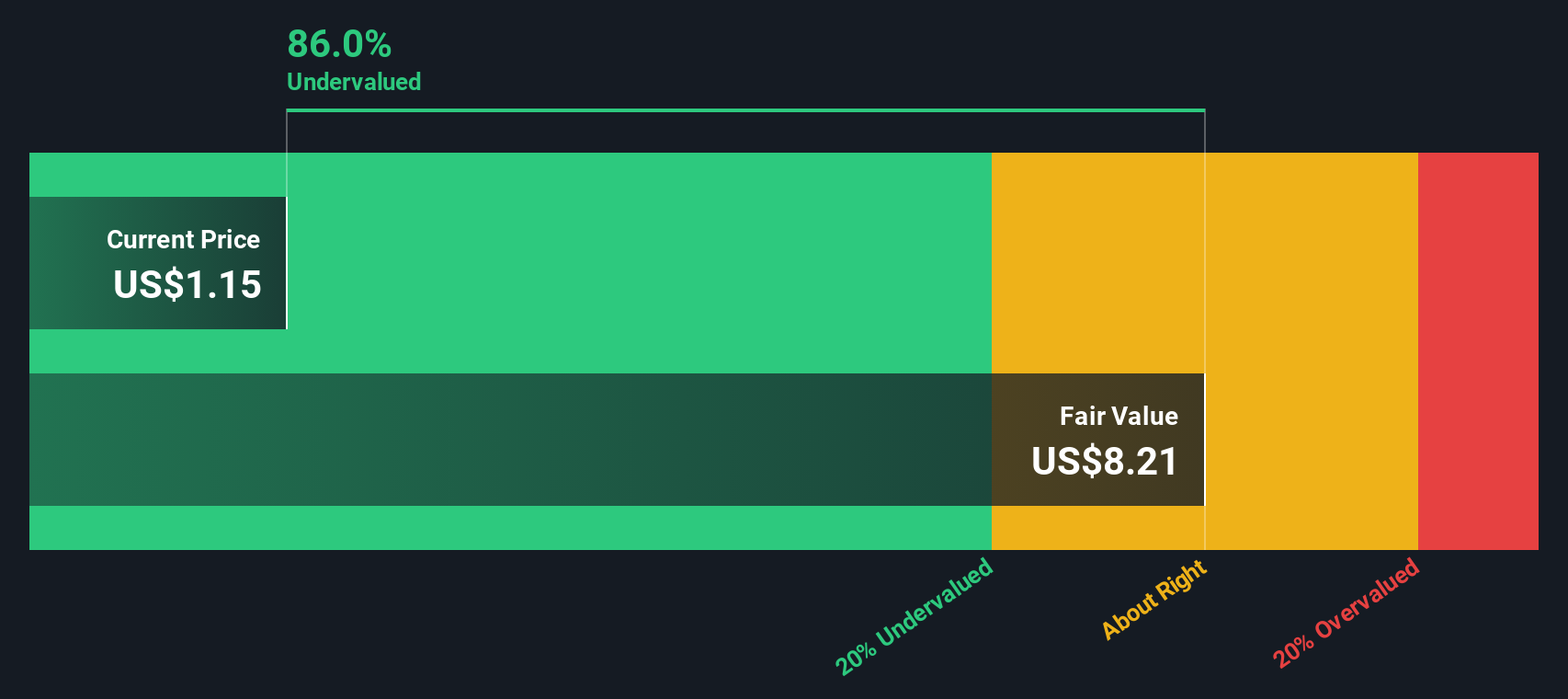

Most Popular Narrative: 42.9% Undervalued

The prevailing narrative views Hain Celestial Group as deeply undervalued by the market, with analysts suggesting significant upside based on their forecast of future financial improvements and operational changes.

The leadership transition to Alison Lewis, who has a track record of driving superior in-market execution and disciplined revenue growth, is expected to enhance operational efficiency and support revenue and earnings improvement. The strategic review of the company's portfolio with Goldman Sachs as the financial advisor aims to explore options that could enhance shareholder value and potentially lead to better financial health and improved earnings.

Is Wall Street missing something in this turnaround story? The calculation fueling this bold valuation hinges on a transformation few expect. The heart of the narrative is built on aggressive numbers you will not find elsewhere. Want to unlock the financial levers powering this 40% discount? Dive in to see what is driving analysts’ optimism.

Result: Fair Value of $2.87 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, ongoing leadership instability and lagging performance in core product categories could derail Hain’s anticipated turnaround and challenge analysts' optimistic case.

Find out about the key risks to this Hain Celestial Group narrative.Another View: What Does the SWS DCF Model Say?

Looking at Hain Celestial Group through our SWS DCF model, the results echo the earlier undervaluation call but come from a deeper analysis of the company's long-term cash flows and potential. Are both methods seeing something the market is missing, or is this just a reflection of hope?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Hain Celestial Group Narrative

If you see things differently or want to dig into the numbers on your own, building your own narrative takes just a few minutes and puts the evidence in your hands. Do it your way

A great starting point for your Hain Celestial Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Why settle for just one opportunity? Use the Simply Wall Street Screener to target high-potential stocks that match your goals and stay ahead of other investors racing for the best ideas.

- Tap into value by targeting companies that may be flying under the radar as truly undervalued stocks based on cash flows.

- Accelerate your research with market favorites in artificial intelligence. See which businesses are capturing huge momentum as AI penny stocks.

- Take a closer look at steady income opportunities with shares offering attractive payouts, including dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hain Celestial Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HAIN

Hain Celestial Group

Manufactures, markets, and sells organic and natural products in the United States, United Kingdom, Europe, and internationally.

Undervalued with imperfect balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion