Advertisement

- United States

- /

- Food

- /

- NasdaqGS:HAIN

Capital Allocation Trends At Hain Celestial Group (NASDAQ:HAIN) Aren't Ideal

If we're looking to avoid a business that is in decline, what are the trends that can warn us ahead of time? More often than not, we'll see a declining return on capital employed (ROCE) and a declining amount of capital employed. Trends like this ultimately mean the business is reducing its investments and also earning less on what it has invested. So after we looked into Hain Celestial Group (NASDAQ:HAIN), the trends above didn't look too great.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Hain Celestial Group, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

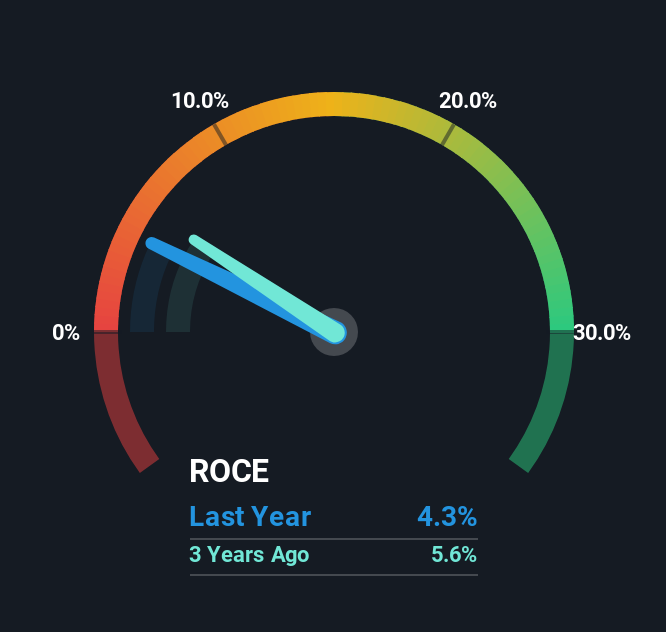

0.043 = US$57m ÷ (US$1.6b - US$277m) (Based on the trailing twelve months to June 2025).

So, Hain Celestial Group has an ROCE of 4.3%. In absolute terms, that's a low return and it also under-performs the Food industry average of 9.0%.

See our latest analysis for Hain Celestial Group

In the above chart we have measured Hain Celestial Group's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Hain Celestial Group for free.

What Does the ROCE Trend For Hain Celestial Group Tell Us?

In terms of Hain Celestial Group's historical ROCE trend, it isn't fantastic. Unfortunately, returns have declined substantially over the last five years to the 4.3% we see today. What's equally concerning is that the amount of capital deployed in the business has shrunk by 30% over that same period. The combination of lower ROCE and less capital employed can indicate that a business is likely to be facing some competitive headwinds or seeing an erosion to its moat. Typically businesses that exhibit these characteristics aren't the ones that tend to multiply over the long term, because statistically speaking, they've already gone through the growth phase of their life cycle.

In Conclusion...

In short, lower returns and decreasing amounts capital employed in the business doesn't fill us with confidence. Unsurprisingly then, the stock has dived 95% over the last five years, so investors are recognizing these changes and don't like the company's prospects. With underlying trends that aren't great in these areas, we'd consider looking elsewhere.

If you'd like to know about the risks facing Hain Celestial Group, we've discovered 1 warning sign that you should be aware of.

While Hain Celestial Group isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Valuation is complex, but we're here to simplify it.

Discover if Hain Celestial Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:HAIN

Hain Celestial Group

Manufactures, markets, and sells organic and natural products in the United States, United Kingdom, Europe, and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor