Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:TALO

Talos Energy (TALO): Revenue Forecast to Decline 3.4% Annually, Valuation Discount Sharpens Investor Debate

Simply Wall St

Reviewed by Simply Wall St

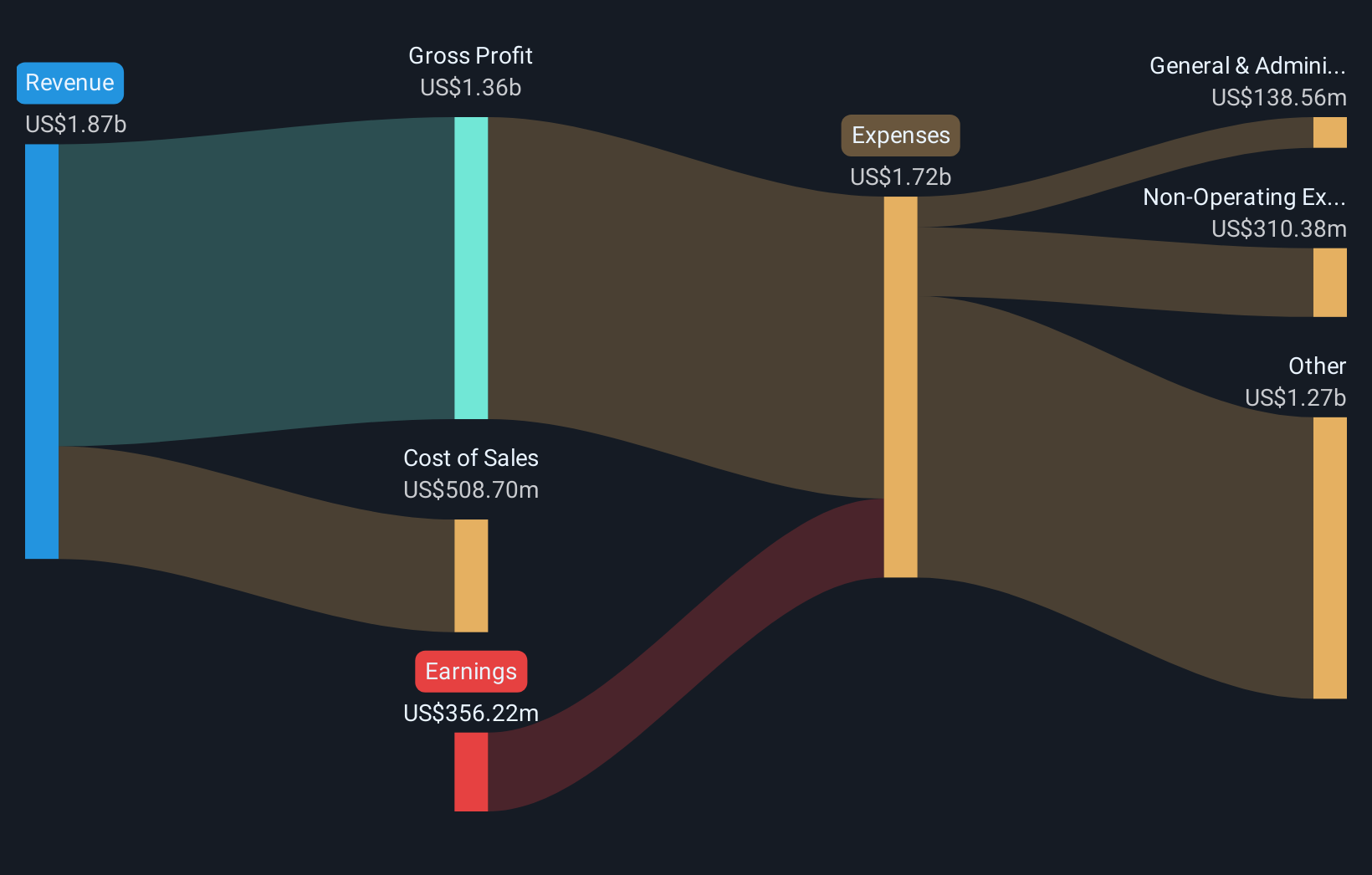

Talos Energy (TALO) remains unprofitable, with forecasts calling for continued losses over the next three years and revenue projected to decline at an annual rate of 3.4%. Over the past five years, the company has narrowed its losses by 28.1% per year, but has not yet shown improved earnings margins due to persistent negative results. While near-term prospects remain pressured, investors may see potential amid ongoing loss reduction and a significant valuation discount compared to peers.

See our full analysis for Talos Energy.Next, we’ll see how these results hold up against the ongoing market narrative. Some investor expectations could be confirmed, while others might be up for debate.

See what the community is saying about Talos Energy

Margin Expansion Hinges on $100 Million Efficiency Push

- Talos is enacting a targeted $100 million per year plan in operational efficiencies and cost reduction, aiming to have a sustainable, recurring impact on free cash flow starting in 2026.

- Analysts' consensus view highlights that operational improvements and disciplined capital allocation are set to drive gains in margins and recurring free cash flow. However, this will depend on Talos executing its cost strategy amid continued industry and regulatory pressures.

- Consensus notes that recurring cost savings and margin gains could enhance financial resilience. Analysts caution that the lack of visible margin improvement so far points to execution risk.

- The interplay between future cost discipline and current negative earnings margins is a major pivot point for whether Talos can narrow its losses as forecast.

- The latest numbers amplify the debate on Talos's pathway to steady free cash flow and set the stage for a deeper dive into industry comparisons. Discover the analysts' reasoning behind the consensus view. 📊 Read the full Talos Energy Consensus Narrative.

Share Buyback Flexibility Backed by $1 Billion Liquidity

- Talos boasts a robust liquidity position of $1 billion alongside leverage at only 0.7x, supporting a policy of programmatic share buybacks up to 50% of annual free cash flow.

- According to analysts' consensus view, this financial flexibility underpins shareholder return potential, even as core operations face ongoing losses into the medium term.

- Consensus suggests Talos’s ample financial resources enable opportunistic M&A and buybacks, helping cushion investor downside while waiting for margin improvements to materialize.

- The narrative, however, flags that persistent unprofitability could erode the company’s ability to fund these programs over time, especially if free cash flow remains constrained.

Discounted Valuation Versus Industry and DCF Fair Value

- Talos trades at a price-to-sales ratio of 0.9x, below both the industry average (1.4x) and peers (1.8x), and with the current market price of $9.78 sitting well under the DCF fair value estimate of $34.75.

- Analysts' consensus view holds that this deep valuation discount offers compelling upside for investors who believe the company’s margin recovery story. Analysts caution that continued operating losses may justify some of the current discount unless profitability materializes.

- Consensus underscores that, with the analyst price target at $12.82, there is at least a 31% gap from today’s price. This assumes buy-side confidence in future margin convergence.

- The tension between a depressed valuation and absent profitability creates a classic value-versus-quality dynamic for prospective shareholders.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Talos Energy on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Looking at the figures from another angle? In just a few minutes, you can craft your own story and shape the outlook: Do it your way

A great starting point for your Talos Energy research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

Talos Energy faces ongoing losses, negative earnings margins, and uncertain margin recovery, making consistent profitability and dependable performance a concern for investors.

If steady results matter most to you, switch focus to stable growth stocks screener (2078 results). Discover companies that deliver reliable revenue and earnings through all market conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Talos Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TALO

Talos Energy

Through its subsidiaries, engages in the exploration and production of oil, natural gas, and natural gas liquids in the United States and Mexico.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor