Advertisement

- United States

- /

- Energy Services

- /

- NYSE:RIG

Transocean (RIG): Evaluating Valuation After Earnings Beat, Strong Utilization, and New Contract Wins

Simply Wall St

Reviewed by Simply Wall St

Transocean (NYSE:RIG) just posted its third-quarter earnings, delivering adjusted earnings and revenue that surpassed expectations. Strong rig utilization and recent contract wins have sparked renewed attention from investors this month.

See our latest analysis for Transocean.

Transocean’s recent contract wins and upbeat quarterly results have reignited investor interest, fueling a staggering 36.7% 90-day share price return. While momentum has clearly picked up in the short term, the total shareholder return over the past year is still down 9.4%, which reflects ongoing volatility in the sector and a cautious longer-term view despite recent operational wins.

If strong sector moves like this catch your attention, it is a great moment to broaden your perspective and discover fast growing stocks with high insider ownership

After this rally and a set of strong operating results, is Transocean still trading below its true value, or has the market already factored in the company’s turnaround and future growth prospects?

Most Popular Narrative: 100% Undervalued

With the narrative's fair value estimate of $3.88 well above Transocean's last close at $3.84, bullish sentiment is mounting around the company's future earnings turnaround. Expectations are clearly set for a sharp change in Transocean’s fortunes, rooted in major improvements to dayrates and contract quality.

Rising global energy demand and the ongoing depletion of easily accessible onshore oil reserves are driving sustained investment in offshore and ultra-deepwater exploration. This is leading to a tightening rig market and rising dayrates, which are poised to boost Transocean's revenue and EBITDA as utilization approaches or exceeds 90% in late 2026 and 2027.

Want to know the growth blueprint behind this high valuation? The key element of this narrative is record-breaking earnings and a future profit multiple usually associated with tech leaders. Interested in which bold financial projections support that price target? Dive deeper to see the surprising numbers that drive this fair value calculation.

Result: Fair Value of $3.88 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent volatility in offshore dayrates and Transocean’s heavy debt load could put pressure on profitability and challenge the upbeat turnaround scenario.

Find out about the key risks to this Transocean narrative.

Another View: Are Multiples Sending a Different Signal?

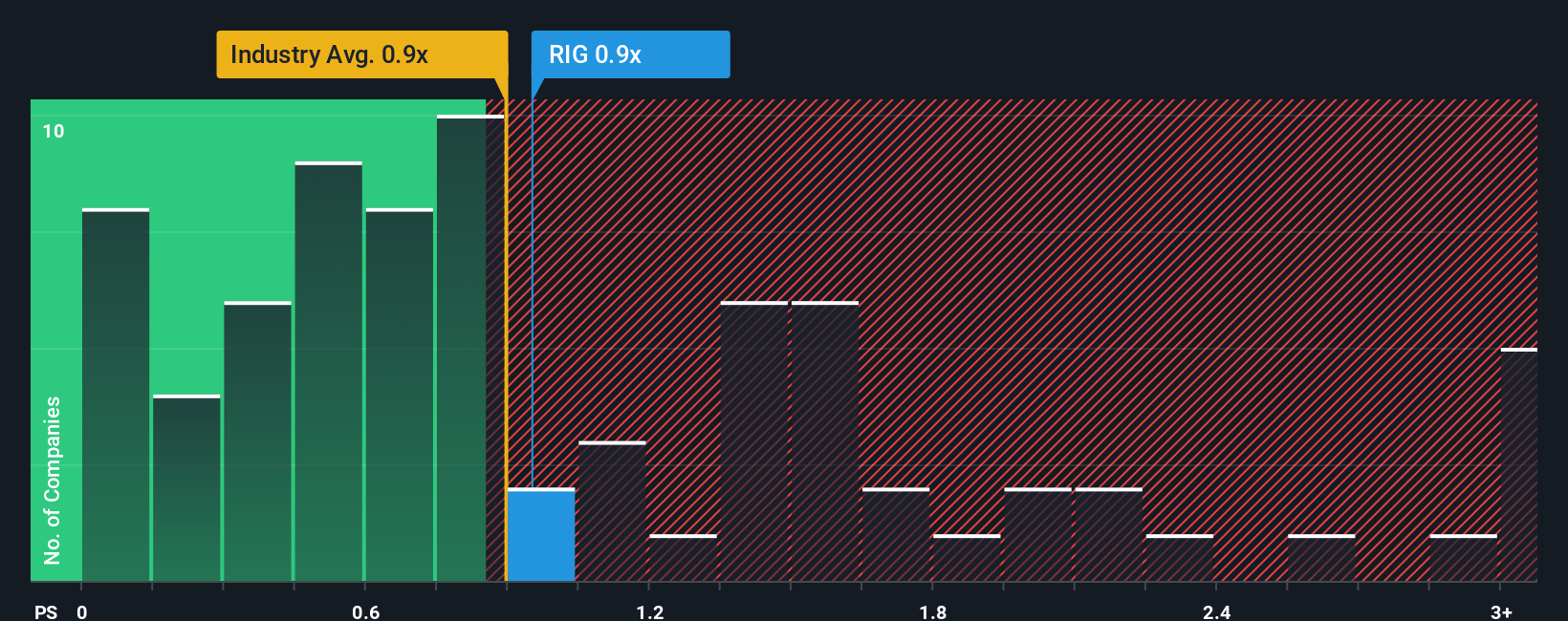

While the narrative points to Transocean being undervalued based on future earnings potential, a look at its price-to-sales ratio tells another story. At 1.1x, Transocean appears more expensive than both the US Energy Services industry average and its peer group, both at 1x. This difference suggests the market is counting on more aggressive growth or profitability than the sector norm, which adds a layer of risk for investors if expectations fall short. Should multiples like these make you pause?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Transocean Narrative

Prefer to chart your own path or dig deeper into the figures behind Transocean? You can quickly craft your own narrative in just a few minutes: Do it your way.

A great starting point for your Transocean research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors never settle for a single opportunity. Position yourself for growth by uncovering stocks with standout potential using these unique searches from Simply Wall Street:

- Uncover powerhouse companies targeting strong yields and steady income by checking out these 22 dividend stocks with yields > 3% to see who's delivering above 3% today.

- Take the lead in the AI revolution with fast-moving opportunities among these 26 AI penny stocks that are driving innovation across industries right now.

- Capitalize on hidden value and snap up bargains by reviewing these 840 undervalued stocks based on cash flows before the market spots them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Transocean might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:RIG

Transocean

Provides offshore contract drilling services for oil and gas wells in Switzerland and internationally.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor