Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:PRT

Why It Might Not Make Sense To Buy PermRock Royalty Trust (NYSE:PRT) For Its Upcoming Dividend

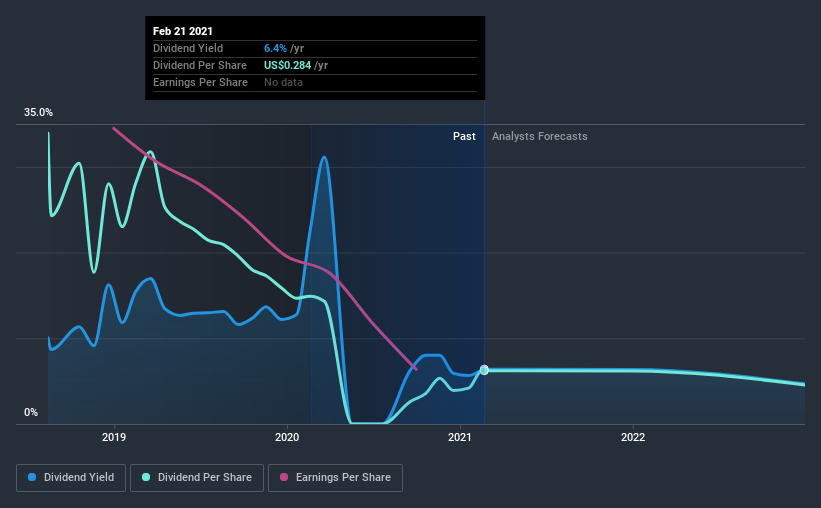

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see PermRock Royalty Trust (NYSE:PRT) is about to trade ex-dividend in the next two days. You can purchase shares before the 25th of February in order to receive the dividend, which the company will pay on the 12th of March.

PermRock Royalty Trust's next dividend payment will be US$0.024 per share. Last year, in total, the company distributed US$0.12 to shareholders. Last year's total dividend payments show that PermRock Royalty Trust has a trailing yield of 6.4% on the current share price of $4.45. If you buy this business for its dividend, you should have an idea of whether PermRock Royalty Trust's dividend is reliable and sustainable. We need to see whether the dividend is covered by earnings and if it's growing.

View our latest analysis for PermRock Royalty Trust

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. PermRock Royalty Trust paid out 100% of its earnings, which is more than we're comfortable with, unless there are mitigating circumstances.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. PermRock Royalty Trust's earnings per share plummeted 29% over the past year,which is rarely good news for the dividend.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. PermRock Royalty Trust has seen its dividend decline 43% per annum on average over the past three years, which is not great to see. While it's not great that earnings and dividends per share have fallen in recent years, we're encouraged by the fact that management has trimmed the dividend rather than risk over-committing the company in a risky attempt to maintain yields to shareholders.

To Sum It Up

Is PermRock Royalty Trust worth buying for its dividend? Earnings per share are in decline and PermRock Royalty Trust is paying out what we feel is an uncomfortably high percentage of its profit as dividends. Generally we think dividend investors should avoid businesses in this situation, as high payout ratios and declining earnings can lead to the dividend being cut. These characteristics don't generally lead to outstanding dividend performance, and investors may not be happy with the results of owning this stock for its dividend.

With that in mind though, if the poor dividend characteristics of PermRock Royalty Trust don't faze you, it's worth being mindful of the risks involved with this business. We've identified 5 warning signs with PermRock Royalty Trust (at least 2 which don't sit too well with us), and understanding them should be part of your investment process.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

When trading PermRock Royalty Trust or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:PRT

PermRock Royalty Trust

Operates as a statutory trust in the United States.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor