Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:OXY

Should Record Permian Production and Debt Reduction Shift the Outlook for Occidental Petroleum (OXY) Investors?

Simply Wall St

Reviewed by Sasha Jovanovic

- Occidental Petroleum recently exceeded its third quarter expectations, posting record Permian production, reducing lease operating expenses to their lowest level since 2021, and repaying US$1.3 billion of debt, with a plan to lower total debt below US$15 billion after an OxyChem sale.

- The company also increased capital returns to shareholders through dividends and buybacks, and is anticipated to raise its dividend next quarter, reflecting greater financial flexibility and ongoing commitment to shareholder returns.

- We'll examine how record production and disciplined cost reductions strengthen Occidental Petroleum's investment narrative and future earnings outlook.

We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Occidental Petroleum Investment Narrative Recap

To be a shareholder in Occidental Petroleum today, you need to believe that the company’s ability to deliver strong oil and gas production while maintaining disciplined capital allocation will outweigh industry risks such as commodity price volatility. The recent quarterly results reinforced production momentum and cost discipline, but these developments may not meaningfully reduce Occidental’s sensitivity to oil prices in the near term, which remains the most important catalyst and risk for investors right now.

One relevant highlight from recent announcements is Occidental’s plan to reduce total debt below US$15 billion following the sale of its OxyChem business. This move directly addresses the company’s elevated leverage and aims to bolster balance sheet flexibility, a key catalyst for offsetting oil price headwinds and supporting further shareholder returns.

But despite strengthened operations, investors should not overlook the ongoing risk tied to potential oil demand declines and...

Read the full narrative on Occidental Petroleum (it's free!)

Occidental Petroleum is projected to reach $29.0 billion in revenue and $3.7 billion in earnings by 2028. This reflects a 2.2% annual revenue growth rate and a $2.0 billion increase in earnings from the current $1.7 billion.

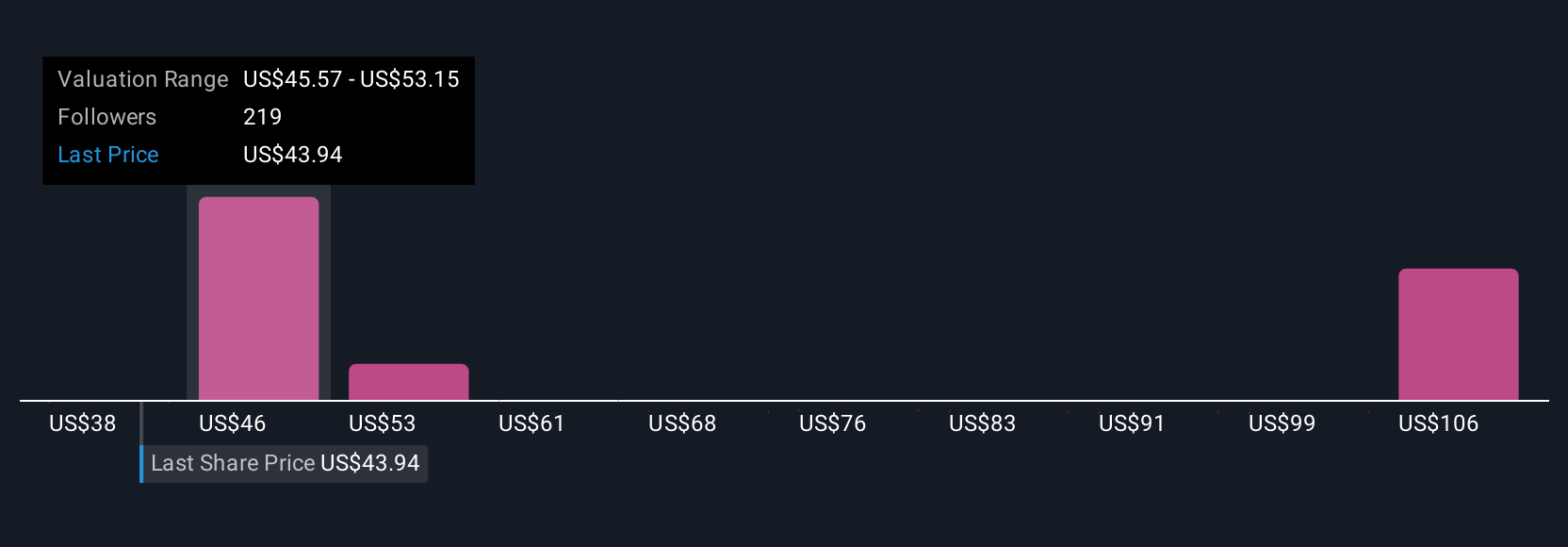

Uncover how Occidental Petroleum's forecasts yield a $50.21 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Twenty-six members of the Simply Wall St Community estimate fair values for Occidental between US$31.19 and US$69.65 per share. While cash flow resilience is a key catalyst, wide differences in expectations underline how much opinions can vary, explore several viewpoints to make a more informed judgment.

Explore 26 other fair value estimates on Occidental Petroleum - why the stock might be worth 25% less than the current price!

Build Your Own Occidental Petroleum Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Occidental Petroleum research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Occidental Petroleum research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Occidental Petroleum's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 35 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:OXY

Occidental Petroleum

Engages in the acquisition, exploration, and development of oil and gas properties in the United States and internationally.

Slight risk with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

135 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

83 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

923 followersusers have followed this narrative

5 commentsusers have commented on this narrative

22 likesusers have liked this narrative