Advertisement

- United States

- /

- Energy Services

- /

- NYSE:HLX

Is Helix Energy Solutions Group (NYSE:HLX) A Risky Investment?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Helix Energy Solutions Group, Inc. (NYSE:HLX) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Helix Energy Solutions Group

What Is Helix Energy Solutions Group's Debt?

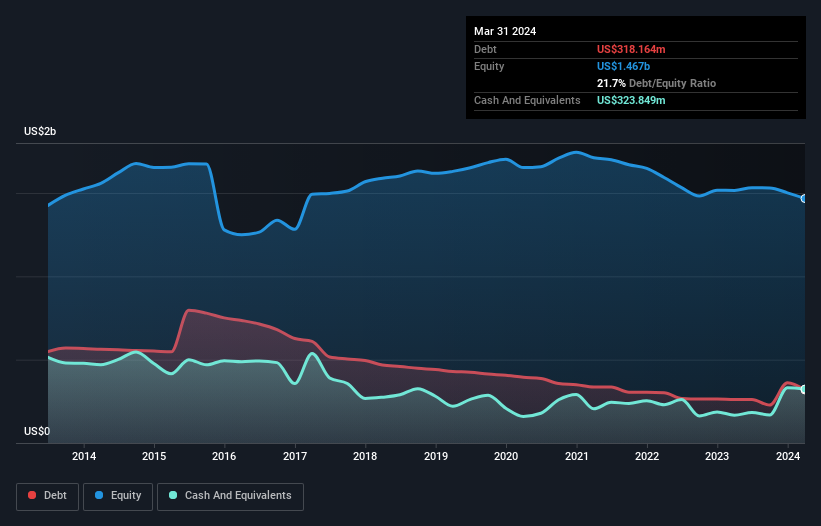

As you can see below, at the end of March 2024, Helix Energy Solutions Group had US$318.2m of debt, up from US$260.5m a year ago. Click the image for more detail. However, it does have US$323.8m in cash offsetting this, leading to net cash of US$5.69m.

A Look At Helix Energy Solutions Group's Liabilities

Zooming in on the latest balance sheet data, we can see that Helix Energy Solutions Group had liabilities of US$348.0m due within 12 months and liabilities of US$799.0m due beyond that. Offsetting this, it had US$323.8m in cash and US$225.8m in receivables that were due within 12 months. So its liabilities total US$597.3m more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Helix Energy Solutions Group has a market capitalization of US$1.78b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt. Despite its noteworthy liabilities, Helix Energy Solutions Group boasts net cash, so it's fair to say it does not have a heavy debt load!

Pleasingly, Helix Energy Solutions Group is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 4,465% gain in the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Helix Energy Solutions Group's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Helix Energy Solutions Group has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Helix Energy Solutions Group actually produced more free cash flow than EBIT over the last two years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing Up

While Helix Energy Solutions Group does have more liabilities than liquid assets, it also has net cash of US$5.69m. The cherry on top was that in converted 205% of that EBIT to free cash flow, bringing in US$206m. So is Helix Energy Solutions Group's debt a risk? It doesn't seem so to us. We'd be very excited to see if Helix Energy Solutions Group insiders have been snapping up shares. If you are too, then click on this link right now to take a (free) peek at our list of reported insider transactions.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Helix Energy Solutions Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:HLX

Helix Energy Solutions Group

An offshore energy services company, provides specialty services to the offshore energy industry in Brazil, the United States, North Sea, the Asia Pacific, West Africa, and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor