Advertisement

The board of Frontline plc (NYSE:FRO) has announced it will be reducing its dividend by 71% from last year's payment of $0.62 on the 24th of June, with shareholders receiving $0.18. This means the annual payment is 9.7% of the current stock price, which is above the average for the industry.

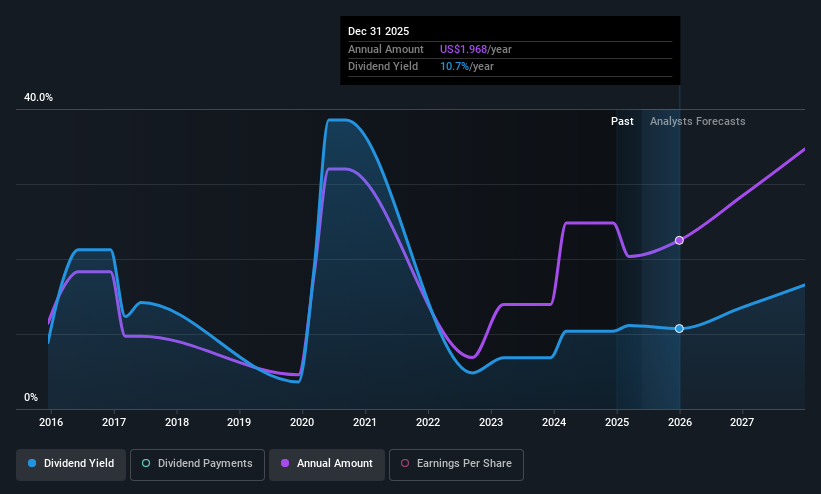

Frontline's Future Dividend Projections Appear Well Covered By Earnings

A big dividend yield for a few years doesn't mean much if it can't be sustained. Prior to this announcement, Frontline's dividend made up quite a large proportion of earnings but only 58% of free cash flows. In general, cash flows are more important than earnings, so we are comfortable that the dividend will be sustainable going forward, especially with so much cash left over for reinvestment.

Looking forward, earnings per share is forecast to rise by 93.2% over the next year. Assuming the dividend continues along the course it has been charting recently, our estimates show the payout ratio being 51% which brings it into quite a comfortable range.

Check out our latest analysis for Frontline

Frontline's Dividend Has Lacked Consistency

Even in its relatively short history, the company has reduced the dividend at least once. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. The annual payment during the last 9 years was $1.00 in 2016, and the most recent fiscal year payment was $1.78. This means that it has been growing its distributions at 6.6% per annum over that time. It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. Frontline might have put its house in order since then, but we remain cautious.

The Dividend's Growth Prospects Are Limited

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. However, Frontline's EPS was effectively flat over the past five years, which could stop the company from paying more every year. Earnings are not growing quickly at all, and the company is paying out most of its profit as dividends. This isn't the end of the world, but for investors looking for strong dividend growth they may want to look elsewhere.

Our Thoughts On Frontline's Dividend

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We would probably look elsewhere for an income investment.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. To that end, Frontline has 4 warning signs (and 1 which doesn't sit too well with us) we think you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:FRO

Frontline

A shipping company, engages in the ownership and operation of oil and product tankers worldwide.

Reasonable growth potential average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor