Frontline (NYSE:FRO) shares have caught the attention of traders this month, climbing by 10% over the past month. Investors seem to be re-evaluating the stock as its returns continue trending above industry peers.

Momentum is clearly building for Frontline, with a 26.6% share price return over the past 90 days and a year-to-date gain topping 76%. Even more compelling, its one-year total shareholder return stands at nearly 41%, handily outpacing its sector. The recent surge reflects renewed optimism about the company’s prospects, as investors look past short-term swings to its impressive multi-year performance and persistently strong demand signals.

But with shares up so dramatically, investors are left to wonder whether Frontline’s stock is still undervalued given its fundamentals or if the market has already priced in all the anticipated growth.

Advertisement

Most Popular Narrative: 6.8% Undervalued

Frontline's most popular narrative estimates a fair value of $27.80 per share compared to the last close of $25.90. This suggests the shares may still have upside potential if strong profit margin improvements are realized. This narrative considers recent margin momentum and improving fleet dynamics while also weighing potential market volatility.

Frontline's modern, eco-friendly fleet (average age 7 years, 100% ECO vessel, over 50% scrubber-fitted) positions the company to benefit from both stricter environmental regulations and higher fuel efficiency, helping to keep operating costs low and supporting better net margins as older, less efficient vessels are phased out.

What exactly is driving this target price? Hint: long-term margin expansion and profit forecasts are the focus, not revenue growth. The full narrative details the quantitative assumptions that are setting Frontline apart in this competitive sector. If you want to see the numbers behind this valuation, you’ll want to read further.

However, there are still risks, such as volatile oil demand and potential regulatory changes, that could challenge Frontline's optimistic outlook if industry conditions shift unexpectedly.

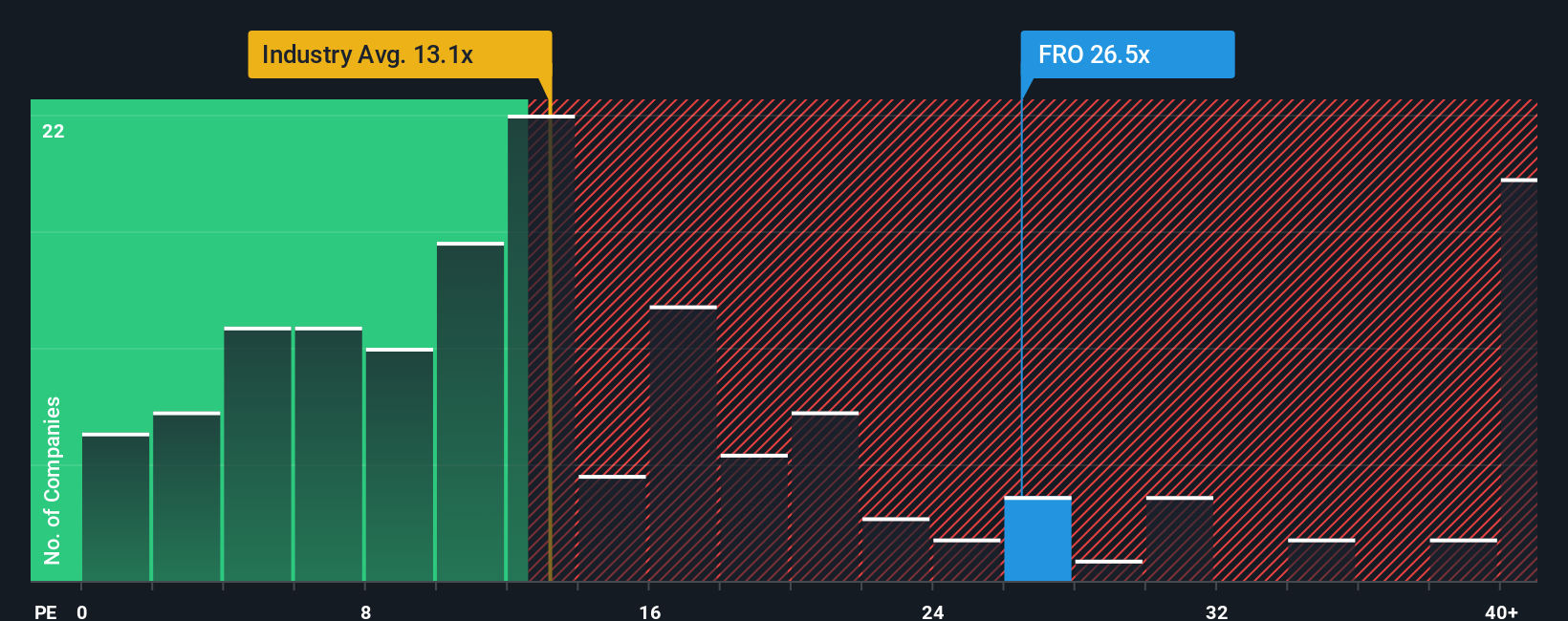

Looking from a market multiple perspective, Frontline is trading at a price-to-earnings ratio of 26.5x, which appears expensive relative to both the US Oil and Gas industry average of 13.1x and a fair ratio estimate of 25.3x. While this might reflect growth expectations, it poses valuation risks if those expectations are not met. Could the market be overvaluing momentum?

Opportunities don’t wait for anyone. Equip yourself with fresh stock ideas you might otherwise overlook by using these tailored tools from Simply Wall Street:

Tap into innovations in patient care and medical technology by targeting these 30 healthcare AI stocks, which are transforming the healthcare sector through advanced artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies