Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:FRO

Analysts Have Just Cut Their Frontline plc (NYSE:FRO) Revenue Estimates By 17%

The latest analyst coverage could presage a bad day for Frontline plc (NYSE:FRO), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative.

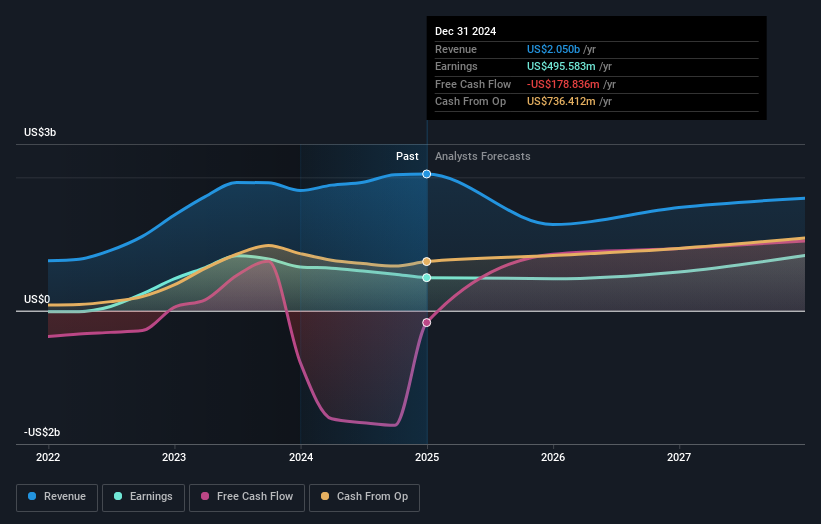

Following the latest downgrade, the seven analysts covering Frontline provided consensus estimates of US$1.3b revenue in 2025, which would reflect a concerning 37% decline on its sales over the past 12 months. Statutory earnings per share are supposed to decrease 7.6% to US$2.06 in the same period. Previously, the analysts had been modelling revenues of US$1.6b and earnings per share (EPS) of US$2.27 in 2025. Indeed, we can see that analyst sentiment has declined measurably after the new consensus came out, with a measurable cut to revenue estimates and a small dip in EPS estimates to boot.

See our latest analysis for Frontline

Analysts made no major changes to their price target of US$26.40, suggesting the downgrades are not expected to have a long-term impact on Frontline's valuation.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 37% by the end of 2025. This indicates a significant reduction from annual growth of 17% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 4.1% per year. It's pretty clear that Frontline's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Frontline. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Frontline's revenues are expected to grow slower than the wider market. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of Frontline going forwards.

After a downgrade like this, it's pretty clear that previous forecasts were too optimistic. What's more, we've spotted several possible issues with Frontline's business, like its declining profit margins. Learn more, and discover the 2 other concerns we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies backed by insiders.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:FRO

Frontline

A shipping company, engages in the ownership and operation of oil and product tankers worldwide.

Reasonable growth potential average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor