- United States

- /

- Oil and Gas

- /

- NYSE:EPD

Is Jim Cramer’s NGL Endorsement Altering The Investment Case For Enterprise Products Partners (EPD)?

Reviewed by Sasha Jovanovic

- Earlier this week, TV commentator Jim Cramer publicly highlighted Enterprise Products Partners as his preferred pick in its peer group, emphasizing its consistent distribution growth, strong yield, and deep expertise in natural gas liquids while playing down concerns around ethane and NGL softness.

- Investors appear to have reacted strongly to this endorsement, underscoring how influential media commentary can rapidly shift sentiment around a midstream operator that is otherwise seen as a long-term, cash-flow-focused business.

- Next, we’ll examine how Cramer’s upbeat view on Enterprise’s natural gas liquids position might influence the existing investment narrative built around its infrastructure expansion and capital allocation plans.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Enterprise Products Partners Investment Narrative Recap

To own Enterprise Products Partners, you need to believe in the durability of its fee-based midstream model, its long track record of distribution growth, and the importance of NGL infrastructure in North American energy flows. Cramer’s bullish comments and the short term price jump do not materially change the key near term story, which still centers on executing growth projects while managing a large debt load in a volatile macro and commodity backdrop.

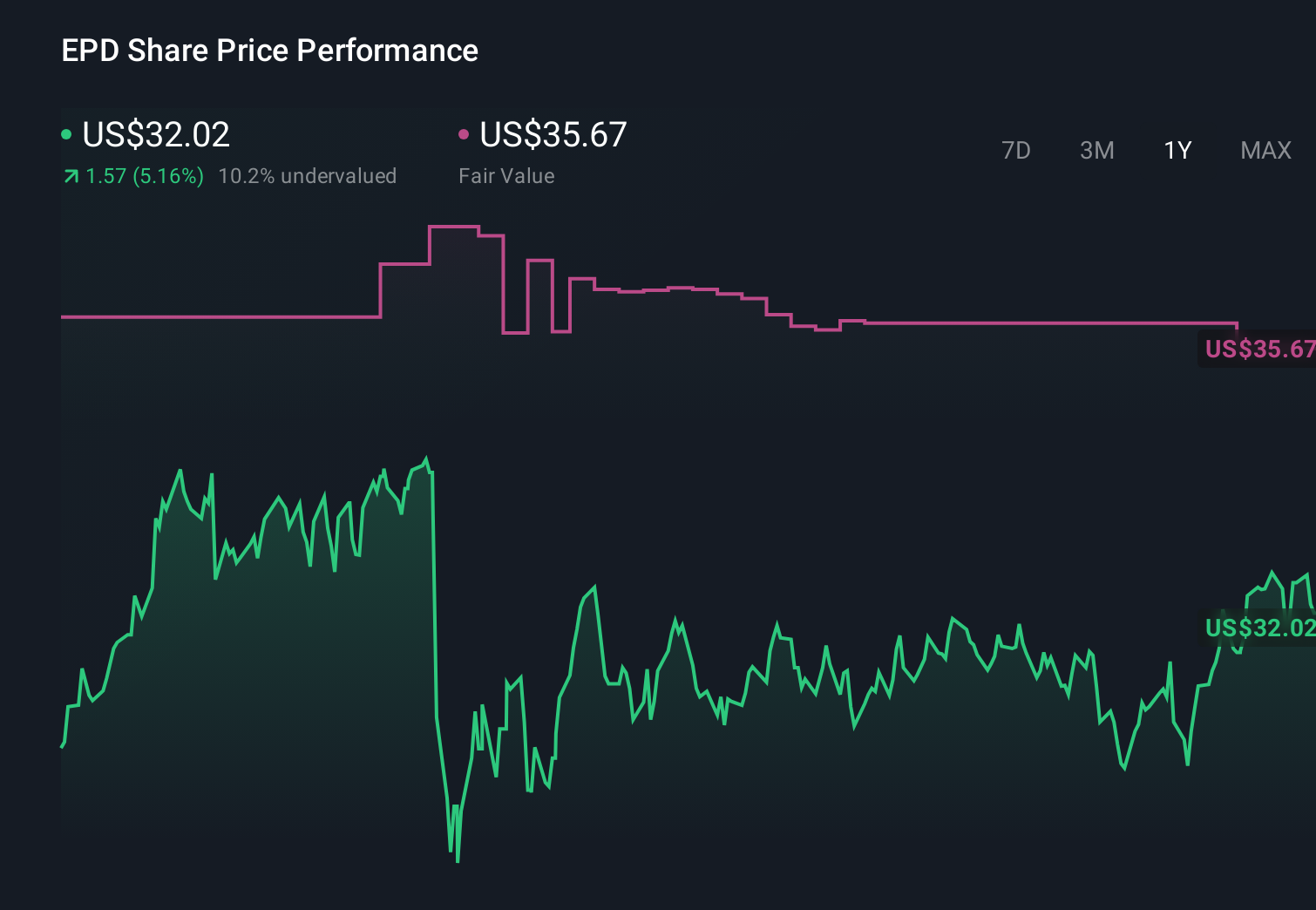

The most relevant recent development here is Enterprise’s continued distribution increases, including the Q2 and Q3 2025 hikes to US$0.545 per unit. That pattern underpins Cramer’s focus on yield and consistency, but it also raises the stakes around maintaining stable cash flows as new processing, pipeline, and export assets ramp up and as interest rate and credit conditions interact with the partnership’s US$31.9 billion debt stack.

Yet behind the appealing yield and media attention, investors should be aware of the potential earnings impact if credit conditions or interest rates were to...

Read the full narrative on Enterprise Products Partners (it's free!)

Enterprise Products Partners’ narrative projects $53.5 billion revenue and $6.6 billion earnings by 2028.

Uncover how Enterprise Products Partners' forecasts yield a $35.67 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Ten Simply Wall St Community members currently see Enterprise’s fair value anywhere between about US$29 and US$78, reflecting very different expectations. When you weigh those views against the company’s sizable debt and sensitivity to funding conditions, it becomes even more important to compare several independent assessments before deciding how Enterprise might fit into your portfolio.

Explore 10 other fair value estimates on Enterprise Products Partners - why the stock might be worth 8% less than the current price!

Build Your Own Enterprise Products Partners Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 13 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Enterprise Products Partners might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EPD

Enterprise Products Partners

Provides midstream energy services to producers and consumers of natural gas, natural gas liquids (NGLs), crude oil, petrochemicals, and refined products.

Undervalued established dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion