- United States

- /

- Oil and Gas

- /

- NYSE:DVN

Do Lower EPS Estimates and Positive Revisions Hint at a Stronger Devon Energy (DVN) Earnings Engine?

Reviewed by Sasha Jovanovic

- In recent weeks, Devon Energy has continued to attract attention as it is now expected to report quarterly earnings of US$0.95 per share, about 18.1% lower year over year, after previously surpassing both revenue and EPS consensus estimates.

- This combination of estimate revisions and earlier performance beats suggests the market is reassessing Devon's operational resilience relative to an industry that has seen weaker returns.

- Next, we'll examine how these positive earnings revisions, despite lower expected EPS, may reshape Devon Energy's broader investment narrative.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

Devon Energy Investment Narrative Recap

To own Devon Energy, you generally need to believe its focus on U.S. shale, operational efficiency and shareholder returns can offset commodity price swings and regulatory pressure. The recent expectation of lower year-over-year EPS, despite estimate upgrades and prior beats, does not materially change the near term catalyst, which remains Devon’s ability to sustain cost discipline and free cash flow. The key risk is still its heavy exposure to volatile hydrocarbon prices and shifting energy policy.

The most relevant recent development here is Devon’s continued share repurchase activity, with roughly 14.25% of shares bought back under its program since 2021. In the context of mixed earnings trends, this capital return approach may support per share metrics and signal confidence in underlying cash generation, but it also concentrates exposure to operational and commodity risks for remaining shareholders.

Yet, for all the talk of buybacks and efficiency, investors should still be aware that Devon’s reliance on volatile oil and gas prices...

Read the full narrative on Devon Energy (it's free!)

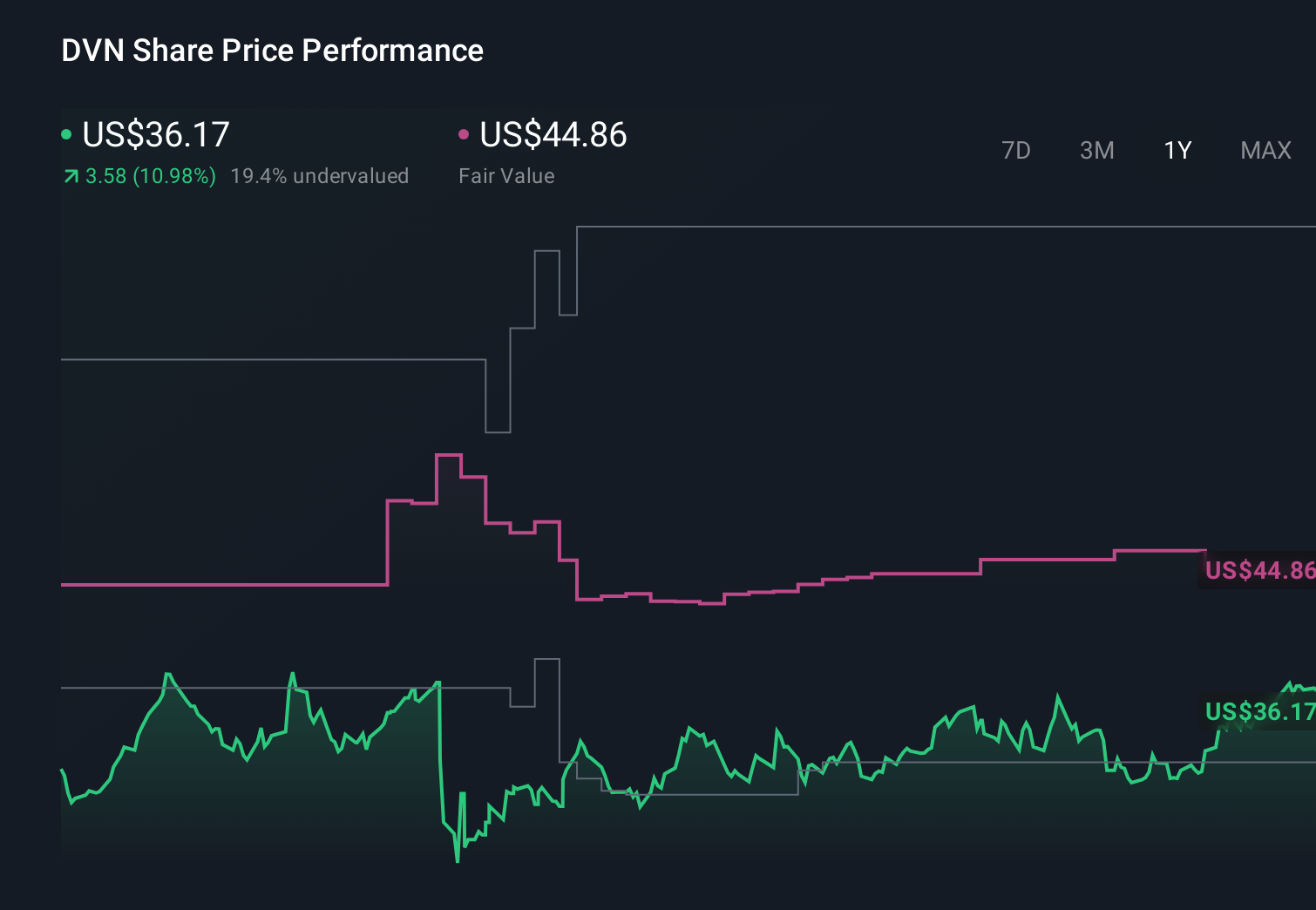

Devon Energy's narrative projects $19.3 billion revenue and $3.0 billion earnings by 2028.

Uncover how Devon Energy's forecasts yield a $44.86 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Eleven members of the Simply Wall St Community currently see Devon’s fair value anywhere between about US$30.95 and US$105.69, underscoring how far views can stretch. As you weigh those opinions, remember that Devon’s earnings and cash flows remain closely tied to commodity prices, a linkage that can quickly reshape both expectations and outcomes, so it is worth exploring several alternative viewpoints before deciding how you see the stock.

Explore 11 other fair value estimates on Devon Energy - why the stock might be worth 13% less than the current price!

Build Your Own Devon Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Devon Energy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Devon Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Devon Energy's overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 35 stocks are leading the charge.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DVN

Devon Energy

An independent energy company, engages in the exploration, development, and production of oil, natural gas, and natural gas liquids in the United States.

Very undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion