- United States

- /

- Oil and Gas

- /

- NYSE:DEC

Assessing Diversified Energy (DEC) After Buybacks and a New Dividend: Does the Valuation Reflect Its Cash Returns?

Reviewed by Simply Wall St

Diversified Energy (DEC) has been quietly reshaping its equity story, leaning on buybacks and dividends rather than splashy headlines. Recent share repurchases and a declared quarterly payout put the spotlight squarely on shareholder returns.

See our latest analysis for Diversified Energy.

Even with steady buybacks and that fresh dividend, the 30 day share price return of minus 6.2 percent and year to date share price return of minus 21.7 percent suggest sentiment is still cautious, despite a less severe 1 year total shareholder return decline.

If you are weighing DEC against other opportunities in the market, this could be a good time to broaden your search and explore fast growing stocks with high insider ownership.

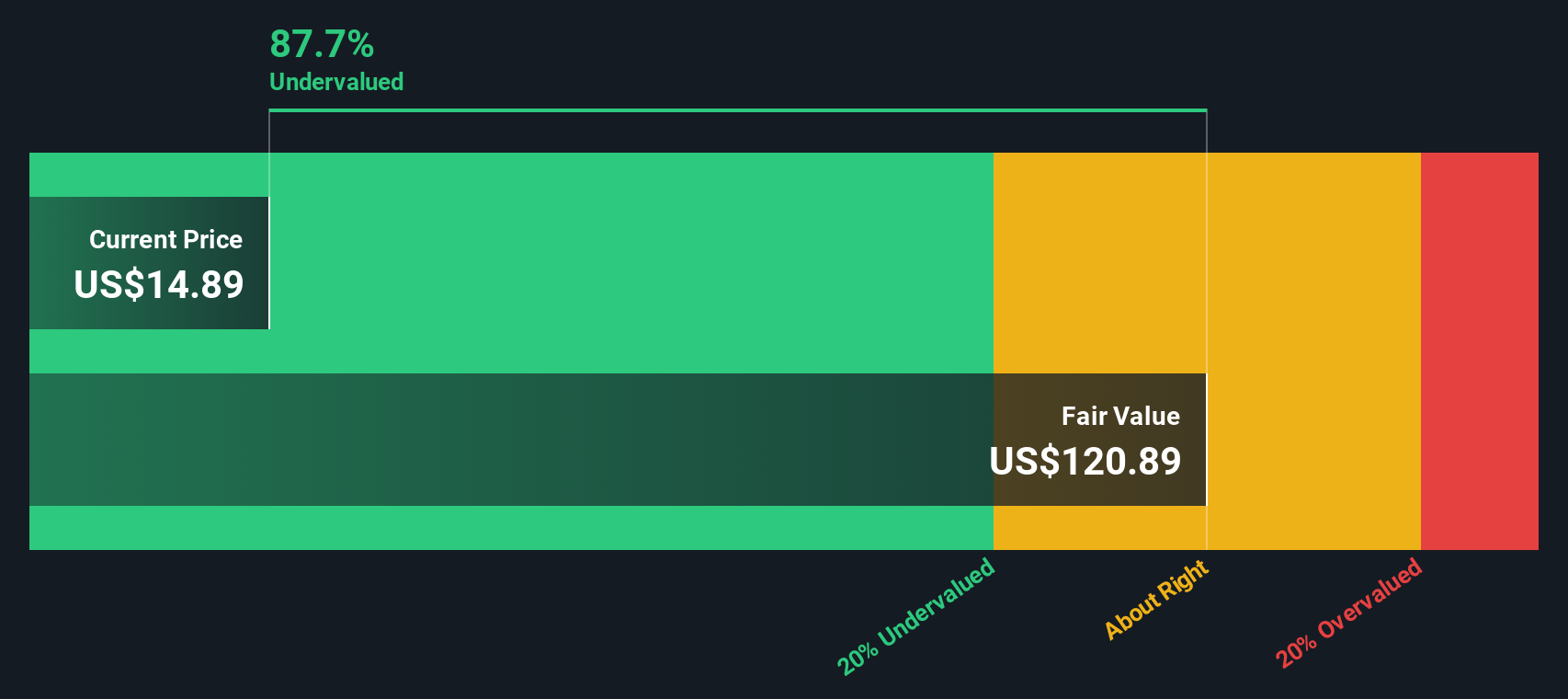

With the share price well below analyst targets and trading at a steep implied discount to intrinsic value, should investors treat Diversified Energy as a mispriced cash return story, or is the market already discounting its future growth?

Price-to-Sales of 1x: Is it justified?

Based on a price-to-sales ratio of 1x versus both peers and the wider Oil and Gas industry, Diversified Energy's last close appears materially discounted.

The price-to-sales multiple compares the market value of the company to the revenue it generates, a useful yardstick for asset heavy, often volatile energy producers where earnings can swing with commodity prices. For DEC, a 1x ratio signals the market is valuing each dollar of its revenue stream at a notable discount.

Against the US Oil and Gas industry average of 1.4x, DEC's 1x price-to-sales looks meaningfully cheaper, and the gap is even starker versus a 17x peer average, implying investors may be heavily discounting its future or overlooking its forecast return to profitability. Our fair price-to-sales estimate of 1.4x points to a level the market could ultimately gravitate toward if those forecasts are delivered.

Explore the SWS fair ratio for Diversified Energy

Result: Price-to-Sales of 1x (UNDERVALUED)

However, persistent net losses, alongside a multi year share price slide, could signal deeper operational issues, limiting any upside from valuation rerating or cash returns.

Find out about the key risks to this Diversified Energy narrative.

Another View: Our DCF Lens

While the 1x price to sales ratio hints at value, our DCF model is far more aggressive. It suggests DEC is trading about 86.8 percent below its fair value estimate of 104.22 dollars. If that gap is even half right, is the market missing a deep value turnaround?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Diversified Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 914 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Diversified Energy Narrative

If you see the numbers differently or want to dig into the details yourself, you can build a complete narrative in minutes: Do it your way.

A great starting point for your Diversified Energy research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, explore your next potential move by scanning fresh opportunities in minutes with our most popular, data driven stock screens.

- Capture early stage upside by targeting quality growth names using these 3634 penny stocks with strong financials that already show financial strength instead of pure speculation.

- Position yourself ahead of the next innovation wave with these 24 AI penny stocks focused on companies turning artificial intelligence into real, scalable revenue.

- Identify potential bargains by screening these 914 undervalued stocks based on cash flows where market prices trail the cash flows, before sentiment and multiples catch up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DEC

Diversified Energy

An independent energy company, focuses on the production, transportation, and marketing of natural gas and liquids primarily in the Appalachian and Central regions of the United States.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion