Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:AR

Antero Resources (AR): Exploring Valuation After Q3 Earnings Miss and 2025 Guidance Update

Simply Wall St

Reviewed by Simply Wall St

Antero Resources (AR) just released its third-quarter 2025 results. Adjusted earnings came in below expectations. Lower oil output and higher expenses weighed on the numbers, while stronger natural gas production and pricing offered some support.

See our latest analysis for Antero Resources.

Despite the earnings stumble driven by softer oil output, Antero Resources’ share price has shown notable resilience lately, with a 17.9% return over the past month and a solid 11.4% total shareholder return over the last year. Momentum has picked up in recent weeks, suggesting that optimism around higher natural gas production and the company’s 2025 outlook is outweighing short-term concerns.

If today’s rebound has you curious about other energy names catching a tailwind, it’s a great moment to broaden your scope and discover fast growing stocks with high insider ownership

With the stock trading roughly 16 percent below analyst targets and a track record of resilient returns, investors are left to wonder: does Antero Resources offer untapped value, or is the market already pricing in its growth potential?

Most Popular Narrative: 13.5% Undervalued

With Antero Resources’ fair value estimated at $42.10 and its last close at $36.43, this narrative points to potential upside beyond the current share price. The valuation story is based on details such as future cash flows, margins, and capital management, offering a clearer view of where the company could go next.

Antero's strategic focus on liquids-rich production and firm transport capacity to premium Gulf Coast and export markets enables it to realize higher prices than in-basin peers. This approach supports net margins and free cash flow growth even as domestic pipeline constraints continue. Ongoing capital efficiency gains, including declining maintenance capital requirements, longer well laterals, and lower well costs year over year, are reducing per-unit operating costs. These improvements are boosting net margins and providing additional cash for debt reduction and shareholder returns.

Want to know the secret behind this bullish figure? The fair value is supported by ambitious revenue targets, stronger profit margins, and capital returns that contribute to a higher multiple. Interested in the growth trajectory analysts have outlined? Discover how far this narrative stretches expectations.

Result: Fair Value of $42.10 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing regulatory pressures and the global pivot toward renewables could challenge Antero’s future earnings trajectory and threaten long-term growth assumptions.

Find out about the key risks to this Antero Resources narrative.

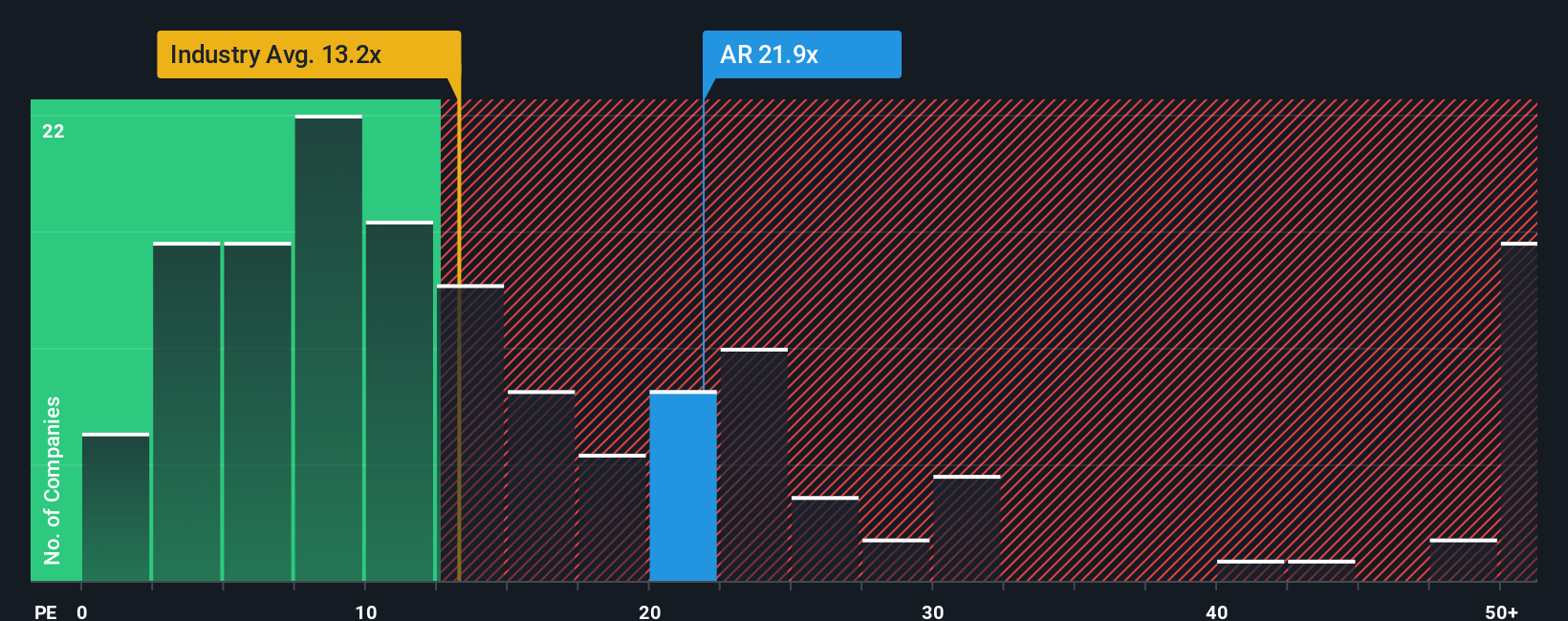

Another View: Multiples Tell a Different Story

While the fair value models hint at upside, the market’s price-to-earnings ratio of 19x presents a more expensive picture compared to the US Oil and Gas industry average of 13.4x. It is also above the fair ratio of 17.2x. This gap raises important questions about whether current optimism is ahead of fundamentals.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Antero Resources Narrative

Prefer taking the reins on your investment perspective? Dive into the numbers and shape your own Antero Resources story in just a few minutes with Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Antero Resources.

Looking for More Investment Ideas?

Expand your horizons and seize fresh opportunities before the market moves. Get ahead by teaming up with the smartest strategies and hottest themes today:

- Tap into tomorrow’s innovations as you scan these 25 AI penny stocks, which are pushing boundaries in artificial intelligence and automation breakthroughs.

- Maximize your income potential and uncover these 15 dividend stocks with yields > 3%, featuring companies offering yields above 3 percent for steady returns.

- Catalyze long-term growth by identifying these 914 undervalued stocks based on cash flows companies trading at attractive prices based on robust cash flow analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AR

Antero Resources

An independent oil and natural gas company, engages in the development, production, exploration, and acquisition of natural gas, natural gas liquids (NGLs), and oil properties in the United States.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative