Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:SF

Stifel Financial (SF): Exploring Valuation After Recent Stock Gains and Analyst Optimism

Simply Wall St

Reviewed by Simply Wall St

Stifel Financial (SF) continues to draw investor attention as its stock trends higher, with shares up roughly 7% over the past month and 15% year-to-date. The steady gains invite a closer look at what is driving this performance and how Stifel’s business lines contribute to its results.

See our latest analysis for Stifel Financial.

Stifel Financial’s share price has climbed steadily this year, reflecting growing optimism about its diversification and continued earnings momentum. With a 15% year-to-date share price return and a robust 109% total shareholder return over three years, investor sentiment appears to be building as the company delivers on both short- and long-term growth potential.

If you want to keep an eye on other companies building momentum, this is a perfect moment to discover fast growing stocks with high insider ownership

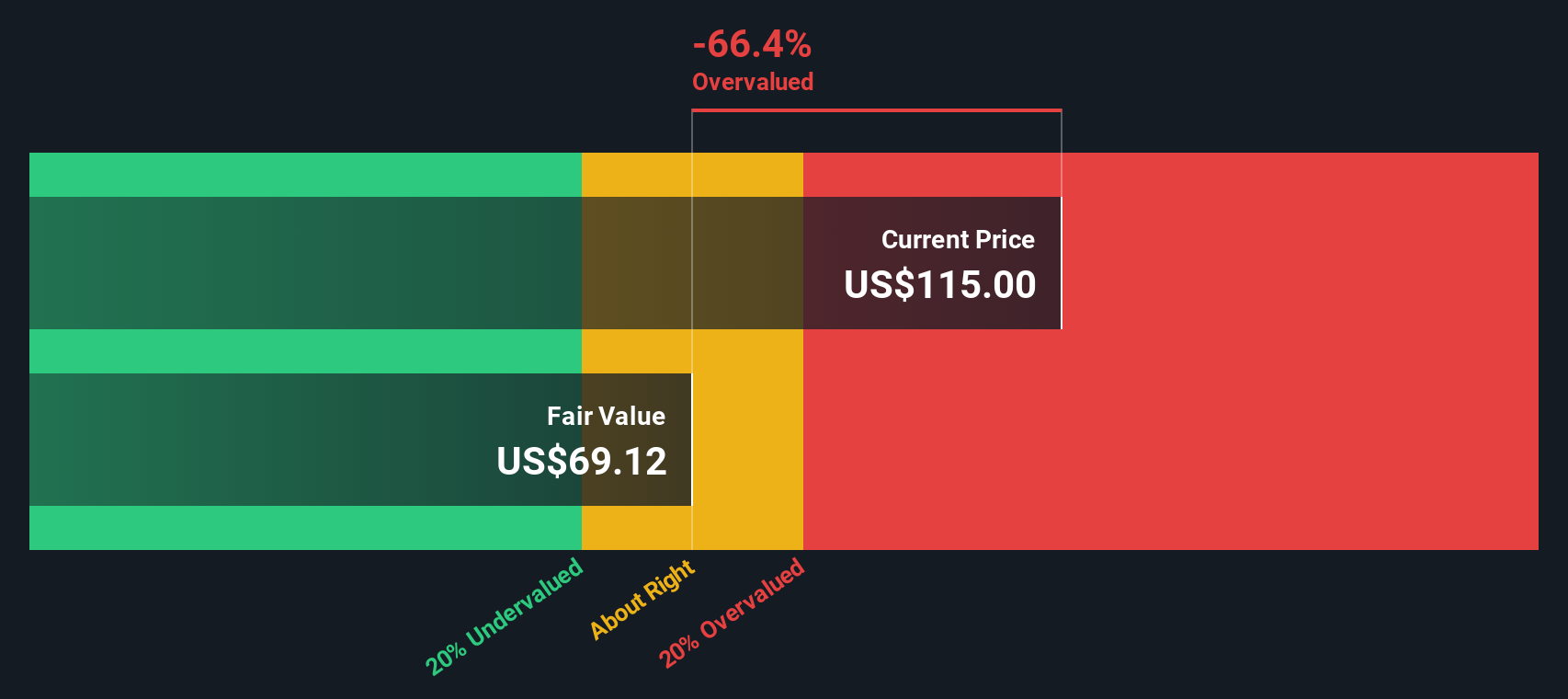

With Stifel’s stock reaching new highs, investors may wonder if the current price reflects an undervalued opportunity or if the market has already factored in future growth. This could leave little room for further upside.

Most Popular Narrative: 7.1% Undervalued

The current narrative puts Stifel Financial’s fair value at $131.38, which remains ahead of the last close price of $122. This gap has investors weighing the drivers behind analyst optimism for future performance.

The firm’s strong pipelines in financial advisory and institutional banking, particularly in sectors like technology, industrial services, and a growing appetite for bank M&A, suggest potential for increased investment banking revenue as market conditions stabilize. Stifel's strategic flexibility to prioritize share repurchases over loan growth reflects an opportunity to enhance earnings per share (EPS) and returns on investment, given current market conditions and undervalued stock prices.

Want to know why analysts are this bullish? The reason lies in a blend of aggressive share buybacks and major shifts in profit margins that could influence future earnings. Which financial lever could act as the next catalyst? Unlock the full narrative to see which assumptions play a key role in this valuation analysis.

Result: Fair Value of $131.38 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing legal expenses and market volatility could quickly shift sentiment. These factors can act as catalysts that challenge the current optimism around Stifel’s valuation.

Find out about the key risks to this Stifel Financial narrative.

Another View: Discounted Cash Flow Puts a Different Spin on Value

While analyst consensus points to Stifel being undervalued, our SWS DCF model offers a more conservative perspective. According to the DCF approach, shares may actually be trading above fair value. This raises real questions about the margin of safety for would-be buyers. Which lens best captures the underlying reality?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Stifel Financial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 916 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Stifel Financial Narrative

If you see these findings differently, or want to analyze the numbers yourself, it takes just a few minutes to build your own perspective, your way. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Stifel Financial.

Looking for More Investment Ideas?

Expand your horizons and put yourself one step ahead by checking out other handpicked stock groups our community is tracking. Don’t let valuable opportunities pass you by.

- Unlock stable income streams and steady growth when you check out these 15 dividend stocks with yields > 3% offering yields that stand out in today’s market.

- Position yourself at the forefront of innovation by exploring these 25 AI penny stocks transforming industries with artificial intelligence advances.

- Capitalize on overlooked value and strong cash flows by reviewing these 916 undervalued stocks based on cash flows before others catch on to these hidden gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SF

Stifel Financial

Operates as the bank holding company for Stifel, Nicolaus & Company, Incorporated that provides retail and institutional wealth management, and investment banking services to individual investors, corporations, municipalities, and institutions in the United States and internationally.

Adequate balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$28.1829.5% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on Fiverr International ·

Fiverr International will transform the freelance industry with AI-powered growth

Fair Value:US$36.8143.1% undervalued

78 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

937 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

144 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative