Something has stirred at loanDepot (LDI), and investors are tuning in. The company has filed a Shelf Registration for just under $25 million of its Class A Common Stock, directly linked to its Employee Stock Ownership Plan. While management hasn’t signaled dramatic strategic pivots, these filings can point to moves to shore up capital or rebalance employee incentives. This may signal a shift in how the business approaches future opportunities or challenges.

Despite this news, the share price tells a story that’s hard to ignore. Over the past month, loanDepot’s stock has climbed a hefty 117%, pushing its yearly gain up to about 60%. Momentum has clearly picked up speed in recent weeks, especially compared to a long stretch of tepid or negative returns prior to this jump. Taken together with annual net income and revenue growth figures, the shelf registration seems to arrive during a moment of shifting expectations.

The real question now is whether this surge reflects a bargain that the market is only waking up to, or if investors are already accounting for brighter days ahead. Is there genuine upside left for new shareholders, or is the premium price justified?

Advertisement

Most Popular Narrative: 164% Overvalued

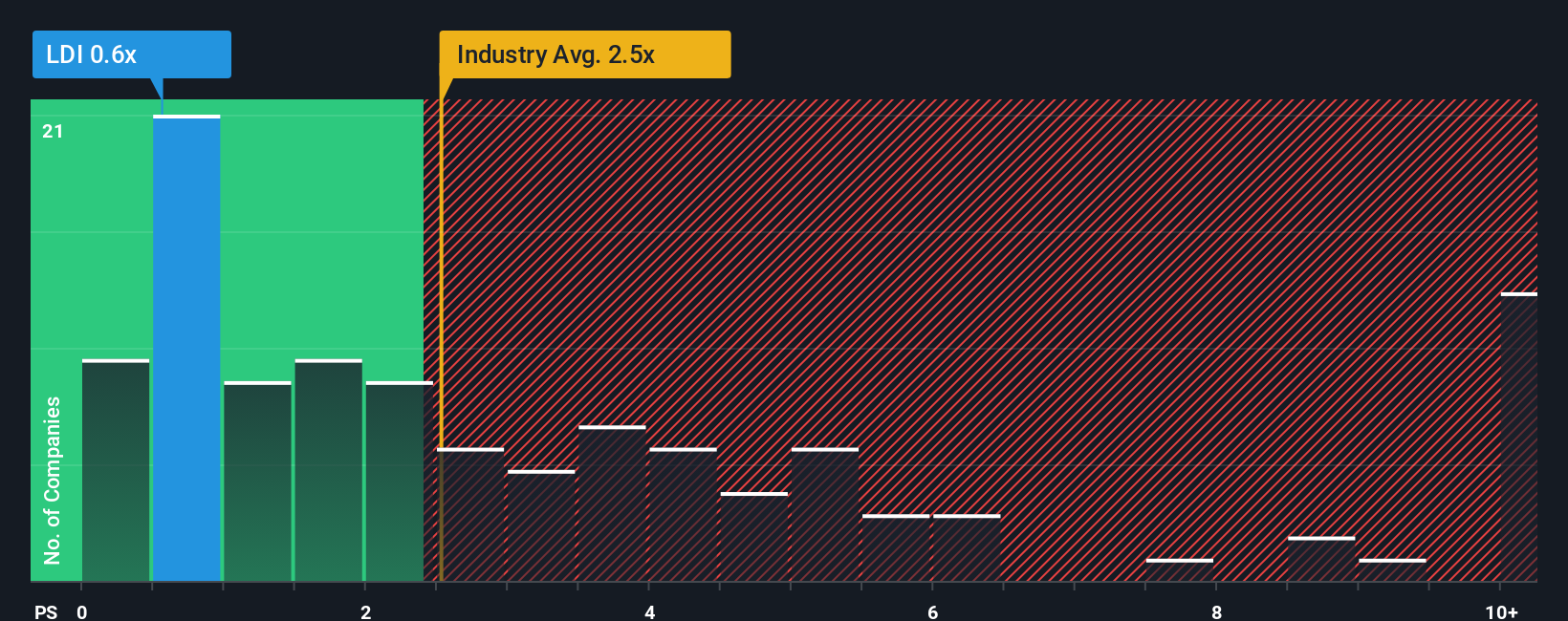

The most widely followed narrative sees loanDepot trading at a significant premium to its estimated fair value. Analysts project that the current share price is well above where fundamentals suggest it should be.

“Investors appear to be pricing in overly optimistic expectations of sustained high mortgage demand from Millennials and Gen Z. However, demographic trends suggest U.S. household formation is slowing and affordability challenges are likely to weigh on mortgage originations, potentially constraining long-term revenue growth.”

Is this rally built on solid foundations, or are investors ignoring critical numbers? There is a bold roadmap baked into expectations, the kind that relies on sharply higher revenue and a total reversal in profitability. What assumptions are driving that sky-high price target, and how do future margins and growth stack up? Get ready to be surprised: the path to the narrative’s fair value is built on projections few would expect from a mortgage lender.

However, if loanDepot’s technology and direct lending strategies drive efficiency or if a refinancing boom arrives, these expectations could quickly change.

Another View: Market Value Through a Different Lens

Taking a step back from growth projections, another common approach is to look at the company’s price compared to its sales. In this context, loanDepot screens as solid value against its industry. But is the stock’s recent run already pricing in all the good news?

Stay updated when valuation signals shift by adding loanDepot to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own loanDepot Narrative

If you see the story differently or want to shape your own insights, you can dive in and build a personalized take in just minutes. Do it your way.

Don’t let other compelling opportunities pass you by. The Simply Wall Street screener unlocks tailored ideas designed to give your portfolio an edge right now.

Accelerate your returns by targeting innovative businesses in artificial intelligence with our shortcut to AI penny stocks.

Maximize your search for long-term value and stable growth with companies focused on consistent dividend payouts. Start your hunt at dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if loanDepot might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.