Advertisement

- United States

- /

- Mortgage REITs

- /

- NYSE:IVR

Invesco Mortgage Capital (IVR) Profitability Return Challenges Bullish Narratives as Valuation Stays Elevated

Simply Wall St

Reviewed by Simply Wall St

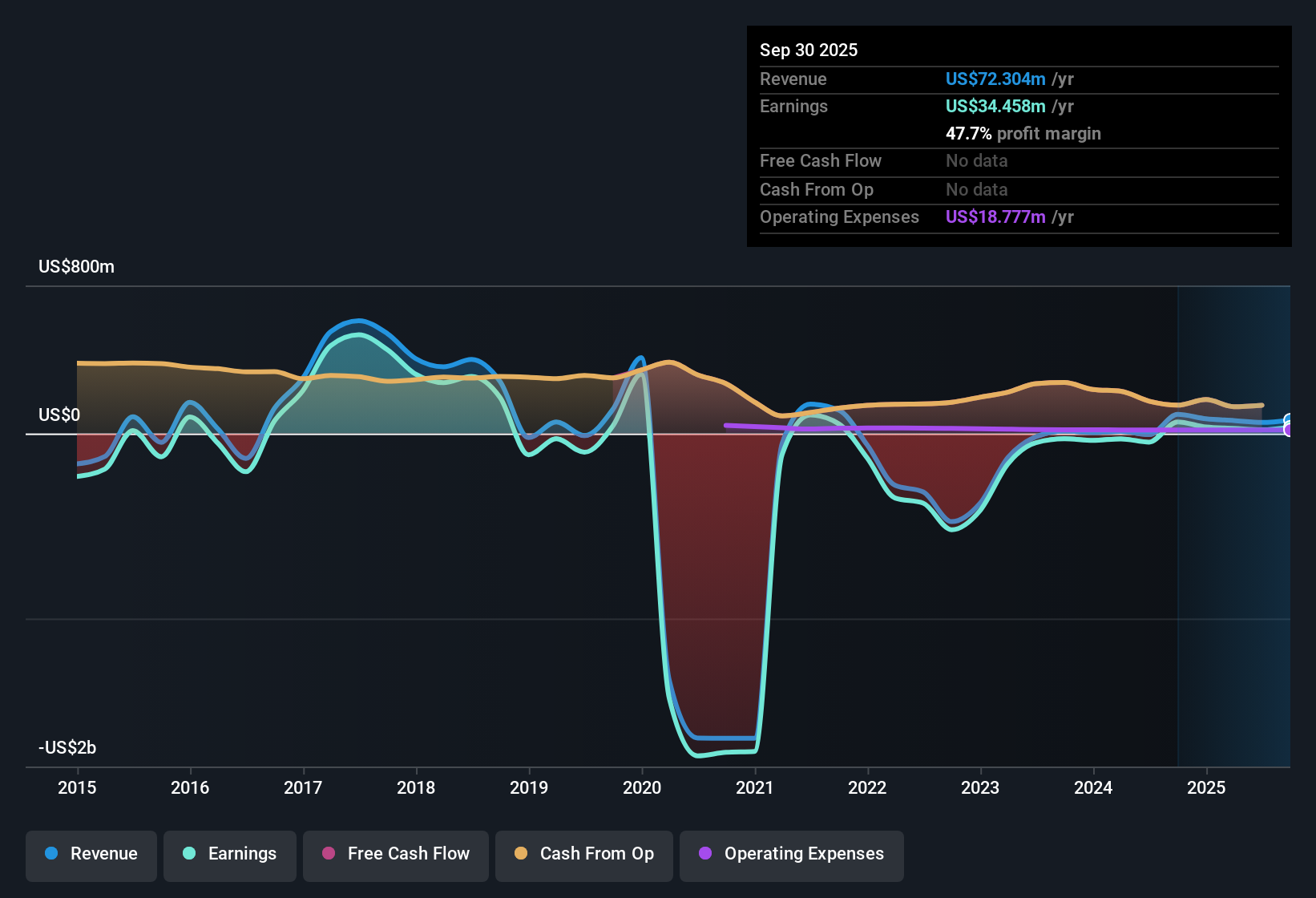

Invesco Mortgage Capital (IVR) has returned to profitability in the past year, with earnings growing at an impressive 70% per year over the last five years. Net profit margin has improved as the company reports high quality earnings. However, comparing the latest growth rate to the five-year average is difficult because of this recent shift. Investors have taken notice of the stronger bottom line, but questions remain about the sustainability of profits given that revenue is projected to decline by 3.1% annually over the next three years and the company’s valuation stands at a premium to peers.

See our full analysis for Invesco Mortgage Capital.Now, let’s see how these earnings results measure up against the current narratives. Some assumptions may be confirmed, while others could be up for debate.

See what the community is saying about Invesco Mortgage Capital

Capital Structure Revamp Lowers Costs

- Invesco Mortgage Capital reduced its capital costs by redeeming its Series B preferred stock. The company replaced it with lower-cost repurchase agreements and increased its allocation to U.S. Treasury futures to help stabilize earnings.

- Analysts' consensus view highlights how this capital restructuring supports margin growth and steadier performance.

- Improving capital structure is expected to boost net margins through lower financing expenses and more diversified hedging against interest rate volatility.

- The reallocation toward Agency CMBS and optimized interest rate hedges is directly connected to the consensus outlook for enhanced returns amid shifting market conditions.

📊 Read the full Invesco Mortgage Capital Consensus Narrative.

Share Dilution and Debt Pose Risks

- The number of shares outstanding is expected to grow by 7.0% per year for the next three years. The debt-to-equity ratio has increased following the capital structure changes.

- Consensus narrative notes that these trends could erode per-share value and put added pressure on future performance, despite efforts to strengthen the balance sheet.

- Dilution from a rising share count may offset the benefits of earnings growth for current shareholders.

- An increased debt load brings added risk, and higher borrowing costs could undermine margin expansion if market rates rise.

Trading at a Valuation Premium

- Invesco Mortgage Capital's price-to-earnings ratio stands at 25.6x, which is more than double the US Mortgage REITs average. The current share price of $7.53 sits just 2.1% above analyst consensus fair value of $7.37.

- According to analysts' consensus view, this premium price suggests investors have already factored in high expectations for future margin expansion and earnings, leaving limited room for further upside unless profitability significantly accelerates.

- The consensus target price indicates that the share price is close to fair value based on anticipated earnings, limiting value-driven upside.

- Peer comparisons reinforce the narrative that IVR needs to deliver on aggressive growth and margin targets to justify the current valuation premium.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Invesco Mortgage Capital on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a fresh take on the figures? You can shape your own perspective and add your voice in just a few minutes. Do it your way.

A great starting point for your Invesco Mortgage Capital research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

See What Else Is Out There

Despite a return to profitability, Invesco Mortgage Capital faces challenges from share dilution, rising debt, and a valuation premium that may be hard to justify.

If you want to sidestep balance sheet risks and find companies with greater financial resilience, check out solid balance sheet and fundamentals stocks screener (1983 results) for better alternatives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:IVR

Invesco Mortgage Capital

Operates as a real estate investment trust (REIT) that invests, finances, and manages mortgage-backed securities and other mortgage-related assets in the United States.

Acceptable track record second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor