Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:HASI

A Look at Hannon Armstrong (HASI) Valuation Following $500M Green Bond Issuance for Sustainability Initiatives

Simply Wall St

Reviewed by Simply Wall St

HA Sustainable Infrastructure Capital (HASI) has announced the issuance of $500 million in 8.000% Green Junior Subordinated Notes due 2056. This marks a meaningful step in strengthening its long-term financing for sustainability initiatives.

See our latest analysis for HA Sustainable Infrastructure Capital.

After a steady stretch earlier in the year, HA Sustainable Infrastructure Capital’s share price has picked up momentum with a 23.9% gain over the past month and a 1-year total shareholder return of 16.2%. This suggests renewed optimism following recent financing moves. Over the longer term, returns have been mixed, but the boost from the latest announcement reflects shifting sentiment and the potential for further upside as market focus turns to sustainability-driven growth.

If this surge in momentum has you wondering what else is catching investor attention, now is an ideal moment to broaden your search and discover fast growing stocks with high insider ownership

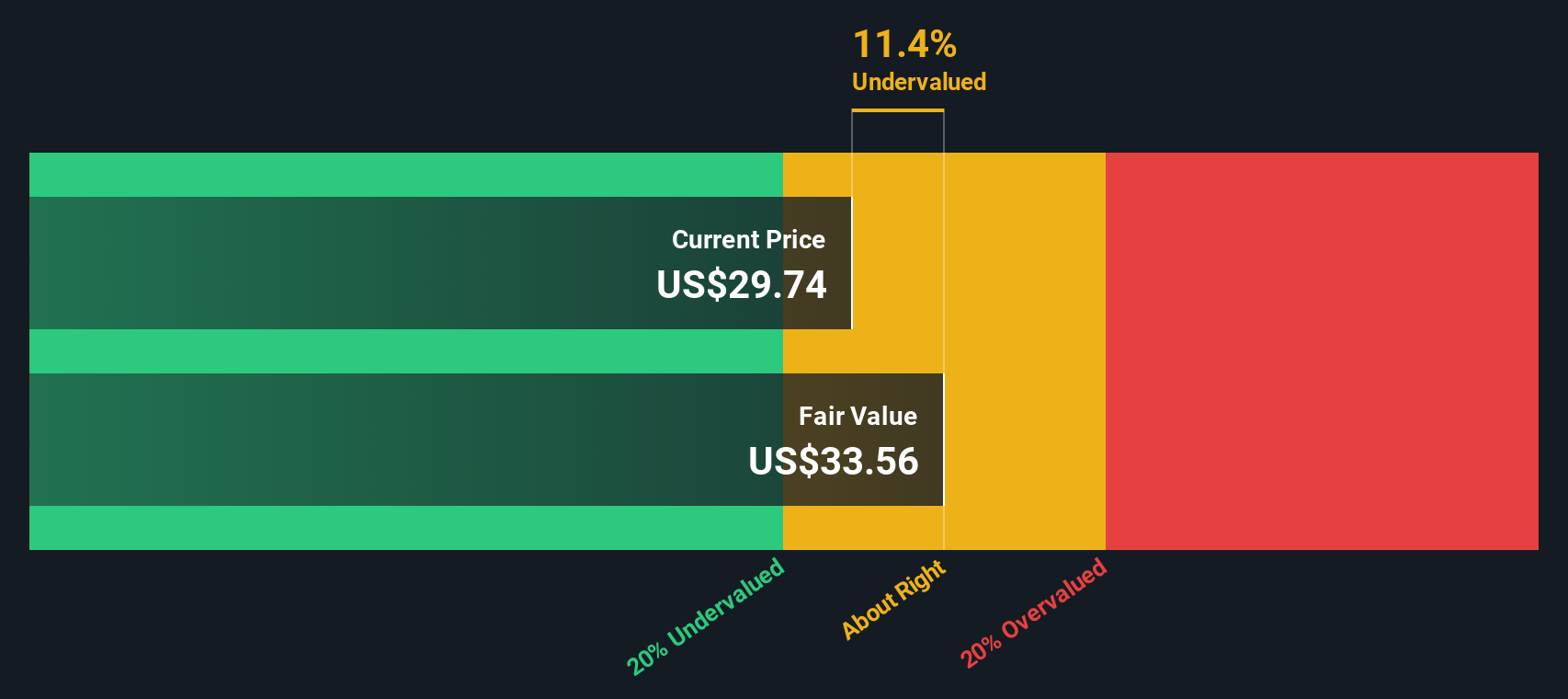

With momentum building after the recent green bond issuance, the key question is whether HA Sustainable Infrastructure Capital is now undervalued or if the market has already priced in further growth. This presents a real dilemma for would-be buyers.

Price-to-Earnings of 14.2x: Is it justified?

HA Sustainable Infrastructure Capital is currently trading at a price-to-earnings (P/E) ratio of 14.2x, which positions the stock just above the average for the US Diversified Financial industry and well below the peer group’s average.

The price-to-earnings multiple measures how much investors are willing to pay for each dollar of a company’s earnings. For sustainability-focused financial groups like HASI, this ratio reflects the expectations the market places on future profitability and growth from green finance.

While HASI’s P/E ratio is slightly higher than the industry average of 14x, it is less than half the peer average of 28.8x. This suggests that although the market recognizes HASI’s growth and sustainability profile, it is not assigning the hyper-premium reserved for some competitors. If the market consensus around fair value multiples shifts, HASI’s multiple could move in either direction, reflecting future optimism or skepticism.

Explore the SWS fair ratio for HA Sustainable Infrastructure Capital

Result: Price-to-Earnings of 14.2x (ABOUT RIGHT)

However, sustained outperformance is not guaranteed. Rising interest rates and regulatory changes could quickly shift market sentiment and impact future returns.

Find out about the key risks to this HA Sustainable Infrastructure Capital narrative.

Another View: SWS DCF Model Offers a Different Perspective

Switching gears, the SWS DCF model values HA Sustainable Infrastructure Capital at $36.63, which is about 6.2% higher than the current share price. This method suggests the stock could be undervalued, giving investors fresh food for thought. Are expectations really too low, or is the market missing something?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out HA Sustainable Infrastructure Capital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 914 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own HA Sustainable Infrastructure Capital Narrative

If you see things differently or enjoy forming your own perspective, you can explore the numbers and create a unique viewpoint in just a few minutes. Do it your way

A great starting point for your HA Sustainable Infrastructure Capital research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Unlock more opportunities by targeting companies with unique potential and strong fundamentals. Smart investors often look for advantages before the crowd takes notice.

- Find tomorrow’s tech giants by reviewing these 25 AI penny stocks uniquely positioned to benefit from the rapid growth in artificial intelligence and machine learning sectors.

- Boost your income potential with these 15 dividend stocks with yields > 3% that consistently offer attractive yields and may help you build a resilient, cash-generating portfolio.

- Capitalize on value by seeking out these 914 undervalued stocks based on cash flows that currently trade below fair worth, based on robust cash flow analysis and market mispricings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HA Sustainable Infrastructure Capital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HASI

HA Sustainable Infrastructure Capital

Through its subsidiaries, engages in the investment in energy efficiency, renewable energy, and sustainable infrastructure markets in the United States.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative